We continue from the Introduction to the Money System that Never Fails, with the next part on money offense and defense, and the four areas of wealth.

One of the pivotal books for me, that I read in that massive action period, was The Millionaire Next Door by Thomas Stanley. In it he talks about playing offense and defense with money. This was a big epiphany for me. I started to see that there were different areas of money. Offense could be likened to what you did to get money in the first place, i.e. producing an income. Defense was keeping the money and watching your expenses.

Offense and defense was a good starting point. But it became even more apparent when I added upon this idea and realized there were essentially four areas of wealth.

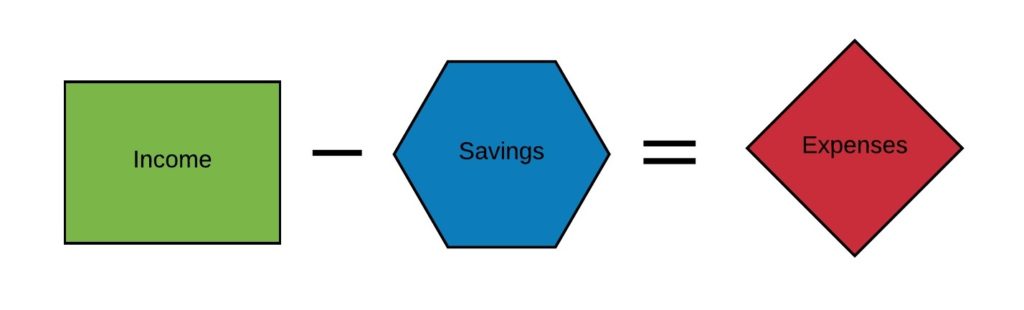

1. Income

2. Expenses

3. Saving

4. Investing

It seems so obvious now, but I didn’t see anyone specifically point this out. Understanding these four categories of money is the foundation to this system.

Finally, this explained why people can have huge incomes and still end up broke. Lots of sports stars and celebrities are great examples of this. The first area is great but all the other three are not. As soon as the big income goes away they’re left with nothing because they’re not truly wealthy. One strength, with three weaknesses does not equal long term success.

It even explains why some people living on meager wages can still end up with large amounts after many years. Income may not be great but the others are even more important. Still I wouldn’t necessarily call these people wealthy either.

It was another epiphany to me to realize that with just minimum wage, you could become a millionaire, just by saving and investing.

At $7.25/hour, 2080 hours worked in a year is $15,080. Saving 10% of this would be $1,508 per year. Invested into something that provided a 5% annual rate of return, it would take 72.37 years to meet this goal.

Yes, that is a long time. And I’m guessing you don’t have that long to wait. But I’m willing to bet if you’re reading this you make more than minimum wage. In California, the minimum wage is raising up to $15/hour soon. In a year this is $31,200. 10% of that is $3,120. Invested at the same 5% annual rate it takes 58.1 years.

This shows that it can be done, showing the importance of savings and investing, and the commonly touted magic of compound interest. But the trick is, if you also optimize your income, then save even more, and invest even better it can all be done far faster, and yield even bigger results.

This is just an extreme example, meant to show you the possibilities. Something to think about is how much money has passed through your hands over your lifetime so far? How much more do you think will happen over time?

If you want to look at other similar calculations you can use this online duration calculator.

Not understanding these four areas of wealth is probably the biggest setback in any money or wealth program or coaching because they are incomplete.

But what happens when you optimize all four areas? Magic!

Each area has some unique traits that best help it out, that are not in the other areas. Each area has specific habits you should do, which are not in the other areas. The good news is that you’re probably doing okay in some areas but just one or two of them falls short.

We all have our strengths and our weaknesses. In this case it is important to play to your strengths, but also to shore up your weaknesses too. The star ball player will be great off with that amazing income, if they make sure the other areas are taken care off.

Thus, when it comes to crafting your wealth plan you must include each of these areas. And each one will have goals and action steps for you to take. Let’s make sure you’re clear on what these four areas are:

1. Income

Money coming in. For a business, this is revenues. Personally, this may be an hourly rate, salary, royalties or whatever else. It also includes selling things, or services whether at a yard sale, on eBay, or wherever else.

2. Expenses

Money going out. Money is used as an exchange of value, so this is where you spend it on stuff. Of course, this occurs both in businesses and personally.

3. Savings

When you get income, it is turned into savings. Most people do this backwards, which is why they don’t have savings. More details on this in the next section. Also note that different types of savings are used for different purposes. Specifically, I consider savings when money is transferred from the income/expense account to a savings account for a specific purpose.

4. Investments

Money from income or savings can then be turned into investments. Active investments are those that generate more income. While you can invest in things like precious metals, these are stores of value, and don’t actually generate income, so these are passive. Understand this difference between active and passive investments.

All of these can be further broken down into more categories. But if you just get these four areas, and the differences of each, you’re ahead of where most people are at. A lot more on each of these to come next.

The Money System That Never Fails is now available in paperback and Kindle at Amazon.