I post this up here in the tradition of what I’ve done the last few years. (You can find the others here: 2017, 2018, 2019, 2020)

Hidden-in-plain-sight within this list you may find the main reason that I read less books this year than previously! Feel free to guess in the comments below 😉

Here I’ll highlight some of my top picks across different categories.

Economy and Crypto

The Bitcoin Standard: The Decentralized Alternative to Central Banking by Saifedean Ammous

If you read one book about cryptocurrency, I would recommend The Bitcoin Standard. It doesn’t just talk about Bitcoin but gives a good history of money. Considering how little people understand how money actually works, this is important for understanding how Bitcoin can work as money. His sequel The Fiat Standard, is also great.

Principles for Dealing with The Changing World Order: Why Nations Succeed and Fail by Ray Dalio

I mentioned this in a recent article. It’s a great overview of the rise and fall of empires. As we’re going through this shaky time right now (the USA falling and China rising fast), it is useful to learn the historical lessons involved. This covers what a changing of the world reserve currency has looked like in the past.

The Pandemic

The Real Anthony Fauci: Bill Gates, Big Pharma, and the Global War on Democracy and Public Health by Robert F. Kennedy Jr.

I’ve obviously studied the pandemic a lot, as you can see by the many articles on this blog. But some have covered it even better. High marks for The Real Anthony Fauci. This covers not just the past two years but all the nefarious actions, particularly around HIV/AIDS that too few people know. The final chapter covering how the military allied itself with pharma (having to do with a biological weapons ban that left biological defense, aka vaccines, on the table) is worth the price of admission. It gives me hope that this was the #1 book in the world for a short time.

Pseudo Pandemic: New Normal Technocracy by Iain Davis

I also have to give a shout out to this one as well. While this drills into the details of inflated deaths and so much more, the best parts, in my opinion, covered the worldviews of eugenics, technocracy and the bigger picture of how current events fit in. Coming from the UK it also gives a greater perspective across the pond, compared to the USA. (Note that you can download this free from his website.)

How the World Really Works

Beyond the pandemic, there’s so many good ones. This subject matter is the main thing I read about these days. But I’ll select just four. I might also term this conspiracy history, or how evil is perpetrated often under the cover of good.

The Shock Doctrine: The Rise of Disaster Capitalism by Naomi Klein

Witness the pattern of economics and totalitarian action done in country after country after country. This playbook is being rolled out worldwide right now (though Klein herself doesn’t seem to see it!). This is foundational and I mention it in this article, Is Your Money Safe? Is the Economy Safe?

Poisoner in Chief: Sidney Gottlieb and the CIA Search for Mind Control by Stephen Kinzer

When people laugh off conspiracy theories, I know that they simply don’t understand history. The CIA literally tortured people in cruel ways as part of their experiments. Dosing them with LSD along with sensory deprivation for weeks on end. And that’s just one example of what we know about as covered in this book. My theory is they were more successful in these experiments than what has been let on. Still, the understanding of the publicly available knowledge is critical.

The Rape of the Mind: The Psychology of Thought Control, Menticide, and Brainwashing by Joost Meerloo

The title tells you what you’re in for. Meerloo was in the Netherlands when the Nazis came through. Helps to flesh out and give some perspective on the former book. I mentioned this book in this article, Totalitarian Takeover.

Empire of Pain: The Secret History of the Sackler Dynasty by Patrick Radden Keefe

Before Purdue Pharma, Arthur Sackler singlehandedly developed pharmaceutical advertising and was a pioneer in the corruption of regulators. His sociopathic children and brothers children were worse. This book catalogs the rise of what is a worse pandemic going on right now, the opioid epidemic, and just how lucrative it was to become philanthropic high society members. In the reality inversion they caused tremendous pain by treating pain. If you’re thinking in terms of family dynasty at all I would encourage you to read this as a cautionary tale.

Science

The Turning Point: Science, Society, and the Rising Culture by Fritjof Capra

Amazing that this book was written decades ago! Capra was a prophet that saw the swinging of the pendulum and put so well into words many things I was thinking. If you’re into philosophy of science, this is a must read.

Not Even Trying…The Corruption of Real Science by Bruce G Charlton

A quick read that accurately diagnosis some of the main problems. There’s a focus on peer review, which instead of making for good science, has turned into a popularity contest.

Health

The Phoenix Protocol: Dry Fasting for Rapid Healing and Radical Life Extension by August Dunning

I don’t read too much about health these days, though you can see the topic sprinkled in my list. This book is the most intriguing to me on the topic of dry fasting which I plan to experiment more with.

The Body Keeps the Score: Brain, Mind, and Body In The Healing of Trauma by Bessel Van Der Kolk, M.D.

A dense book but well worth reading through. If you want to understand trauma and healing it, this is probably the best place to start. Highly recommended!

Mind-Stretching

The Shamanic Way of the Bee: Ancient Wisdom and Healing Practices of the Bee Masters by Simon Buxton

A non-fiction account of a man initiated into a secret sect of shamanism focused around bees. The out-of-this-world shamanic events are mind-blowing. A highly entertaining read.

Fiction

Abaddon’s Gate by James S.A. Corey

This is the third in a series called The Expanse, my favorite so far. Its an Amazon Prime series, though as typical the books are far better, especially this third book that loses its best character and gets scrunched into half a season.

It’s some good ol’ sci-fi drama. I’m enjoying it and have the rest of the books in the series that I’ll eventually be reading.

Your Turn

If you have any questions about any of these books go ahead and ask them in the comments below.

Also please share your top one or two books that you read last year. I’m always looking to add to my reading list.

In recent articles I covered possible scenarios. Keyword being possible. While I like to think in probabilities and possibilities, I’m aiming to put in what I think is most likely to occur here and with the time frame of just a year.

In other words, what follows are my highest probability picks.

Again, I’ll reiterate that this isn’t from looking into a crystal ball so much as it is looking at the trends in play and projecting where those lead. As such, this article is not just predictions, but serves as a current state-of-things status report too.

Chief among my superpowers is learning and synthesizing. My heavy “data diet” of speed read articles and books, along with 3X playback videos and podcasts, is overwhelming at times. For me, it’s a long-cultivated skillset.

Of course, just absorbing the information would only be so useful. Bringing it all together, then distilling it down to the most useful and actionable is what I’m truly aiming for. Add a dash or three of intuition and here we are.

The Pandemic

It’s going to be the same old song and dance as long as they can get away with it…but with some interesting twists.

If you haven’t figured it out by now, SARS-CoV-2 is not going away. It’s endemic, we have to live with it, just like common coronaviruses that have caused some versions of the common cold before all this.

The definition of insanity is to do the same thing over and over again despite the results. Clearly, our world is insane.

The data coming out of Israel is interesting, such as this study from July 2021. “This communication… challenges the assumption that high universal vaccination rates will lead to herd immunity and prevent COVID-19 outbreaks… In the outbreak described here, 96.2% of the exposed population was vaccinated. Infection advanced rapidly (many cases became symptomatic within 2 days of exposure), and viral load was high.” I like to throw this quote at people who say the vaccines stops infection.

But there is a big positive sign. Omicron, while spreading more rapidly, is even less deadly than the already statistically speaking not-so-deadly other variants.

In addition there is something extremely odd about Omicron. “Omicron has no recent ancestor. Its most recent ancestor existed in the beginning of year 2020 and went extinct. The weirdness of this is similar to a young man who is alive today and is proven genetically to be a biological son of George Washington: you know that something very special is going on,” writes Igor Chudov.

Of course the public narrative comes up with some hypothesis about this being because of an immune-compromised individual, or jumping to an animal and back to humans. Publicly, there’s no talk of possible (more) lab engineering. The question to ask: did someone assist in making this virus more innocuous? If so, why?

Or, if indeed this did come from a lab, is there some more nefarious purpose to it that we can’t see just yet?

Or does it cause people to double-down saying I’m glad that I had the vaccine or else it would have been worse?

What I see happening is both. Some places continuing pushing forward with draconian policies. Other places increasingly stop playing the pandemic game.

Hmmm, when would that be? End of November plus 100 days takes us into the middle of March. Right after Winter ends…you know when historically there’s always been cold and flu season coming to an end. Guess what can then take the credit for ending the spike once again? The vaccines, just like what happened as they rolled out in 2020.

For those places that are escalating, that means more mandates and coercion. In the USA, we only have to look at some other countries that are ahead of the race.

Across the pond, “Austria is the first European country to demand compulsory vaccinations for all citizens. Now, employees will be tasked with enforcing fines on those who refuse to acquire the COVID vaccine in the Austrian city of Linz.” Socially enforced once again.

And of course, Australia already has the camps ready and is taking away people who test positive.

New York was trying to pass a bill for the “removal of cases, contacts and carriers of communicable diseases who are potentially dangerous to the public health.” Apparently, this already has been struck down. Yet that’s just one of several bills proposed for vote on January 5th, 2022. JP Sears covers this well.

If you’re anywhere that something like this passes, get out!

I’ll distill this down. My predictions on what we’ll see in 2022:

People detained in “medical facilities” or camps within some parts of the USA.

There will be more of these facilities in many parts around the world, copying Australia. These will include sending people that aren’t even “infected” but “exposed,” aka the contacts of cases.

Fines will begin on the unvaccinated for being so. This will happen in some states but will likely be pushed by the Biden admin too.

The growth of “unvaccinated hunters” as a job position for many countries. Of course, they’ll have a nicer title than that.

At least one example of a vaccinated person killing an unvaccinated person because they’re a “threat” to their health.

Escalation of doctors and hospitals refusing to treat the unvaccinated completely.

Escalation of many more grocery stores refusing the unvaccinated.

More lockdowns in more countries specifically just for the unvaccinated.

The vaccines will be rolled out to all ages within the USA, meaning the 0-4 year old group is next.

The vaccines will be added to the official CDC schedule for children to enter school.

The companies talked about mRNA jabs as updates to the software of life. Fauci and others want to update your immunity every five months. 2022 sees the year when boosters become variant-specific.

A strong push in the USA to make all flights reliant on being jabbed and current with boosters.

Other countries will pass similar measures. The unvaccinated will not be able to travel, whether flying or driving out of some places.

There will be Chinese-style reeducation camps in other countries for the unvaccinated to be “deradicalized”.

Dystopian, I know, but that’s fortunately only half of the story…

The Pushback and the Revolution

The pushback is working to a large degree. For instance:

That’s in legit courts. The legal angle is important, but it certainly can’t be the only part of the picture. The pushback will continue to escalate in country after country in all ways it can.

My prediction is it actually will get to the point of revolutionary behavior in some places.

Austria, Germany or other parts of Europe seem the most likely as they’re going the most totalitarian with solid levels of pushback. The protests are already huge. Australia possibly too, but it’s harder to judge from this point.

There will be violence. Again, I hope for it to be minimal, but it is already existing. It needs to be quite strategic so that the violence doesn’t simply beget more violence.

In case, you haven’t seen any footage related to the above, here’s one short clip in France.

Holy shit the French riot police is getting fucked up 😅 the law usually gets forced at the end of a police baton but it seems that the roles are changing… People are fed up! pic.twitter.com/8exOFAptKh

Let me be clear. I am not advocating for violence. I am simply predicting that it will occur.

Here’s another interesting example, apparently threats did change a lawmaker’s mind! State Rep. Jonathan Carroll, led a “proposal requiring unvaccinated Illinoisans to pay their health care expenses — including hospital bills — out of pocket if they contract COVID-19.” He said in “a statement Thursday that he decided not to pursue the legislation he filed earlier in the week because of the ‘unintended divisive nature’ of the proposal.”

Seems like a mixed message to me that the threats were horrible and unjustified…yet they worked when nicely pleading to lawmakers doesn’t appear to in most cases.

Here’s some specific events I’ll be on the lookout for:

Mainstream media figures will be physically attacked, maybe even killed.

Politicians will be physically attacked, maybe even killed.

The size of worldwide protests will continue to grow. As has been happening, only independent media will cover such, which is why normies don’t even know they’re happening.

Increasingly, protests will become riots with clashes against the people and the police/military. Increasingly, we’ll also see police joined with the people in.

The destructive behavior this time will focus on damaging parts of “the system” such as camps, vaccination facilities and the like.

There will be cases of sabotage of communications and technology of such parts of “the system”.

In the USA, November holds the midterm elections. There will be fraud, but nonetheless, Democrats will be losing a lot of power.

As I’ve talked about before only our side is growing in numbers. More people are popping out of the matrix. Many people who got the vaccine the first time, aren’t going back for round two, let alone three, four and beyond.

C.J. Hopkins made a great point that GloboCap, as he likes to call it, needs to work with at least the pretense of democracy. “In other words, we need to make GloboCap (and its minions) go openly totalitarian … because it can’t. If it could, it would have done so already. Global capitalism cannot function that way. Going openly totalitarian will cause it to implode … no, not global capitalism itself, but this totalitarian version of it. In fact, this is starting to happen already. It needs the simulation of “reality,” and “democracy,” and “normality,” to keep the masses docile.”

As you’re witnessing, they are going more totalitarian and this has the benefit of making it that much more apparent to everyone.

I’m encouraging people to ask where those buying into the narrative draw their line personally as to what is overreach. Mostly people ignore the question, as that is the only defense against it. But I have finally gotten one person to answer it. As we know the agenda is to cross all such lines, this helps rally people to our side.

A follow-up question if they do answer is to ask, when they do cross that line, “What are you going to do about it?”

As it becomes increasingly totalitarian, more people will stand up and say no more. Of course there is an adoption curve of learning and acting on this stuff.

In one sense, that is all we really have to do. To not participate in the madness, the consequences be damned. Because their only response is to go more totalitarian and they increasingly have less justification for doing so.

Fantastic podcast here from Aubrey Marcus with Charles Eisenstein. This is some level five conversation.

One of my takeaways from this was that courage is largely a community thing. I’ve said this before in different ways, but the more that people stand up, the easier it becomes to do so. I see more and more people speaking out. I see encouraging signs of that.

And with this trend, I predict 2022 is the year where this tipping point is reached. Understand that it doesn’t take courage anymore once just about everyone else is doing. Each and every person speaking out is less courageous than the person before. That doesn’t mean that it’s not important to do so, just that it becomes easier as the crowd shifts.

The key of the totalitarian control grid plan is vaccine mandates and passports. These must be pushed back on each and every chance we get. It is the lynch pin of the whole system.

If they get that, the noose is on. If they don’t get that, the other pieces cannot so easily fall into place.

All you have to do is say no. And I understand that this can be a big ask because your people’s livelihoods depend on it.

There are strong elements of both sides will not shift. This only leads to revolution and/or war. It’s the historical facts of such a situation.

As I said earlier, the good news is that there will be other places, small towns in the country mostly, perhaps even small countries themselves, that simply stop complying with all the BS. It will be “normal” in these locations. In this way there will be decentralized growth of alternatives, while the propaganda becomes increasingly spitting into the wind.

Similarly the psyop, will be dismantled legally piece by piece in certain places. The tide turns.

This is the de-escalation that is occurring at the same time than escalation is occurring.

The Counterrevolution

Unfortunately, the increasing pushback comes from the other side too.

As a result of attacks, private police and military will be used increasingly by certain public individuals.

There will be assassinations of leaders of freedom. Of course, these won’t look like assassinations to the normies. They’ll have plausible deniability. (There’s already some evidence of this taking place throughout the pandemic.)

The army will be called in to quell the protests and riots increasingly.

The UN “peacekeepers” will have to be brought in to assist in some countries.

Any sort of government aid will increasingly be tied into being a good citizen (aka vaccinated and obedient).

The propaganda will ramp up because they need the people themselves to enforce their rules. It’ll get that much more bat-shit crazy as the demonization of the scapegoats must escalate.

It’s an information war first, economic war second, and will increasingly become a physical war. This is because information and economic warfare are the appetizers to the real thing.

In many ways, I perceive that 2022 could be the make-or-break year for humanity.

Perhaps I’m smoking too much hopium, but I think we will make it. That is my prediction. Understand that that doesn’t mean it’ll be “done with” in 2022, far from it, but the tide of the war will change.

Think about when Hitler and Napoleon before him over-reached by attacking Russia. It turned the tide of war. This push for vaccine mandates and passports for a vaccine that is not safe nor effective is the turning point.

The Cyber Pandemic

I predicted this last year but was either wrong or too early. So I’m pushing the prediction out to 2022 or beyond. The thing is, at this point, I don’t know enough about the topic to make a solid prediction.

I’m going to deep dive into this area in an upcoming article. With that hopefully I can paint a more useful picture of what this likely will look like.

I was struck reading The Real Anthony Fauci, especially the last chapter where RFK Jr. goes into all the pandemic-planning exercises over the past two decades.

Many of these war games I was familiar with. Some were new to me. What became clear was that these training exercises were about coordinating among institutions and individuals how to rollout the real thing. Each and every event focused on vaccines, grabbing more totalitarian control and using censorship.

None of them focused on actually keeping people healthy, such as repurposing therapeutics, having stockpiles ready, etc. The planning and training was about making sure the powers-that-be could and would act in lockstep (which happened to be the name of one such exercise).

It brought me back to watching the full Event 201 videos which I did when the pandemic started. Here’s my March 2020 article.

Something stood out to me in reviewing this information. They predicted internet blackouts in some countries as part of the censorship/pandemic response.

In other words, they were planning for (expecting?) pushback to be even greater early on and thus needing to do such things!

My feeling right now is the big cyber pandemic is the card they pull out when they need too.

The other huge piece is this. The pandemic was the excuse for the collapsing financial system. It both kicked the can down the road and allowed the grift to continue. The virus was blamed, never the bankers.

Our economy is that much more in collapse now. The bankers won’t be blamed publicly, so the cyber pandemic is the next scapegoat, as well as emergency to seize more power.

The tide is turning…and that makes me think exactly such an event could be close to happening. When they are losing control of the narrative, and we see signs of it cracking left and right, they MUST do something to gain back control.

The pandemic wargames such as Event 201 and SPARS are virtually a script for the entire real thing (though less deaths in real life than in those).

What if the cyber war games are much the same? I need to understand what occurs. Again, far more detail upcoming in my next article I hope to have out in the next week or two. With that there will be some more projections/predictions of how it could roll out.

The Economy

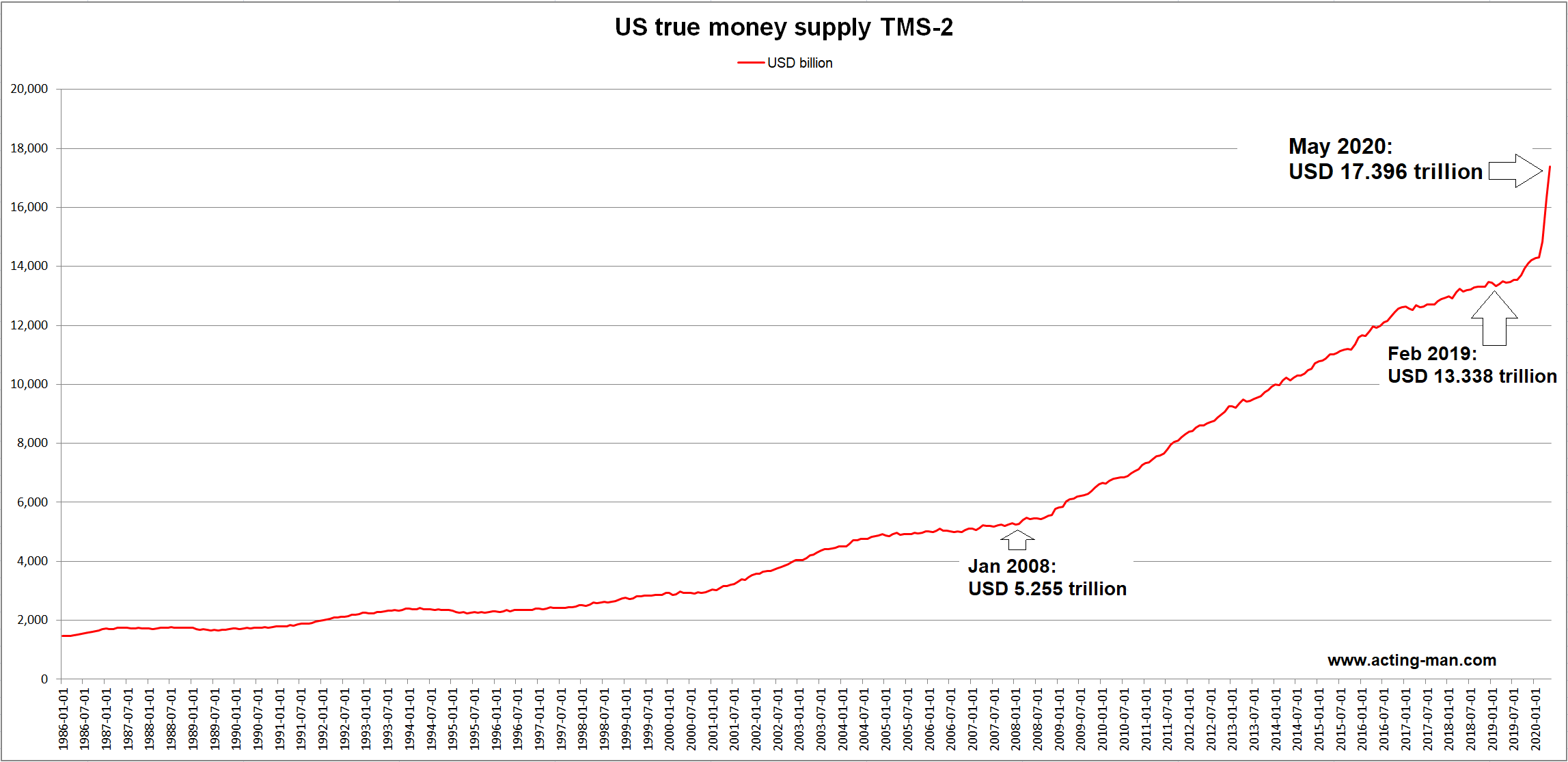

The Fed recently mentioned that they’d increase rates, but this is a lie. The inflationary money added into the system has been described as crack and heroin. The current economic system is an addict that has no chance of redemption.

Any tapering will be reversed in short order once the withdrawal symptoms kick in. Why? Well, those withdrawal symptoms hurt the predator class.

In other words, inflation will continue, even going higher.

We’re not going to see deflation. They’re going to inflate until the entire worldwide economy bubble bursts. The only deflation will occur with the new financial system coming in.

We’ll see prices continue in the same directions. While the frenzy has died down, as comes with winter anyway, houses will continue to see higher values.

Supply chain problems will become even more apparent in certain sectors such as chip manufacturing and all the technological devices that depend on such. I just purchased a vehicle and the inventory was extremely small because of these chips.

The US dollar will not hyperinflate, but will continue to accelerate in it’s inflation. It’s the least worst fiat currency and as such has shown some strength recently.

More of the same…until the time is ready for it to pop. Right now, I feel like the cyber pandemic is likely the engineered pin that pops the balloon for both the collapse and demolition, but again need to do more research on the topic.

And I feel like this is most likely coming when the pushback is winning, because that makes sense too.

Understand also that such an event opens up the money printing spigot even more widely open.

Cryptocurrency

I’ve still got two more articles on cryptocurrency and various scenarios and narratives coming up, hopefully in January. Those will explore some of these ideas further.

I do think there’s more blue-sky ahead though we haven’t yet hit the bottom of this sideways/down leg. After that, I am undecided if it will be a quick run up and a blow-off top before it collapses.

I’ll be looking at the following signs for a blow-off top encroaching:

Retail flowing in from A) tweaks in social media algorithms showing social metrics and B) even mainstream news coverage

Or it may just slowly grind higher over time, with some dips and sideways action along the way. Again, that depends on larger economic events. You can bet I’ll be watching those indicators like a hawk.

Either way, I’m still heavily positioned in the space though there’s a good chance I won’t be so heavily invested come 2022’s end. You’ve got to have an Exit Plan! (I discuss my 5-prong exit strategy as one of the bonuses in the Crash Course.)

Certain sectors such as crypto-gaming are going to do particularly well. (I just covered my top pick for this in my Crypto Conspiracy membership.)

Some of the alternative Layer 1’s will continue to do well. Terra (LUNA) continues to impress me, though I feel that Ethereum (ETH) and it’s Layer 2’s are likely to have another big opportunity to shine too around mid-2022.

I predict we’ll see at least another country or two follow suit from El Salvador in adoption of Bitcoin.

We’ll definitely see more cities, states and various places make steps towards using it as a parallel currency.

Regarding the SEC and regulation of crypto, this will occur to some degree in 2022. It’s going to be restricting in some way, compared to other countries, thus forcing more talent and innovation out. But it will not cripple the industry. I don’t think they’ll go that far, after all their control-grid rides on many of the same rails.

Speaking of control grids, China is rolling out their CBDC early in 2022, surrounding the Winter Olympics. There are tons of other CBDC experiments going on that are worth watching. The pace of CBDC’s is going to accelerate.

I think a Tether (USDT) collapse could damage the overall crypto market and allow the bankers and regulators to step in saying this is why you need us. I see that as on-the-table. However, I also don’t know if the bankers, outside of China, are ready to step in with their solutions just yet either.

What head of the SEC Gary Gensler (aka Goldman Gary) is doing seems mostly to be playing a delay game. Delay for what? Until they are ready?

Obviously, any sort of cyber pandemic could play into crypto and/or disintegrate these markets in a big way.

Ghislaine Maxwell

I wrote this last week while working on the article, “She will be found guilty.” I didn’t realize the verdict would come in before the article was out. And indeed she has, on five of six counts. This will be appealed of course.

But the important thing to the powers-that-be is that she’s the scapegoat and this case goes no further beyond her.

And yet there will be continued slow moving push towards just that.

The Epstein saga is important because it shows just how high such things go (royalty, presidents, businessmen and intelligence agencies), how long they can go on (Epstein was reported to the FBI back in the 90’s), and the extent of cover-up involved (Epstein didn’t kill himself).

Eugenics and Genocide

Besides The Real Anthony Fauci, if you read one book about the pandemic, I would recommend Pseudo Pandemic: New Normal Technocracy by Iain Davis. You can download this free at his website.

While this drills into the details of inflated deaths and so much more, the best parts, in my opinion, cover the worldviews of eugenics, technocracy and the bigger picture of how all these current events fit together. Coming from the UK it also gives a greater perspective across the pond, compared to the USA.

Understanding eugenics is key to understand what we see going on.

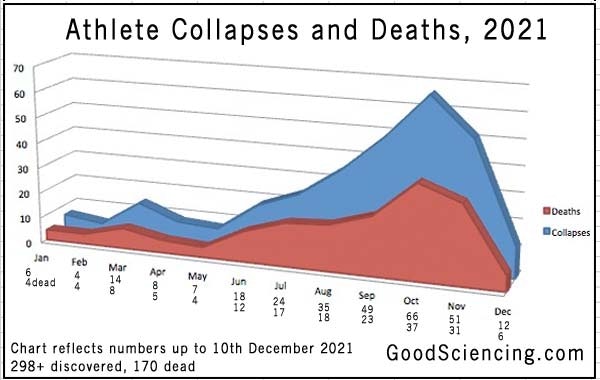

The vaccine is killing some people. This certainly is a statistically small number, but it is happening nonetheless. (I personally know one person who died within two weeks after a shot. I also personally only know one person who has died of COVID, though I am unsure if he was vaccinated or not.)

You’ve probably seen athletes dropping dead on the field and the court. I wish this chart went back to 2020 to show the comparison, but you can see the baseline rate pretty much from the first months when the vaccine was just starting to rollout.

Some people are claiming that the shot is a death sentence, just delayed for most with prion disease or something like that. I don’t believe that is true overall, thankfully, but there is zero doubt it is for some.

Reducing population is the desire of some in power. That is clear. The evidence is out in the open if you simply look. This is not only done by the vaccine though.

What I didn’t see at the time was how it has dangerous side effects that may have been killing people in the hospitals where COVID would be blamed instead of the deadly drug. This is well covered in RFK Jr’s book.

I fear that Pfizer’s Paxlovid and Merck’s molnupiravir might end up doing the same. Think about this from the nefarious viewpoint. What if you could make money killing people, while being able to blame the deaths on the disease which generates more fear? It’s evil genius. And it’s not just today. AZT during AIDS was exactly that.

These vaccines likely are going to render many sterile. Miscarriage rates are up and IVF clinics are reporting problems. There is a history of sterility vaccines being worked on, again covered well in RFK Jr’s book. The long tail of seeing vaccines as causative means that most people will miss it.

But the big killers across time have always been starvation and war. If the economic collapse occurs in 2022, there will be the former. If the revolution really ramps up we’ve got to be careful of the latter.

These stats are hard to get, and not fun to think about, but my prediction is more overall death in 2022 than 2021. Just like there were more COVID deaths in 2021, despite the vaccine, then in 2020 when there was no vaccine. (Of course, this is the unvaccinated people’s fault, not the failure of the vaccine say the cognitively dissonant.)

Governments are going to shift more totalitarian by necessity.

Courage and pushback will grow.

Revolutions are going to start.

Wargamers going to rollout the next big real thing.

Economics going to inflate and eventually collapse.

And eugenicists gonna genocide.

Despite all this, I think 2022 will be a good year.

Forcing into the open the batshit craziness and totalitarian nature is necessary for the cleansing that must be done. It’s going to be a rough ride but that is the nature of a healing crisis.

Feel free to agree or disagree or add your own prognostications in the comments below.

I’ve been talking a lot about cryptocurrencies lately and will continue to do so. One of the big topics that stops many people from getting involved is how safe are they?

Safety is an important question, but I want to change tracks a bit. How safe is your money in general? How safe is the ever-growing economic bubble we all live in? (Like a fish in water, most can’t see it.)

In this article we’ll be looking at several areas to dispel the myths of safety we are supposed to believe in, showing that such safety nets that we assume exist may not be there when we expect them to be, especially as this country continues to fall apart.

“To understand the state of our currencies, it is essential to realize that we live and transact in a transition time between two systems—amid a global currency war. The first system is the U.S. dollar, which has served as the global reserve currency since World War II…The second system is ‘in the invention room’ as we speak. Numerous parties throughout the developed and developing worlds—including members of the dollar syndicate—are attempting to bring up new digital transaction, payment and settlement systems…these unfolding developments represent a complex, confusing landscape for even the most sophisticated financial observer…The important thing to understand in this transition period is that many members of the global leadership do not intend to bring up a new currency system for use by the general population. Instead, they intend to end the use of currency as we know it, as part of a radical reengineering of our existing laws, finances, and culture. Their goal is the end of individual sovereignty—managed with technocracy and transaction systems that can operate without markets or currency in the classic sense, integrated with other heretofore separate control systems.”

I’ve touched on many of these areas before but aim to give a bigger picture looking at the unsustainability of our current system here in a two-fold way:

The system at large

Your dollars within the system

How Safe is the FDIC?

FDIC, the Federal Deposit Insurance Corporation, is what backs every bank account to the tune of $250,000 nowadays. Your money is safe in banks because the government guarantees it.

As their website says, FDIC is “an independent agency created by the Congress to maintain stability and public confidence in the nation’s financial system. The FDIC insures deposits…”

But do you believe in a guarantee when you know that our government is run as a criminal organization?

(After all, the Constitution is supposedly a series of government guarantees, but we can see these guarantees are all being whittled away.)

Here’s a history lesson. Another US insurance organization, the Federal Savings and Loan Insurance Corporation, became insolvent in the 1980’s savings and loan crisis.

It was “recapitalized” with taxpayer money, $15 billion in 1986 and $10.75 billion in 1987. Despite these efforts, by 1989 it was still broke and was gotten rid of. Its responsibilities were replaced by the FDIC. That crisis ultimately cost taxpayers $150 billion dollars.

So let’s look at the FDIC.

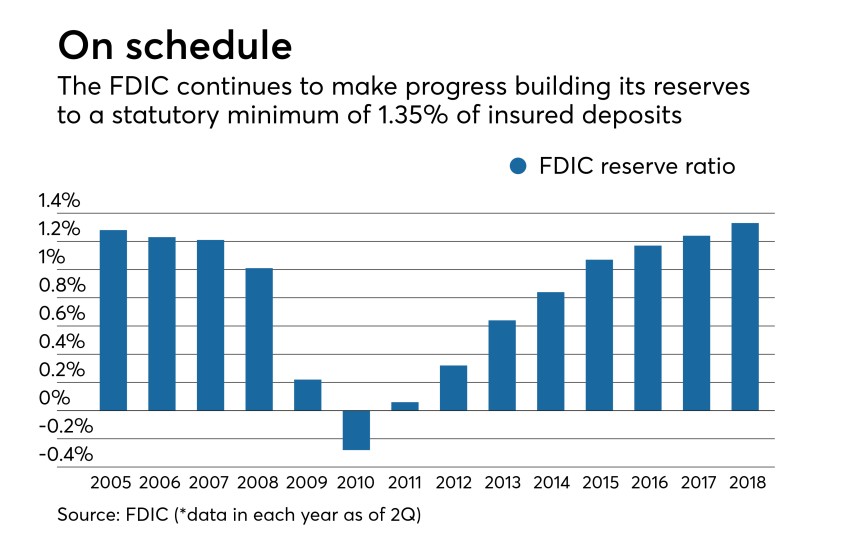

Did you know that the FDIC was $8 billion in the hole back in 2010 from the last big crisis and bank failures? They’ve since reversed that, but just how exactly are they insuring that your money stays in bank accounts when they themselves haven’t always had it?

Nothing fundamental was fixed after the 2008 crisis. The problems are all bigger now…just elsewhere besides mortgages.

That covers 400,800 accounts at the $250,000 limit. Of course, most people don’t have that much money. But of those that do, many have several different insured accounts at different institutions.

If a crisis bankrupted a federal insurance institution before, what are the chances of it happening again? I’d be willing to bet on it.

Bank Runs?

Investopedia defines a bank run as the following: “A bank run occurs when a large number of customers of a bank or other financial institution withdraw their deposits simultaneously over concerns of the bank’s solvency. As more people withdraw their funds, the probability of default increases, prompting more people to withdraw their deposits. In extreme cases, the bank’s reserves may not be sufficient to cover the withdrawals.”

If there is a demolition of the current system (whether controlled or uncontrolled) this is a potential consequence.

Oh, and regarding those reserves? I reported on this back in March of 2020. The Fed stated: “As announced on March 15, 2020, the Board reduced reserve requirement ratios to zero percent effective March 26, 2020. This action eliminated reserve requirements for all depository institutions.”

Banks aren’t required to hold any reserves anymore. Suspicious timing…What does a pandemic have to do with bank reserves? There’s no answer on the surface level which is why such a policy change got no mainstream coverage. But below the surface…everything.

I guess if we go fully digital there can’t really be a bank run?

…at least no one will SEE the bank run since all they need to do is transmit some bits over there and say we’re not allowing cash transactions anymore (because of the virus of course).

The FDIC is there to ensure that bank runs don’t happen. But what if the system is pushed to the point of collapse where FDIC goes with it.

The “good news” is there is a solution…

The Solution to Every Problem – Print More Money

The answer to any and all of these questions is to print more money. That seems to be our economic plan. That is what Modern Monetary Policy says to do.

Yes, the FDIC could be rescued from ANY failure by printing more money. But understand that comes at a cost, the dollars we all have get debased further.

Printing money acts as a hidden tax on the people. Congress doesn’t have to approve it. (Technically in the Constitution they approve budgets but that’s hardly how it actually works now.)

They don’t take it from you like they do with taxes, instead they just make any dollars you hold worth less.

In fact, with almost everything listed here the answer may be the same. Got a pandemic? Print more money. Going to war with China? Print more money. Climate change? Print more money. Alien invasion? Print more money.

It’s the magical solution to any threat, real or spun.

Why would they debase a currency like this?

Understand that by printing more, the bankers and their political, intelligence, non-profit, and corporate friends can gobble up assets better than anyone else. They get the benefits of new money created out of thin air, while it negatively impacts all the other existing money in value.

This creates bubbles. Bubbles always pop. Whether engineered or not, growing bubbles contribute to economic inequality. The rich get richer. The poor get poorer.

…And the bubble popping is another crisis which gives license to print more money.

It’s a hell of a system. Kicking the can down the road like this, without any fundamental reform, only delays and grows the problems that will have to be dealt with at some time.

Many in the financial space liken this money printing to be hooked on crack, heroin and meth!

The Debt Death Spiral

A zombie company is defined as a company that either needs bailouts in order to operate or has debt that it can pay interest on but not principal. While some can get turned-around most ultimately go bankrupt.

It must be great to be too big to fail, right?

Bloomberg reported that since the pandemic started over 200 large corporations, with over $2 trillion in debt, were added to the list of zombies list. This included Boeing, Delta, Exxon Mobil, Carnival, Macy’s and more.

Even more important than companies…what happens when the US goes full on zombie government?

This was BEFORE all the pandemic bailouts. Are we already a zombie or will it be in 2022 or 2023?

I suppose they can just print more money to handle the debt, right?

How Safe are 401K’s?

Most IRA’s are only taxed when you withdraw from them. (Roth IRA’s being the exception, where you pay taxes before contributing and then can withdraw tax free.)

Here’s a question to ask yourself. By the time you’re taking money out, do you think taxes are going to:

A) stay the same? B) go lower? C) go higher?

Really take some time to ponder that question. They might just print money, but I’d also be willing to bet taxes will be going up.

With government spending ramping up, likely to ramp up even more, where do you think that money is going to come from?

And if you think only the richest people are going to be taxed, I’m sorry but you’re not paying attention. Yes, there are things like the proposed California wealth tax, but the brunt will always fall on the middle class, while the elites have their ways of avoiding the worst of such policies. (After all, they’re paying the politicians to write the rules.)

I know some of my readers are already retired. Others won’t for decades to come. But you really need to project out where you think the USA is going for this.

Do you even own Your 401K?

Can the government just take your 401K? Not with current laws. But laws can change. Apparently, this would take going through Congress, the President and the Supreme Court. Again, if you think this is impossible, I ask you how many impossible things happened in 2020?

My friend Garrett Gunderson first clued me into this. In a Forbes article he wrote, “Did you know that your 401(k) does not even technically belong to you? Read the fine print and you will find that it is what’s called an “FBO” (For Benefit Of). In other words, it’s held in trust by a custodian on your behalf and is subject to a slew of government regulation and change. It’s essentially a tax code. If history proves to be a reliable guide, 401(k) funds are therefore in great jeopardy! In the same way that the government raises and lowers taxes at their whim, it can change the rules and take the money that you so diligently saved.”

But realize that is just one means of transferring wealth.

Even if 401K’s aren’t touched, we know that the markets are largely rigged. I don’t know if it is completely so, or just partially, but insider’s do have ways of creating, inflating and popping bubbles to their benefit. They can ride the bubbles on the way up and get out before they pop.

In 2008, my mom’s retirement in her 401K was cut in half by the stock market crash. She passed away before she retired (because of the poisoning of our environment and ineffective medical care) but I know she was worried that she wouldn’t be able to retire when she planned to. She’d have to work longer because of the market of which she had no control. She just trusted that her 401K was a wise choice.

Is the Stock Market Safe?

We saw stocks drop significantly in March of last year, only for it to resume going to new highs. The stock market is thriving only because of the money being pumped into the system. But that won’t inflate it forever.

But what goes up must come down.

There will be another bigger and prolonged crash at some point. Guaranteed.

Most people have ZERO control over their 401K’s, all of which is in the stock market. It’s managed by some mutual fund, typically paying a hefty but hidden fee for the privilege.

A better option in my mind is a self-directed 401K. This way you can do much more than index funds in the stock market. With the right setup you can invest in businesses, real estate, precious metals, foreign assets, and even cryptocurrencies.

Personally, I don’t have a 401K. And I don’t ever plan to. Truthfully, I don’t even buy to the idea of retirement for myself. That doesn’t mean I’m not working for my future; I’m just using different vehicles to do so.

The fact that you don’t actually own it makes it highly suspect in my mind.

What if the government decides that all white people need to pay reparations for their whiteness and the 401K is a good way to do that? Because obviously, if you have a 401K you’re privileged and engaging in white supremacy.

I only say this in partial jest with the direction things are going…After all, if math can be racist, all things are on the table!

It’s not a far leap from the right answers in math being racist, to any financial literacy and therefore retirement funds being racist.

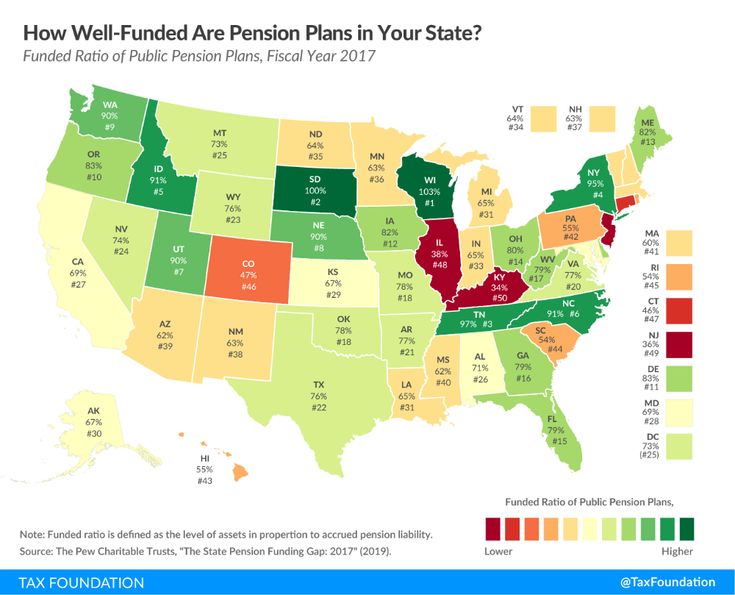

How Safe are Pensions?

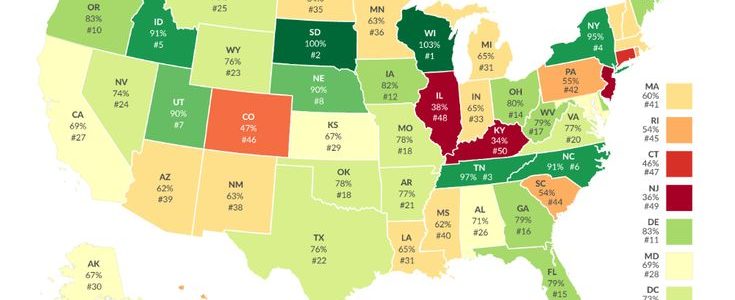

Virtually all the state pensions are underfunded.

Here’s a graphic from 2017 showing the average state is short about 30%. Some like New Jersey are deeply in the red. Only two states, South Dakota and Wisconsin were fully funded.

That’s government workers. What about private pensions?

There are many more examples of such actions the world over. Do you think this kind of thing is impossible within the USA?

Is it American exceptionalism alone that protect us?

A good question is why are these pensions underfunded? The government is full of crooks that are already robbing us every chance they get. For the sociopaths involved, they’ll continue to rob us of anything and everything with whatever they can get away with. Of course, there are ways of getting at pension money, just like social security which will be bankrupt within a couple years.

Yes, there is tons of government waste. But so much more of this money is going into the pockets of corporate partners. (Like all those private prisons and contractors. It’s a very profitable system and has been for decades to throw victimless criminals in jail.)

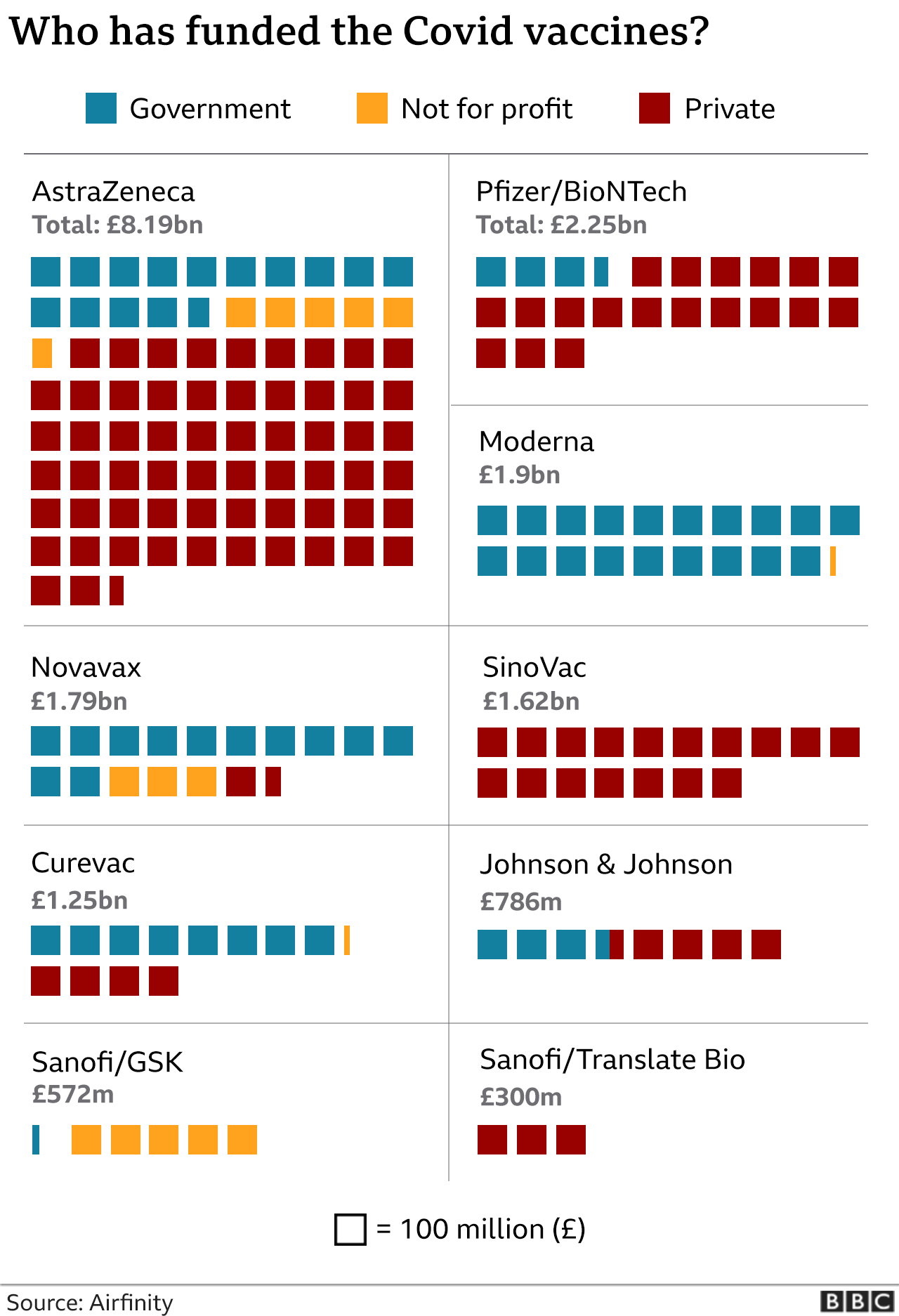

Moderna was almost 100% government funded, the last little bit kicked in from…you guessed it, the Gates Foundation.

Public funding, yet Moderna gets to keep the profits private. Furthermore, the private companies have zero product liability, that falls on the government too. That’s one a hell of a deal!

This is how the organized criminal syndicate runs. This is why the system is so overburdened with debt. the criminals loot money from taxpayers to pass back and forth between each other.

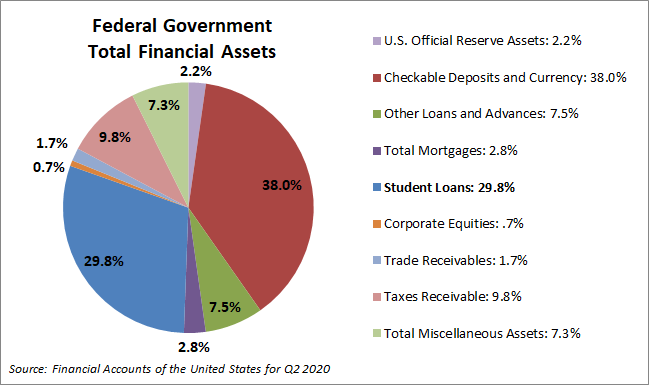

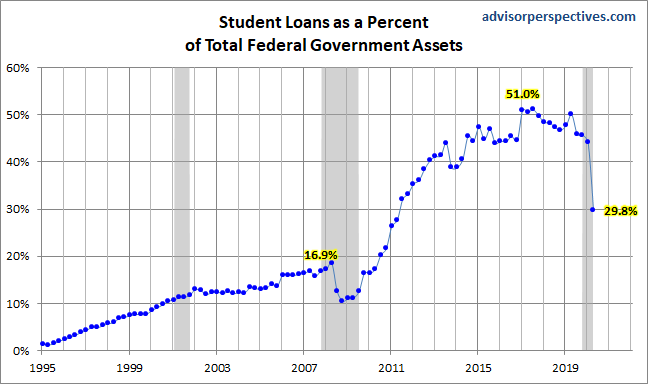

The Student Debt Bubble

Student loan debt makes up almost a third of the assets of our government.

And previously it was even a larger chunk, over 50% of governement assets!

Student loans are certainly a racket that screws over people big time. I’m not trying to debate that here.

But just looking at it from the other side…what happens when you get rid of the biggest asset held by a government quickly going bankrupt?

I suppose you can just raise taxes or print more money to make it up.

The Dollar Continues to be Downplayed Across the World

The discussions between Russia, China and other countries about moving away from the dollar continue to occur. This has been going on for years now.

Recently, Nikkei Asia reported, “Russian Foreign Minister Sergei Lavrov began a visit to China on Monday with a call for Moscow and Beijing to reduce their dependence on the U.S. dollar and Western payment systems to push back against what he called the West’s ideological agenda.”

“Washington has been abusing SWIFT to arbitrarily sanction any country at will, which sparked global dissatisfaction. If China and Russia could work together to challenge the dollar hegemony, a laundry list of countries would echo the call and join the new system,” Dong Dengxin, director of the Finance and Securities Institute at the Wuhan University of Science and Technology, told the Global Times.

But it’s not just our “enemies” saying this…

Mark Carney, governor of the Bank of England said in 2019, “The world’s reliance on the U.S. dollar won’t hold and needs to be replaced by a new international monetary and financial system based on many more global currencies.”

The Coming Shocks

Understand that all this IS the desired outcome by many at the top of the financial pyramid. It allows the cover-up of crimes over the decades and for the global ponzi scheme to continue. And of course, even more power and control.

How? Read The Shock Doctrine. At the very least watch the documentary. It’s a great overview of how things have worked and will continue to do so.

An analogy that I think fits is that we’ll be going through a fall-of-the-USSR type of change, covered about halfway through the video here.

(Though they went “communist” to “capitalist”, while our case seems more in reverse. Those labels aren’t what is most important, but instead to see the commonalities of the economic impacts! In either case powerful oligarchs manipulating the systems are profiting while people suffer.)

By continuing to manipulate markets, loot pensions and taxpayers, this allows for benefits to them today and bigger shocks for the common people later.

Then greater austerity measures will be introduced.

Your acceptance of the totalitarians aims in order to get your handouts are the carrot. Their threats and violence, the stick.

Furthermore, while tested out with Ebola, the bird and swine flus, and even earlier, we can say that “Pandemic Capitalism” is definitely on the rise.

Let me ask a few questions…

Did drugs go away after we declared war on them? (Not when intelligence agencies were funding their black ops by running drugs.)

Did cancer go away after we declared war on it? (Not when the pharmaceutical-industrial-government complex is profiting from both causing and curing cancer.)

Did terrorism go away after we declared war on it? (Not when the military-industrial complex profited trillions.)

We declared war on the coronavirus. Does that mean the coronavirus be gone soon?

It is frustrating to me that people think we’re getting back to normal now.

A temporary reprieve at best. Something that serves to drive us deeper into trance come the next shock.

No, the endless wars (not just physical) have been running for a long time now.

Looking at and understanding the economics of it (instead of getting wrapped up in left/right politics, royal scandals with Markle and Oprah, even scientific debates about health) will give you the most clarity moving forward.

That’s why I’m going to be talking about this even more.

Economics is probably the most useful lens to use to see how the world really works.

My Conclusion: US Dollars are Not Safe

Wrap your mind around that. To keep assets in USD is risky. Once again, I don’t think the dollar is going away anytime soon. It’s a step-by-step process that will unfold over the next several years.

But we are on that road.

The value trend is going down while other assets inflate. (Despite a spike up in USD value recently. That likely has to do with it’s not just the US printing money either.)

Not today, but soon. Perhaps somewhere in 2023-2025 when the US debt stands at $40 trillion, we’re a zombie government, social security is bankrupt, and more has all occurred?

That’s the old system. What about the new?

I found this interesting. Soros Fund Management chief information officer Dawn Fitzpatrick said, “We think the whole infrastructure around crypto is really interesting, and we’ve been making some investments into that infrastructure — and we think that is at an inflection point…I think when it comes to crypto generally, we’re at a really important moment in time, in that, something like Bitcoin might have stayed a fringe asset, but for the fact that, over the last 12 months, we’ve increased money supply in the U.S. by 25%.”

The hedge funds are seeing it. Are you?

An inflection point.

You can literally follow the money right now as we go from the dollar system to the new system.

By that I mean follow the money with your money.

Of course, this doesn’t make cryptocurrencies completely safe either. Far from it. A big crash will come there too. A huge shock which allows the “Fedcoin” to come in is almost assured at some point.

But right now, as it is in the “invention room” we’re FAR from the totalitarian control of the system. We are going through the massive change right now.

So many in the crypto space are against the totalitarian control. But just like everything else, you need to seek to see what is going on behind the scenes.

Most of my assets besides my businesses are invested in cryptocurrency right now.

The writing is on the wall. I’m reading it. I could be wrong about this trend , but I don’t think I am. I certainly benefited by seeing this trend last year.

This gives me time to profit from the asset inflation, the bubble, take profits along the way and get out when the time is right.

To reinvest those profits in my family, my community, supplies and Plan B scenarios. Also to fund those that are fighting the good fight.

You might think me risky to do so…but as I’ve shown, money, the US dollar, is risky right now.

There is risk either way…

But I am trusting in my understanding of the global system! I’m almost all in.

More Spots Opened Up

Reading over this article multiple times, I feel like it may be stoking lots of fear. I sincerely apologize for that, but I think it is best to be realistic even if it looks incredibly pessimistic.

There still is hope that the system implodes on itself allowing people to get free. But even if that happens that too will be rough.

Neither should this be construed to mean that cryptocurrency is some utopian thing that will save us all. I hope I’ve clearly explained how it very well could be the exact opposite.

Still, I do believe their is a window of opportunity here. So much so that I’m not just doing it myself but sharing this message with others.

On that note, my crypto crash course coaching is going great. Several have made their first investments already. (One even got in right before one token shot up in value about 20%. Good timing there.)

As I’m halfway through with several clients, I’ve decided to open up a few more spots. If you’re interested email me at logan@legendarystrength.com and I’ll send you more details.

Even if you don’t work with me I hope you’ve taken this message to heart and are a little better prepared, psychologically…and perhaps financially… for what is coming.

Cast your mind back to the earlier days of the internet. Do you remember when online banks became a thing?

And many people were scared to use them. “How could you trust a bank that didn’t have a building?” they asked.

Your money would disappear into the electronic ethers and you’d have to trust it would be there. I remember when I first signed up for one such bank, ING Direct. My parents thought I was crazy to do so!

That fear seems pretty naïve at this point of the pervasive internet, right?

While I’m sure that some still swear off these things, they’ve become quite common. People routinely do banking, make payments, buy and sell stocks off their smarts phones these days.

But that yield has gone down, closer to what the big banks were giving. One of the places I used, has gone from 1.5% down to a measly 0.5%.

This does not even keep up with the inflation we have going on. The Fed expects 2.4% this year…when we know better than to trust official numbers. (That means it is most definitely higher.)

In other words, holding money in a bank account is a good way to lose.

No thanks, I need a better option.

EnterDeFi

DeFi stands for Decentralized Finance. Basically, this is the ecosystem that has sprung up around cryptocurrencies, most notably the Ethereum network.

By being decentralized it relies on smart contracts and a network of people. There are no centralized hubs like the banks. Instead, there are decentralized applications that build a financial platform available to everyone that operates peer to peer.

Let me check in…have I already lost you?

Do you understand what I’m talking about, or did your eyes glaze over earlier?

In the past months I’ve been having quite a few conversations with different people on these topics. And most simply cannot wrap their heads around it. It is too different from what they know.

New is challenging. Like conspiracy topics they don’t seek to understand because they want to stay safe within their worldview.

I understand it’s not easy to grasp. Yet, that is part of the reason it is important to do so now. Get ahead of the curve not behind, as I talked about in my last post.

Let me take you back in time…

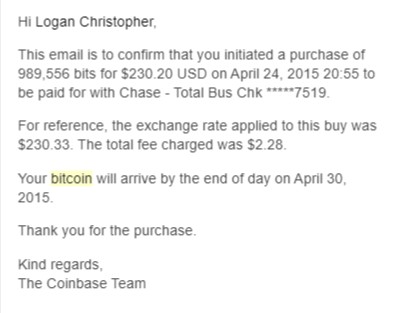

It was 2015 and I had heard about Bitcoin from several different sources. So I dug in. I decided I had to get what this was. It took me some time to do so, looking at multiple sources. It was challenging. But the reward was then I felt like I understood enough that I could begin investing.

On April 24th, 2015 I bought my first ever Bitcoin for $230.20.

Was that a good choice? While I have made many mistakes along the way, the fact that I saw the future coming at least to some degree, and did the hard work of trying to understand it, paid off.

The question is will you do the same if you haven’t already?

The Easiest Way I’ve Found into the Benefits of DeFi…without the Complications!

Why did I bring up online bank accounts? Because it is much the same here.

I’m going to cover more of the complex stuff in the future. But first I want to simplify it for you. Can you get the power (and benefits of DeFi) without actually understanding any of it?

Yes, you can.

What follows is the simplest route in that I’ve found. This doesn’t involve exchanges, setting up wallets or anything like that.

Unfortunately, at this time it is only available for iOS. But they are working on Android.

And that leads me to start with what I do not like. This financial app is exclusively for your smart phone, or iPad. They have a website, but you can’t even login there! You can only interface through the app right now.

Let me be clear, I do not like this trend. Since most of my work is at a computer, I use a desktop. I really don’t even use my cell phone much. But this is where things are going. (And that’s not to mention the whole being controlled by the smart device thing which will grow and grow.)

The good news is that if you can and do use any financial apps, you can do this too.

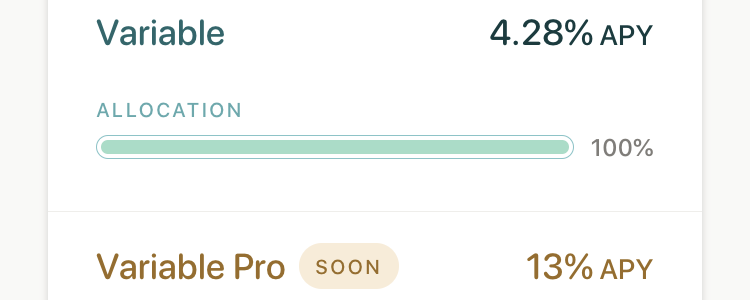

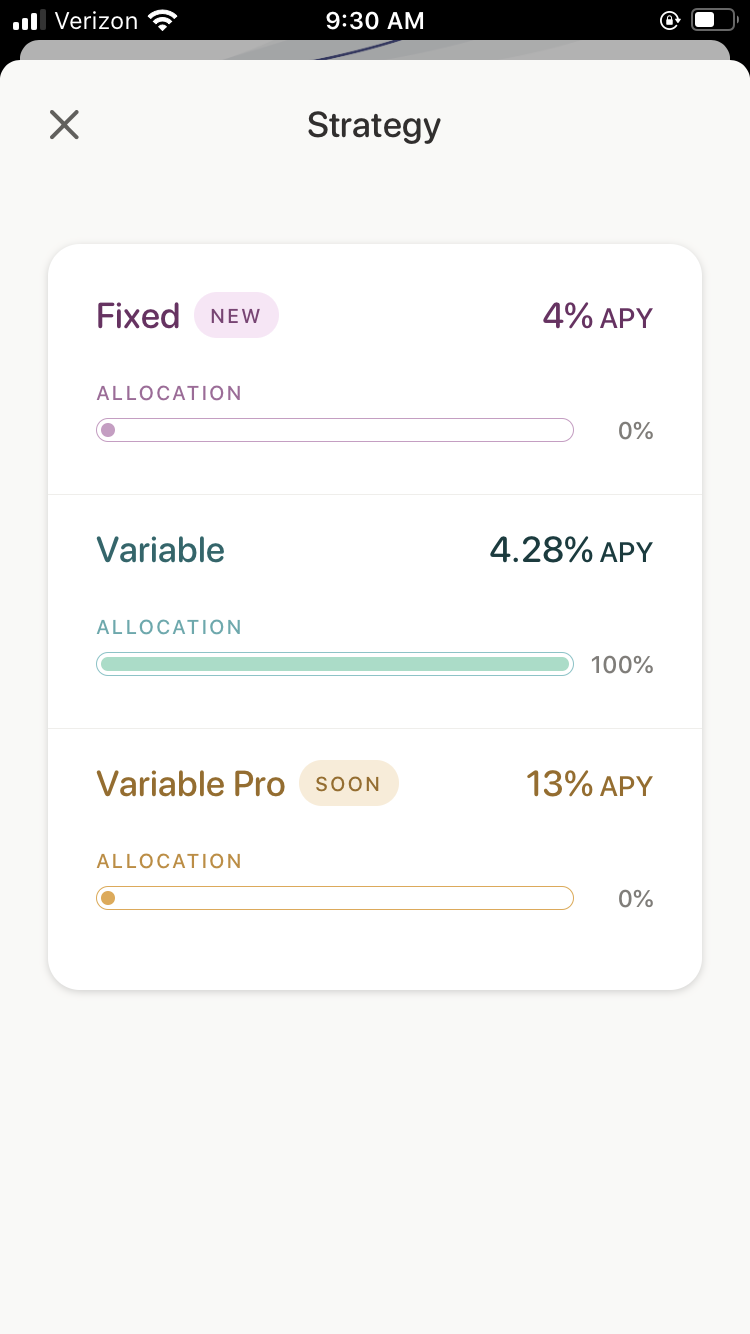

How Would You Like to Earn 4-13% on Your Cash?

Basically, because in DeFi there are ways to earn much larger yields, 5-12% is quite easy, and possibilities of making a ridiculous 1000%+, this company can use the money you save to do so.

And they can give you your cut of 4% for use of your funds.

Here is an actual screenshot from my account. I have only been using this for a couple of months and have already earned more interest than a full year of my online savings accounts with a much smaller balance.

In fact, you can get more than 4%. You can select the variable amount. At the time of this screen shot it was 6.96%. I have seen it move below 4% as well. (The thing is you can click a button and then move back to the standard 4% when that happens too.)

And soon they’re planning on offering even more. This morning I took another screen shot. You can see the variable rate is just above the fixed rate at 4.3%. And they have a Variable Pro rate of 13% coming soon.

So at the very least you’re earning 8x times more than most banks offer. And there are possibilities for much more than that.

This is the power of DeFi…made really simple to get started with.

To understand this, you have to understand more about digital currencies. One thing (of several) that have stopped their widespread adoption is the volatility. The space does go through some wild swings.

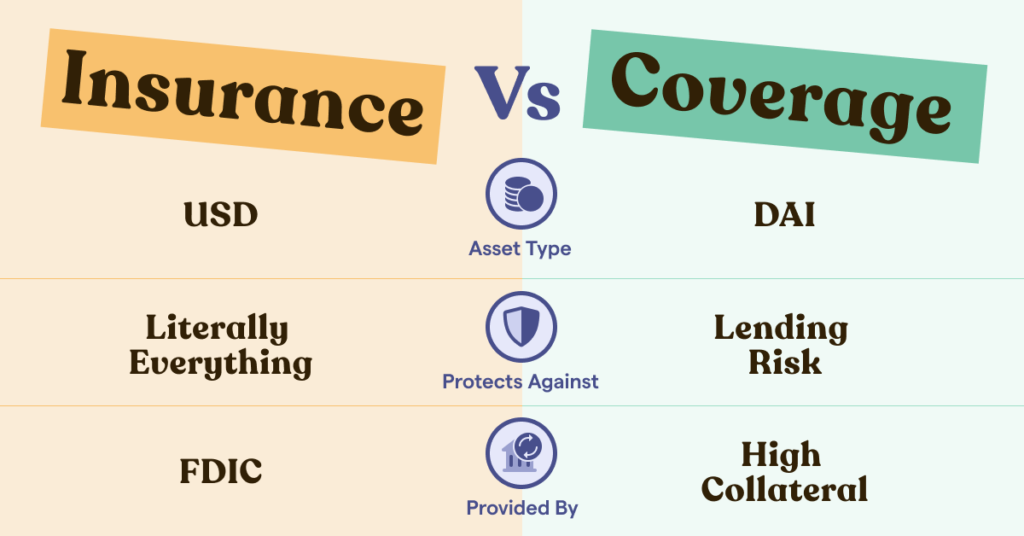

And this is why stablecoins were created. They are cryptocurrencies that are pegged to a (comparatively) stable asset, such as the US Dollar.

These are basically a cryptocurrency versions of the US dollar. Like a digital dollar but typically backed by real cash and audited (PAXOS), backed up by code and a basket of other cryptocurrencies (DAI), or seemingly backed by cash but actually a scam (USDT aka Tether). More on stablecoins including the scam details another time.

In short, these stablecoins are stable in price compared to other cryptocurrencies. Importantly for this topic, they can be lent out in a variety of ways to make money in the space.

With Donut, your cash is converted into stablecoins (DAI specifically) and then lent out for you. You can withdraw your cash at any time.

Is this Risky? Is this Safe?

First of all, this is not FDIC insured. There is no Federal guarantee that your money is protected. (As you might imagine, there are financial problems with this federal agency, I plan to explore in the near future.)

FDIC insurance backs every bank account. But not this.

But the fact that this lending is backed by collateral ultimately acts as coverage, at least to a degree. While there are ways of leveraging such assets, within DeFi lending things tend to be collateralized over 100%. Often 150%. So it is safer in that way.

Donut has been around since 2019. I know that doesn’t sound like much but that is a decent timeframe for a stable company in this space!

Ultimately, time will tell. There is a big crypto crash at some point in the future. Nothing ever just goes up. When that crash occurs does the collateral cover everything so that Donut and their users have zero problems? I hope so. For my sake and theirs.

Ideally, I would like to see even more information on their website including audited reports.

My Use of Donut

I would NOT recommend you ditch any and all other investments and use only this. Far from it. Instead try it out as one place to make use of.

Diversification of platforms is one of my strategies especially in this newer field.

I am actively using Donut as one of my savings accounts. Sure, I can use those funds within the crypto space and make even more doing the lending myself.

One thing I like about this is the extremely quick liquidity of it. You can withdraw your cash at any time and it’ll arrive back to your bank within 1-5 business days.

This is far from the end-all, be-all of DeFi, but I choose to share it as it’s an incredibly easy intro point where you can get some of the benefits of crypto without the hassles of it.

Regardless of whether or not you choose to (or can) use this app, I hope that this served as an intro into the space. Much more to come in the future.

Let me know if you have any questions below.

Disclaimer: This is not to be used as financial advice. Logan Christopher and Legendary Strength LLC are not registered investment, legal or tax advisors nor a broker/dealer. All investment opinions expressed are from personal research and experience. Email and website content is to be used for informational purposes only. Logan Christopher is personally invested (long) in a number of cryptocurrencies.

Remember that people dismissed the internet as a fad. How are they feeling right now?

Sure, there was spectacular flashes and crashes along the way. The dotcom bubble being an early such example. But did that kill the internet?

Look at where we are at today. Everyone holds the internet in their hand or pocket with them wherever they go. To not be connected at an instant is the anomaly.

This is where cryptocurrencies, blockchains and smart contracts are going.

If you’re looking to stretch this analogy further, we are likely in the post dotcom bubble era with crypto.

The internet is established but most people still aren’t using it. This is the time of the mass mailing of AOL discs!

We’re in the spot where many people were still hesitant to buy things or bank online.

We’re in the spot before social media became pervasive.

We’re in the spot before smart phones made the internet ubiquitous.

NOW is the time to get in. Because this may well be even bigger than the internet. That might be hard to believe, but it is the entire global economy in transition.

Just because it might be hard to wrap your head around how such things work, doesn’t mean that its not worth paying attention to.

You may not know the engineering details of how electricity gets generated and everything involved in delivering it to your house but that doesn’t stop you from flipping the light switch, does it?

There are other factors at play that make this even more pressing.

Our Economy is Crumbling

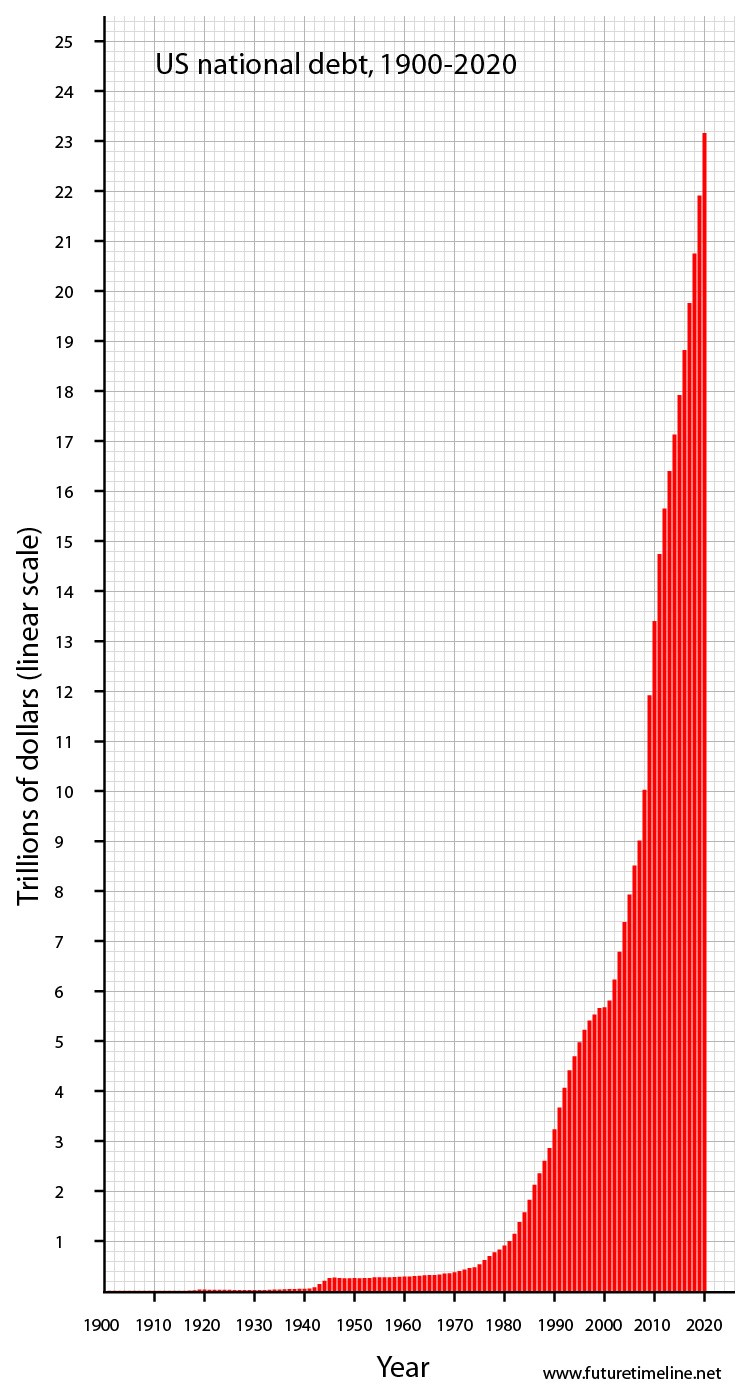

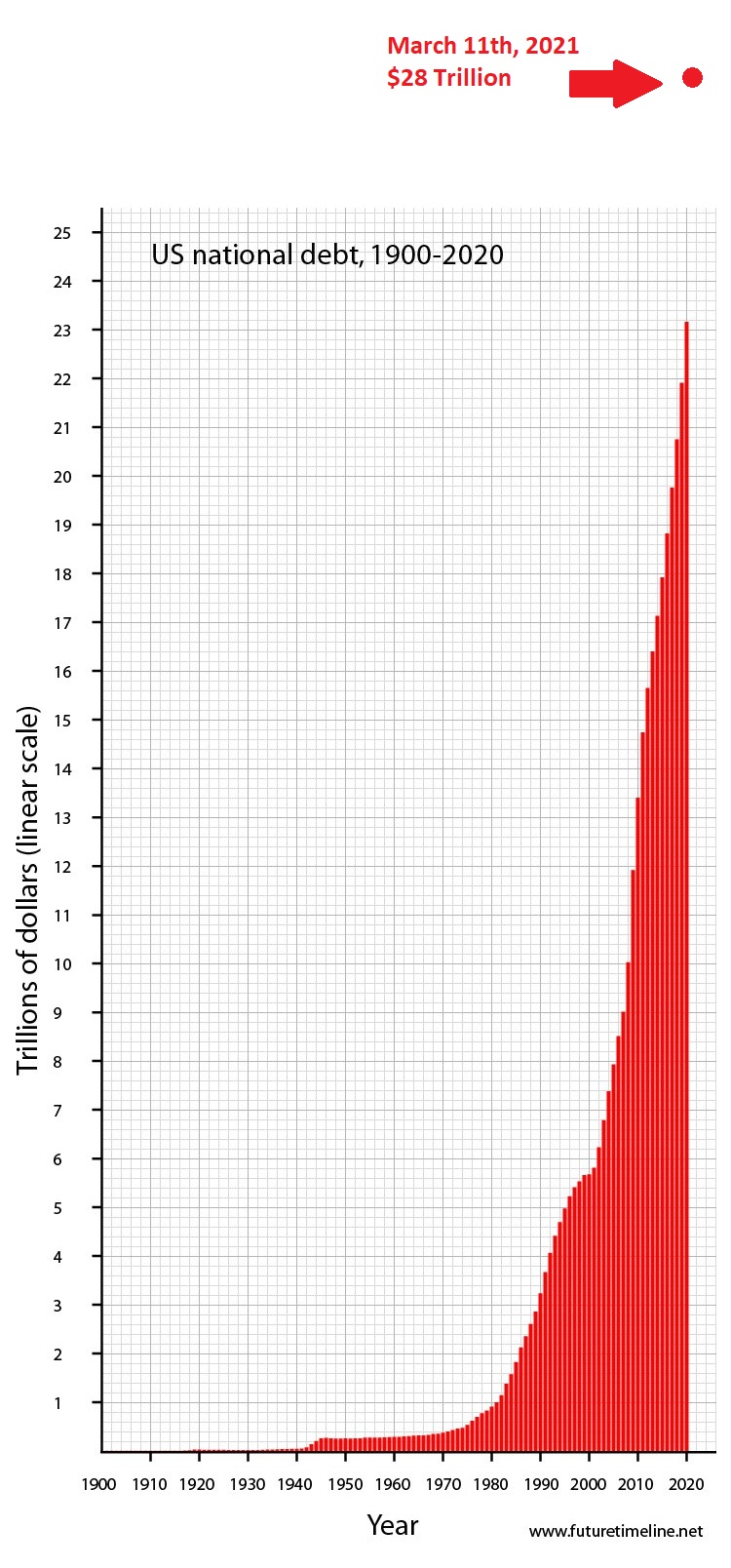

Here’s the US National debt over 120 years…

Exponential growth and hockey sticks are not sustainable.

This image, made at the end of 2020, is already outdated and inaccurate. The chart must be extended to shift into less than 2 ½ months of 2021.

They will continue printing money in ever bigger amounts. Eventually people will lose confidence in the US dollar. Modern Monetary Theory says there is no consequence for printing all the money you want. (How did that work out for every other country that has done that?)

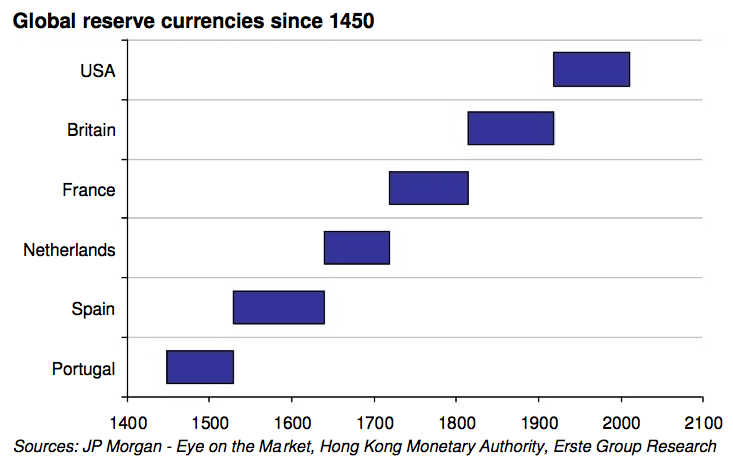

As of right now the USD is still the global reserve currency. Being tied to oil (they don’t call it the petrodollar for nothing), backed by the US army, it still has legs.

Reserve currencies don’t last forever. In fact, they tend to last about 70 years. The US dollar is getting long in the tooth.

This won’t happen tomorrow. But the transition will happen in time.

And when it happens, it may happen FAST.

When that does happen, everything will be disrupted even bigger than what happened with the pandemic.

First bit of advice, do not get caught with your pants down!

Be prepared and ready for this. Even better, be in a position where this works for you.

Are You Winning or Losing from Inflation?

Crazy inflation is already happening…but most people don’t see it, because they don’t understand the bigger picture.

(So many still think the virus is about this virus! The economic magicians wonderful use of misdirection hides their schemes.)

At some point, very likely in the near future, the prices at the store, at the gas pump, and elsewhere will start to rise. In some places they already have.

This will snowball…

Perception is fact in this day and age, sadly. That’s why the news can print or say something the is literally the opposite of the truth and besides a few people screaming about the insanity, nothing happens.

We’re dealing with fake money after all. That is what fiat means.

(I laugh at people who balked at crypto saying it’s just made up. Yes it is…and that comment shows how little they understand our economy and current fiat currency. If you haven’t got that memo, it’s all made up. It is all based on perceived value.)

Most of what is happening right now is known as asset inflation.

Have you noticed real estate prices lately? The stock market? Physical precious metals? And certainly cryptocurrencies?

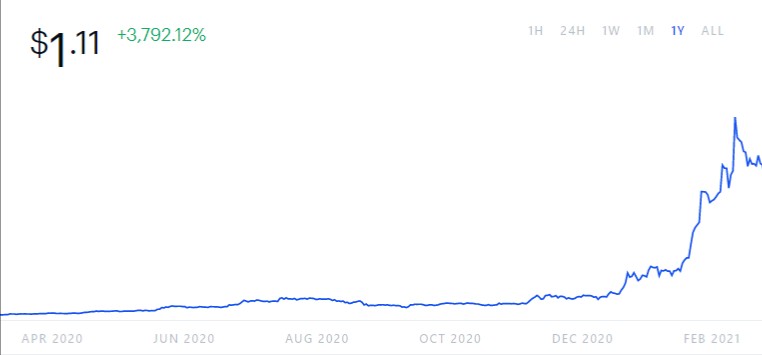

In other words, right now, people perceive certain cryptographic code on a computer called a Bitcoin as worthy of lots and lots of dollars.

90% of the attention goes on Bitcoin. But honestly, I’m more excited about several other tokens.

Here is one of many I got invested in. Some hockey stick charts suck (US debt). Some hockey stick charts rule (anything I’m invested in).

What is the Dollar’s Replacement?

If the dollar is going away, something must come to replace it. What is coming?

The answer should be obvious by now. Cryptocurrencies, in one shape or another. This much is certain.

Based on limitations, it won’t be Bitcoin. Who knows? It might be the Digital Yuan.

There are still hurdles to overcome and details to get ironed out, but we know the shift is here because the technology involved make certain things possible that are not in any other way.

Besides most of our money is already digital.

The “signal” that cash was to be phased out because of the virus, and the supposed coin shortage, should be loud and clear.

Money is flooding into things of value. Some certainly more tangible and more productive than others.

Yet, many think these bits are not productive. That’s not quite correct. There is technology backing them. Productive technology and ideas. Therefore, money will continue to move from the “old system” into the “new system.”

Being faddish, absolutely this will outstrip what is rationally moving in.

But if you haven’t figured it out there is little rationality in the 20’s.

Bitcoin has popped as a bubble three times now. And it’s still around. It is bubbling again and will pop again. But it is not going away.

We had the real estate bubble in 2008. Did real estate go away after that? Not at all.

So my question to you is this…

Would you rather own some of that asset inflation, or have it in areas that are deflating?

I’ll get back to that but let’s talk more financial matters…

Social Security is Bankrupt Guaranteed

Social security will be bankrupt somewhere between 2023 and 2035. The 2035 projection was before the pandemic, but this rapidly accelerated that time line.

This is just one example of many.

The only way the US government can afford to pay it’s many, many liabilities, is to print more money. This means that if you’re relying on those government services, you’re becoming poorer and poorer.

Bitcoin at $100,000 is not because bitcoin is worth necessarily worth $100,000. A large chunk of that is because US dollars are losing value.

So many of us, especially within the USA, are soft. Life has been easy. Comfortable. We don’t know what true hardship is.

…And that makes so many blind to the trajectories we’re on leading us there.

It is tough to learn lessons you don’t have first hand experience with.

You’ve been reading my conspiratorial blog posts here, so you understand some of what is going on. And on that note, the thing I get asked more and more is what do we do about all the craziness?

What Can We Do?

To be honest, these forces are far more powerful and with far deeper pockets than you and I.

Sure, collectively together we are more powerful. But we are NOT acting collectively together. Not by a long shot!

Divide and conquer has worked so well. Why change the playbook when the same play works over and over?

Yes, the sheep could turn on their owners. But it’s not in the nature of sheep to do so.

How many people that swore off of politics, knowing it’s a shitshow, have gotten wrapped up into the right vs. left fight once again because the soap opera theatrics have been cranked up to 11?

I’ll admit it. It drew me in as I tried to make sense of the craziness.

Sure, one side is fighting for more freedom, but in most cases only just enough to make a good show of it. You gotta have your faces and heels. (That’s pro wrestling terms for the good guys and bad guys.)

So what can we do?

You can take care of yourself and yours. I don’t mean this in a selfish manner.

Instead, I mean that the only chance we have to do anything is to accumulate resources which can then be aimed towards greater collective action.

You can increase your optionality. You can figure out your Plan B, C, D and E.

Money is one part of that. Community and other usable skills is another.

Some of the best people I see trying to support collective action…have FU money.

FU money is defined as “any amount of money allowing infinite perpetuation of wealth necessary to maintain a desired lifestyle without needing employment or assistance from anyone.”

Do you?

It certainly makes it easier if you don’t have the regular 9-5, much less two or three jobs.

I don’t see any way around this.

As the saying goes… “The best thing you can do for the poor is not be one of them.”

Granted, that’s just a starting point. Money by no means makes you a good person.

But if we wanted to fight Bill Gates‘ plans…it sure would be much easier if we had Bill Gates’ resources without his techno-morality!

The Opportunity Before the Fall

Crushing you and your free thinking is necessary for the agendas at play.

We are economic men and women, and therefore control of the money is paramount. Always has been. Always will be, as long as money exists in one form or another.

While the totalitarian control grid will seek to wrap money into your digital ID, vaccination passports and more, that is still far off. Years down the road.

Understand that that cannot happen until widespread digital money is used. And we’re still a far cry from that.

(Although the vaccine pass apps are starting up already, Israel taking the lead. There are many steps that are happening quite quickly.)

So there is great opportunity now…even if crypto makes up part of our ultimate prison. You can get in and get out if that becomes necessary.

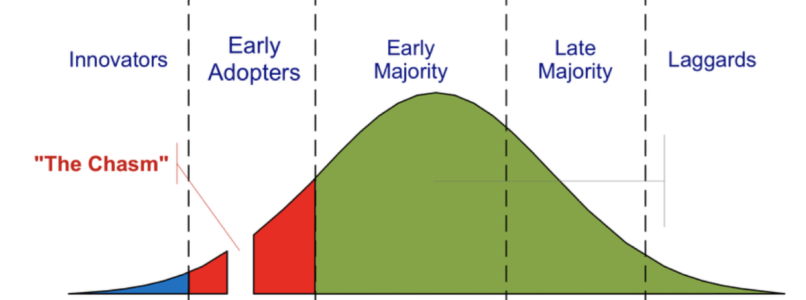

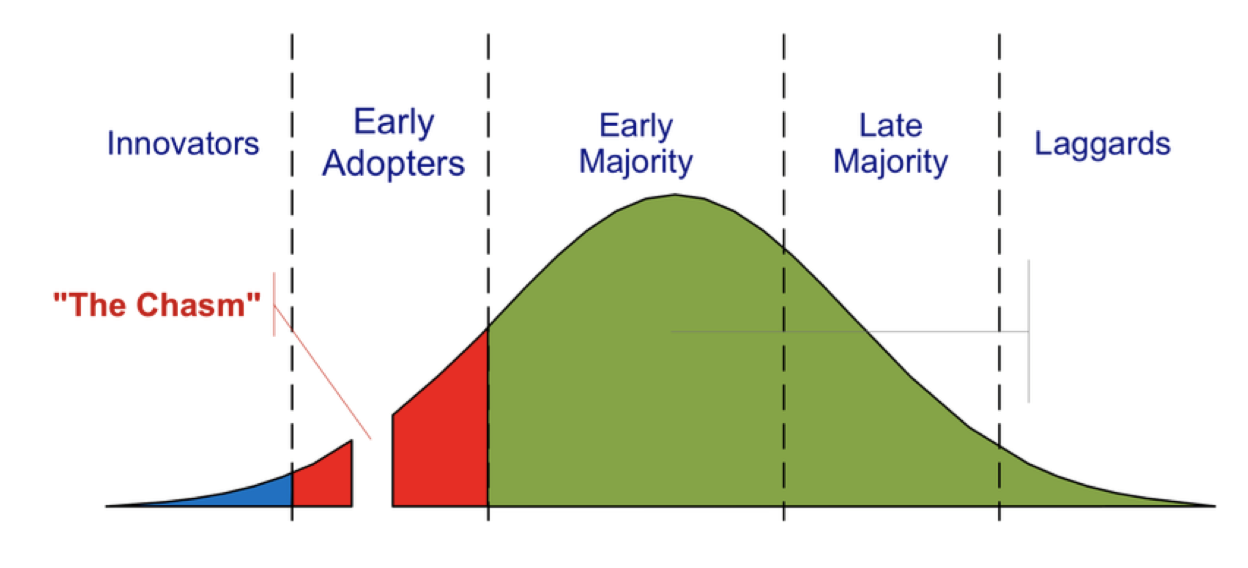

You may be reading this thinking you’re missing out, sitting on the sidelines, but the truth is we haven’t even crossed the chasm of the early adopters yet. We’re a far cry from the early majority.

In other words, there is still time to get in early and profit from doing so. But I don’t think that chasm is very far off now.

The good news is that cryptocurrencies could also be used to free us from the central banks and their government, media, etc. cronies. That’s what decentralized, as in decentralized finance or DeFi, is all about.

Some cryptos are by their very design aimed at getting around such totalitarian systems too.

Thinking of optionality wouldn’t that be great to be setup and proficient in ahead of time?

The elites won’t go down so easily. In fact, I would argue they’re behind many of the most popular cryptocurrencies, a topic I plan to explore in future articles too.

And scams and schemes certainly abound in the area. It is the new wild west. I’m not saying to throw caution to the wind. But I’m also not saying to be complacent.

Crypto is happening. The dollar hegemony is falling. These forces will not be stopped.

A One World Currency?

There will not be a global currency. Not for quite some time at least. There are tons and tons of currencies and will be for some time.

Eventually there will be a few winners and lots of losers. But we’re still far from any sort of consolidation. We’re in expansion mode. (This too, means there are tons of failures, but also plenty of winners.)

You have two choices in front of you:

Accept what is coming. For good or ill, digital currency is the future.

Or bury your head in the sand.

Look, you don’t need to be super technical. I can’t write nor read a line of code to save my life. If you use online banking services and apps on your phone, you have the skills necessary to get involved in investing in crypto.

Sure, it can get complicated fast, but it doesn’t have to be super difficult.

All the luddites didn’t stop the internet. And now my almost 70 year old dad who never used a computer in his life…uses his smart phone regularly. The naysayers won’t stop it.

My argument is that it is worthwhile to hop aboard this train we’re all on. It is worth doing so.

I’m going to be doing more articles in the coming weeks…

Crash Course Beta Program!

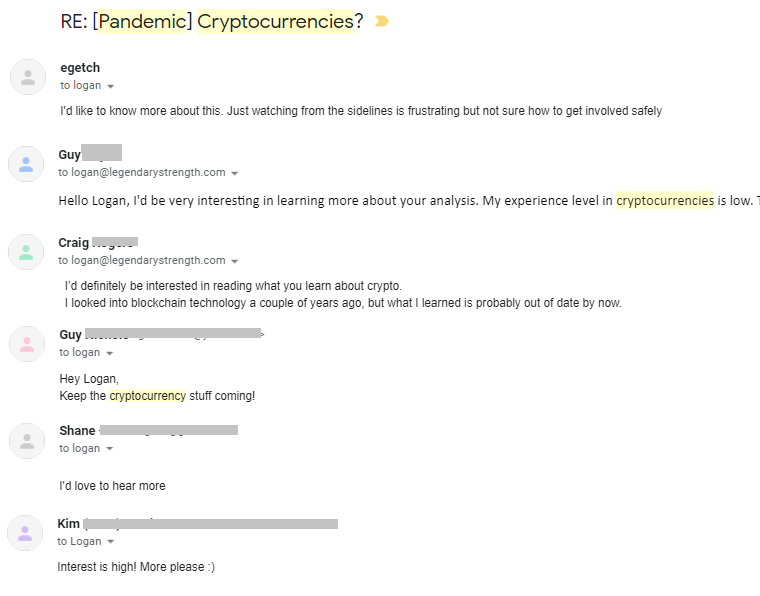

But after I sent out an email the other week asking people’s interest in the topic I was flooded with response. I expected a positive response, but it was huge. Here’s just a small sampling:

The vast majority of people knew nothing and held nothing. That got me thinking.

After careful reflection I’m trying out something new, a beta program to walk a few select people by the hand into this world giving everything I know.

I won’t be doing this for free. And it assumes you have some funds to invest as well. As the plan is to work one-on-one with a few select people, it is limited. (After all I’ve still got my two businesses and family to attend to.)

If that interests you reply in the comments below or shoot me an email at logan@legendarystrength.com with your interest.

I will be putting up free articles soon on the topic as well, but this program is for people that want to get up and running, with a solid strategy in place, as quickly as possible.

Disclaimer: This is not to be used as financial advice. Logan Christopher and Legendary Strength LLC are not registered investment, legal or tax advisors nor a broker/dealer. All investment opinions expressed are from personal research and experience. Email and website content is to be used for informational purposes only. Logan Christopher is personally invested (long) in a number of cryptocurrencies.

How did Lost Empire Herbs get started? Well, it wasn’t even called Lost Empire back then!

Recently, I worked with Starter Story to share the story of the beginnings and how that has led up to today.

This covers some things that have not been shared anywhere else including numbers and stats, what’s worked, what hasn’t and many of the resources that helped get us to where we are today.

And while I’m at it, I’ll also point you to a recent podcast episode I did with Grow Ensemble that also talks a bit about the behind-the-scenes of the herb business.

I’m going out on a limb here and making a prediction for

2019, that silver will rise up in value significantly.

Let me start right now with this…

Disclaimer: This post references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.

I’ve been following silver for years since first

getting interested back in it back in 2011.

It’s been part of my wealth building strategy. In a way, it’s a forced savings. Yes, you can sell your precious metals but there’s an added hurdle that can stop you from doing so.

In addition to buying onto and holding the physical

silver, of which I have some, I use a trading service for easier use. With this

I can automatically transfer money into silver every week or month.

(In the sake of transparency, I do get rewarded for people

signing up through that link. It’s great in that it’s a way to have my precious