The 5th Generation Warfare is vast. And you’re not schooled in it.

You’re up against politicians that don’t give a damn about you. Armies of lawyers, lobbyists and PR agents who operate the corporate side. Data analysts and psychological operations experts working full time in the fusion centers and intelligence agencies to sway your mind. Not to mention occult magicians doing some sort of dark work that aids in this in various ways!

What is a person to do about all that?

Instilling demotivation, apathy and hopelessness against your enemy are always part of the art of war.

There are many fronts in the global war. The ones that come to mind:

Culture

Economics

Healthcare

Legal

Political

Spiritual

Psychological

Media

Environmental

Physical/Kinetic

Cyber

In most cases these will be mixed and matched. For example, there could be a legal fight regarding healthcare, where opinions are shaped on way or another in cyberspace, with the psychology and spirit of all involved.

What we’re up against is vast. No one person can do much against all of it. The good news is that is not your mission. But you may be able to do something against SOME small piece of it.

First, let’s look at the big picture. As I’ve said before, the hard part about this war, is most people don’t even realize they’re in it, nor what they’re fighting against or for!

The Inhuman Agenda

There is what I like to call the inhuman agenda aiming at total enslavement of humanity. It is inhuman in that it goes against the principles of humanism. And it is inhuman in that, I believe, what drives it comes from dark forces beyond mere humans.

To overly simplify the inhuman agenda we can look at it’s technocratic aims. These are easy to see as they’re all talked about openly, with many steps already made towards them.

The overall technocratic agenda involves having a digital ID that is tied into CBDC’s (central banker digital currency), vaccine passport, a social credit score and a carbon credit score. That gives the controllers damn near near total control because of the ability to steer and even shut down the economic life of each individual person.

There is clear evidence that all of that is in play. In the words of H.G. Wells, it’s an “open conspiracy”. If you need the facts surrounding this, I’d point you to Pseudo Pandemic by Iain Davis as a good primer on virtually all these subjects.

(The agendas of depopulation and transhumanism are related but can be seen as somewhat separate from these so won’t be addressed here.)

Understand that getting this “digital prison” put in place is for the technocratic elite to win the war.

All this to say that dismantling the pieces of this plan is required by the people, for them to win.

Leverage and Weak Spots

Not only MUST the battles be waged here, but in some ways it is quite nice that they are. By that I mean because we have leverage against these specific points in that very few people want these things at all.

The majority of people believe in something called rights, to bodily autonomy, to privacy, etc., that stand in stark contrast to vaccine passports, social credit scores and the like.

A few centuries of talking and striving for inalienable rights, even when falling far short of such ideals, have led many to desire more freedom not less.

It takes a LOT of propaganda to make people willing slaves, especially on that level. The accelerated push towards these even more inhuman things makes such propaganda seen for what it is by more and more.

Therefore, it is actually easier to fight against some of these things than certain other issues. There is leverage in some of these fronts.

Defense and Offense

The inhuman agenda is a game of inches. These technocratic forces have power and are willing to do what has been called the totalitarian march. This always involves going two steps forward, one step back. Floating trial balloons, observing and adapting from there.

When there is pushback from people, they cool their jets. They look for a side-door entry in. Often times they bide their time until later, until the next emergency allows them to ram something through.

Technocracy has been talked about for over one hundred years. Such powers have been patient in moving this plan forward.

Therefore, we need to not only push-back but reclaim lost ground.

The latter is what I’m calling going on the offense.

Because their offense is non-stop. California just signed into law that if any doctor dares commit Covid heresy that doesn’t recognize the scientism-dogma they can be excommunicated.

I mentioned this a little bit in Strategic Relocation. Such battles are much more likely to be won in certain jurisdictions over others.

Defense and offense means to withdraw economic support from anyone that furthers or supports the inhuman agenda, and to support those that oppose it. Witness the closing of Paypal accounts by many after their $2500 fine for misinformation policy.

Much more on these topics in future People’s Playbook articles.

Picking a Battle Front

You must choose your front(s) wisely.

Like in real war, be wary of trying to fight on too many fronts at once! Spreading your resources too thin is a good way to lose ground.

Your resources include:

Your Time

Your Attention

Your Money

Your Efforts

Your Network

Your Organizations

What can you actually do?

Where can you lend a hand?

What specific area calls out to you most of all?

What place is of high leverage that more people need to rally around and attack?

Sometimes it is not you that does the choosing, but the front chooses you. Like those who watch their loved ones become vaccine-injured or even die. A very unfortunate calling, but a calling nonetheless.

I got into health for a variety of reasons. My businesses are involved in the space. Therefore, it makes sense for me to focus on that space, which is why I have.

I plan to continue to focus my efforts specifically on the battlefront of mandatory vaccines and vaccine passports. I think this is the highest leverage spot where the tide of war is turning in that public opinion is failing. Not only against the COVID vaccine, but the entire corrupt vaccine industry to a lesser but significant degree.

They’re propping it up with everything they can, so the powers that be still control the narrative, but it is falling apart. More outright censorship is needed to hold the information battlefront line.

It is my opinion that if one area like this, just one area, where fraud has taken place for over a century can be beaten, then the whole house of cards will begin to come down.

Now’s the time for a continued strong defense and even more offense.

Parallel Systems

Building parallel societies and systems covers a whole range of other ways to go on the offense. Not just retaking lost ground, but this can be thought of as basically creating more and better resources for the war effort.

To is to increasingly fight FOR something, not just against.

For what? Again I list…

Culture

Economics

Healthcare

Legal

Political

Spiritual

Psychological

Media

Environmental

Physical/Kinetic

Cyber

As all current systems are corrupted, new systems that are not corrupt, and better yet built towards an ideal of incorruptibility are crucial.

This wisdom of Buckminster Fuller applies here.

Though, as should be clear from what I’ve written so far, since we are at war, fighting against the old system IS necessary in my opinion. If nothing else, it gives us more time to create the new systems. But fighting can’t be the only thing.

Some may choose to fight more. Some may choose to build more. Some will do both.

Understand that we can’t simply beat the inhuman agenda, with a void to fill its space. It will always keep coming back, that is at least until much better systems, much more human, are in place.

Next I want to cover a few other battlefronts that have my attention…

Child Abuse Battlefront

The Jeffrey Epstein saga gripped my attention. For whatever reason it hooked me in and led me into a deep exploration of what it all meant. This led me into understanding the sick roles of child abuse, sex trafficking and blackmail as part of our corrupted systems.

This involves the darkest parts of humanity which causes most to look away and pretend it doesn’t exist. That is cowardice hidden at the subconscious level.

Because this is a part of the twisted power elite system, this front too must be dismantled to win the war. More awareness is growing, though it does seem a harder front to win.

While I am constantly learning about this topic and contribute monthly to Operation Underground Railroad, I am not clear on the best next steps to take on this front. I have faith that more clear actions will make themselves known in the future to me.

Economic Battlefront

Following the money was an important strategy in understanding our health and medicine systems. After exploring this for a long time, I realized I needed to understand money and economics, including the corruption in these systems much better.

As money drives all other systems, it is good to gain a foundation of understanding such. Without such a foundation, I would argue, it’s easier to be led astray in any other front for a variety of reasons.

There’s also the fascinating technology of cryptocurrency. CBDC’s are something to fight against because of the increased control in the hands of the technocratic elite.

On the flip side, there’s a good case for decentralized technology such as Bitcoin, Monero, etc. to actually support the people too. However, these being digital, we must be wary of how even seemingly useful systems could end up aiding in building the “digital prison”.

Many future articles will cover the economics of the People’s Playbook. After all, war is expensive! And money flows are a big part of the supply lines of 5th Generation Warfare.

Woke Battlefront

Are we really arguing about whether men can get pregnant or not?

Apparently…

From Critical Race Theory to pushing irreversible hormonal treatments and surgeries onto children, this area certainly garners a LOT of attention in the culture wars.

And it is my opinion that most of it is misdirection. Not that it isn’t important at all, but it pulls time, energy, effort, attention and intention away from the other things that are quite a bit more important.

Wasting breath going up against racist anti-racists stops people from seeing the digital prison that is coming. Unfortunately, these fights must be fought, primarily in schools if you don’t want to see children indoctrinated in this way.

The Meta Battlefront

No. I’m not talking about Facebook, though that certainly could be considered a battlefront all on its own.

I’m talking about “meta” as meaning over and above. What are the systems, structures, ideas that apply across all domains?

Like the structure behind practicing or habits, I’ve always been interested in looking across contexts. This is a strength of mine.

Ultimately, it is this meta-front that has me writing the People’s Playbook.

Can the same methods apply to fighting against vaccine passports, CBDC’s, child sex trafficking, and fighting for food sovereignty, health sovereignty and more? Absolutely.

This article has been something of the philosophy, or meta-strategy, behind the People’s Playbook. I wrote it for my own clarity but hope you have found it useful.

As typical, I’ll leave off with a question for you…

Incentivize More Whistleblowers to Do the Right Thing

Donald Soeken conducted a study with 233 whistleblowers in government and the private sector. He found:

90% of the whistleblowers were fired or demoted

27% had lawsuits brought against them

26% sought psychiatric or physical care

17% lost their homes

15% got divorced

10% attempted suicide

8% were bankrupted

And yet only 16% said they wouldn’t do it again. But maybe it’s because these ones got through it…

A NY Times article covering this 1987 study stated, “Mr. Soeken said there are seven stages of life for the whistle blower: discovery of the abuse; reflection on what action to take; confrontation with superiors; retaliation; the long haul of legal or other action involved; termination of the case, and going on to a new life.”

Few make it to the last stage. In other words, whistleblowers go through hell.

While we know of quite a few successful cases, how many are effectively stamped out by such actions?

In The Tobacco Playbook I share the story of tobacco executive and scientist Jeffrey Wigand, which was also featured in the blockbuster movie, The Insider. He went through death threats, a coordinated media smear campaign, and legal actions against him. He stood strong and weathered all the attacks, so we know his story.

That all was decades ago.

Do you think the powerful have gotten better or worse at dissuading and stopping whistleblowers since that time?

Unless you’ve studied the subject, then of course not.

How many whistleblowers where the smears are more successful in controlling the narrative? How many whistleblowers are simply kept out of the mainstream media?

Whistleblowers may be the most devastating enemy of those in power. All the more reason for the powerful to use every tool possible to keep them quiet.

All the more reason for you and I, the people, to look at what they’re saying. And not only that, but support their courageous decisions to blow the whistle, standing up against power and abuse.

How do we do that?

These days, many whistleblowers are often going to Project Veritas to tell their stories. In addition to building a large following despite the smears and censorship, there is something else great that Project Veritas does. That is they help the people to support the whistleblowers directly through donations.

Every whistleblower has a campaign setup to accept donations. I personally have been financially supporting those that comes forth. Why? Because, as the stats show, almost every one of them loses their job for it at the very least.

The amounts I give are small, but lots of small donations really add up. Money is what keeps most locked into doing something they don’t want to do. It too often buys silence. Therefore, donations form the safety net, so that losing your job might not be so bad.

Before diving deeper into that there are some important things to recognize about whistleblowers today.

If what the whistleblower says matches the ideology of the news and forwards certain agendas, they will be giving mainstream media coverage. The whistleblower will be held up as a moral and courageous individual by the narrative.

If what the whistleblower says does not match the ideology of the news and stands in the way of certain agendas, they will be ignored if the threat is small enough or smeared if the threat is big enough. The full industry playbook can and will be thrown at them.

Knowing this, whistleblower’s treatment by the media gives you a very useful clue.

Julian Assange does not fit the classic definition of a whistleblower. However, WikiLeaks was a platform through which the whistle was blown, by people such as Bradley Manning (now Chelsea). Look at Assange’s treatment, from the rape allegations to the torturous imprisonment. Look at the media smearing him with all sorts of labels. Look at Manning’s treatment as well.

Contrast this to recent Facebook whistleblower, Frances Haugen, who gets the limelight. She’s on a big 60 Minutes piece. The media and politicians fawning over her. Why? Even if she legitimately believes what she is saying, which is very much possible, it helps move forward the agenda of greater censorship.

Did this Facebook whistleblower get any news coverage? A little bit on Fox, but not a peep anywhere else mainstream. Not surprisingly, he did get fired from Facebook for it.

“Throughout history, truth-tellers have received a lot of blowback. I knew this, yet could not sit idly by while Facebook enacted these Orwellian measures on its users. Due to my willingness to expose the truth about Facebook’s secret censorship of vaccine concerns, I have been let go from my job. I have a wife who is 7 months pregnant and a son who is 2 years old—we would appreciate any support you are able to offer at this time.”

By the way, the website GiveSendGo.com was used for most of this. They’re a Christian based funding website. Most importantly, they haven’t been removing fundraisers, censoring them, like the more well-known platform GoFundMe has done, such as with the Canadian Freedom Convoy.

This censorship playbook keeps evolving too! There was another whistleblower, this time from Pfizer, that leaked internal documents showing the company lied about using fetal tissues in development of their COVID vaccine, despite all their PR about being completely transparent.

Twitter went so far as to slap a “possible spammy or unsafe” warning label on the link.

As censorship ramps up further, this fight may become even more difficult. Censorship resistant money, such as some forms of cryptocurrency, might become even more important.

Project Veritas is not the only one’s helping people blow the whistle but may be the biggest ones doing so actively today.

What I’m calling the “Whistleblower’s Safety Net” needs two things. First of all, this needs more people to chip in. Even just a couple bucks can really add up when that comes from many different people. It will make a difference for these people, which sends a message to other would-be whistleblowers.

Essentially, we can collectively say, “Do the right thing, we’ve got your back.”

Another example of this is Steve Kirsch, who has tried to incentivize people from the CDC and FDA to come forward out of his own pocket.

Secondly, this idea needs propagation. Spread the channels that support whistleblowers that fight for the people (not for the tyrants).

Spread the idea of supporting those whistleblowers to help other’s in becoming part of the safety net.

Part 3 of 3 part mini-series on Supporting Independent Media as part of the People’s Playbook

Last time I covered all the Substack sources I follow. In this message I’ll share who I follow from other sources, using the principles I covered in the first part.

Interwoven throughout this will be a discussion of how to support independent media in a variety of ways that these people and platforms utilize.

My Top Intel Sources

For longtime readers, many of these sources will be familiar as I used their work in many of my pandemic writings.

I would rank this as my top source of intel. Funnily enough, I was recommended it originally by a customer of mine that happened to work in military intelligence previously. Fitts was a former United States Assistant Secretary of Housing and Urban Development for Housing during the Presidency of George H.W. Bush. She was an insider, that through a series of events because she didn’t play ball, got pushed out. She is great at bringing the big picture of corruption together, with a big focus on economics since that is a huge piece of the puzzle.

Here website is run as a membership site. There is the digital option but also the print option where the quarterly Solari Report is delivered. I devour each issue as soon as it arrives. In addition to the quarterly and yearly wrap-ups, there are videos every week. Some content is available for free.

I first heard of Del Bigtree when he spoke at a health conference, I attended many years ago. I’ve since found his show, which I listen to as a podcast regularly, to be some of the best data on the subject. It is focused first and foremost on vaccines but touches on related subjects.

In addition to being journalists, they’re seeking to “make the news” in that they partner with lawyers that bring suits against medical corruption and our captured agencies.

Behind this news show is the non-profit charity organization Informed Consent Action Network, or ICAN. I donate on a monthly basis to this cause. These funds go to producing the weekly show as well as the legal action they take. I’ll talk more about how charities such as this play into the People’s Playbook another time.

The other big player in the vaccine debate that I follow is Children’s Health Defense, run by Robert F. Kennedy Jr. They also cover environmental issues, EMF’s and the like. The website is rich with detailed articles and their newsletter, The Defender, is worth signing up for.

Children’s Health Defense is also a non-profit charity organization, one that I donate to monthly.

Whitney Webb is one of my favorite investigative journalists that I donate too, just because her work is so good. Her website is named after the inverse of the limited hangout concept I covered in the first part of this series. Both the articles there and her podcast are phenomenal.

I originally found her work when learning about Jeffrey Epstein. On that note I’m anxiously awaiting the arrival of her just released two volume book One Nation Under Blackmail, that covers not only Epstein but the history of such operations.

Mostly he does an almost daily show of about 10-15 minutes that covers the headlines of the outrageous stuff going on.

He also operates a membership site which includes a second daily show, a forum and other useful stuff. He’s also got the biggest selection of shirts with a statement I’ve ever seen which is constantly growing too.

James Corbett has been doing independent news for a long time now. I greatly admire the depth of references he’ll put on every single video. His long form videos are scripted out, but then include references for every tiny bit. It’s how news ought to be done.

He offers a membership which is really pretty much just a donation. There are also DVD’s and a new offering, Mass Media: A History, which would be useful as a crash course for anyone wanting to understand how media works. And some of his other free documentaries are great starting points for the other side of history too.

They are mainstream adjacent. But I find it useful to view people slowly wake-up to the level of corruption in our society.

They have a Patreon which includes a Discord with Q&A. The podcast also features advertising. Just by watching or listening you help their numbers which pays them to put out their show.

This is a great place in that they make news in the way of being a great outlet for true whistleblowers, hidden recordings and more. A lot of big stories come out of Project Veritas these days.

They’re a charity organization that is funded fully by donations. James O’Keefe has also written a number of books. I read American Muckraker which I found quite interesting.

Some Additional Points

Now, all these people are “conspiracy theorists.” All would be labelled right wing, even though several were die-hard democrats and liberals at an earlier point.

How is this parallax? Well, after all my digging, I’m not interested in following any mainstream viewpoints that are easily seen to be propaganda. I still follow some mainstream adjacent. In either case, since many of these cover the craziness of the mainstream, that still comes through.

You might be asking where do I find the time to follow all of this? Speed reading, and watching videos/listening to podcasts at 2.5-3X speed certainly helps. Here’s a report I did on how to do those.

But it’s still a lot. I’m still working on balancing

Funding Sources of Independent Media

I wanted to wrap up with a review of what we’ve seen as ways to support independent media.

Paid Substack subscriptions

Patreon or other platforms (warning that Patreon has been known to censor so not recommended)

Advertising through podcasts

Membership sites

Donations

Book sales

DVD’s/Info course sales

Shirt or other gear sales

Whether it is a donation or a membership, recurring payments tend to help out the most because everyone has ongoing expenses.

Many of these people accept cryptocurrency donations, due to its censorship-resistant nature as well.

This boils down to this concept. If we want to see better news then it is worth paying for. Getting things for free is part of what has gotten us in this mess.

Even if you don’t have money, you can always say “thank you” and “good job.” Those kind of comments are fuel sometimes more powerful than money in want can be a tough job.

Questions for you, dear reader. What are your favorites intel sources? What if any other models have you seen for funding?

Part 2 of 3 part mini-series on Supporting Independent Media as part of the People’s Playbook

In the previous article, I detailed out six principles I use to vet out sources for helping to make sense of the news. In this and the next part of the series, I’ll share my main intel sources for independent media.

In this part, I’ll talk about where we are now, Substack, as a platform. Why I like it and have chosen to use it and the people on here that I follow. In the next part I’ll detail other people using various other platforms.

Here is why I’m using Substack. It is super simple to use. It takes over the details of collecting email optins and emailing out completely. While these are not difficult to do otherwise, Substack has made them seamless and automatic.

Substack also allows for both free and paid subscriptions. I have chosen at this time to make everything available for free for my writings here. Various other people give:

Paid subscriber only posts

Early access to posts

Increased interaction

Signed copies of books

Others use it completely as a donation only platform without any tangible benefit.

They’re rolling out new features such as podcasting via this platform too.

What we’ve seen is that people with a sizeable following, often earned from truth-telling, can make a decent or even great income from Substack. Of course, building a following from scratch is easier said than done.

Many investigative journalists that previously worked for mainstream media outlets instead find their home here.

Instead of some corporation or singular big benefactor being responsible for their paycheck, and thus influencing what can be said, the is a means of a bottoms-up decentralized funding source. That is a theme we’ll be returning to again and again.

And where income streams were demonetized or outright banned in other places, this can be a great place to grow it.

You can do your part in supporting the journalists you wish to see thrive. The point of the independent media is that the funding is independent too.

There does need to be a watchful eye towards audience capture, but this is of much less threat (at least right now) compared to corporate and government capture. Anyone who doesn’t seen that is pointing at pennies, while ignoring $100 bills.

Substack Channels I Follow

Here are the channels that I am currently following at the time of writing.

Hopkins is a playwright in Germany that provides an often needed humorous take on the “Rise of the New Normal” and the “Covidian Cult”. I wish I could write with the same wit and satire he does.

A former teacher in New York about propaganda, Miller fairly recently got fired for his views. Gives great insight into how propaganda works from someone that has studied it for decades. One of the things he does is keep an ever-growing list of accounts of those that “died suddenly” the world over. This includes some very disturbing videos. (Unknown causes are the leading cause of death in Alberta, Canada.)

Kirsch is bombastic, but very passionate. Has put his money where his mouth is, and he has millions that he is wielding in an attempt to get the truth out. Details the facts surrounding vaccination quite in depth from someone that got vaccinated himself.

Lawrie formerly worked for the WHO. She led the meta-analysis that showed, without a doubt that Ivermectin worked against COVID. She even recorded her colleague Andrew Hill talking about how he was pressured from the outside to arrive at the opposite conclusion.

Rappoport is more out-there than most here. He doesn’t believe in viruses. But again, I follow people that I don’t agree with completely. He often also provides imaginative and humorous takes on things.

Berenson is a New York Times report that got squeezed out because of actually following the data on the vaccines. Got censored off Twitter, but is winning a case against them, and actually got reinstated, proving collusion between the White House and Twitter.

Greenwald was made famous from the Edward Snowden NSA leaks. Got squeezed out of a news organization he helped create, The Intercept. Now on Substack.

Taibbi is another mainstream journalist now independent. Does some very valuable deep dives with a humorous take, pointing out the hypocrisy involved often.

Eisenstein often talks about the mythology behind our the movement of the masses. Definitely a viewpoint that stands out from the rest.

Siri is the main lawyer that the Informed Consent Action Network works with. He battles and wins cases against the pharmaceutical fraud machine with a focus on vaccines.

Some of these people are what I like to call “mainstream-adjacent,” such as Taibbi, Greenwald and Berenson. They only recently got squeeze out of the mainstream. While they cover certain topics well, they still follow the propaganda on such things as 9-11. Or thinking that only this vaccine is problematic but the vaccine program as a whole hasn’t been. In short, they only diverged from the masses recently.

Others are off the deep-end, and I say that with respect as I’m off the deep end myself. Again, parallax through multiple angles.

This is a living list. Some people I read everything from. Others I just glance at a few pieces here and there. Some I’ll stop following at some point. Others will be added.

And this is just around “news” topics. There are, of course, writers covering every sort of subject here on Substack.

Most of them I follow as free subscribers. A handful I lend a few bucks in support.

The Potential Downside

I’d be remiss if I didn’t cover this subject without this warning. Substack is a centralized website. They’ve made clear their stance on free speech and stood strongly for it, at least thus far. Here’s an excerpt from their article, Society Has a Trust Problem.

We will continue to take a strong stance in defense of free speech because we believe the alternatives are so much worse. We believe that when you use censorship to silence certain voices or push them to another place, you don’t make the misinformation problem disappear but you do make the mistrust problem worse.

Trust is built over time. It can be rebuilt over time, as long as those in positions of responsibility don’t succumb to pressure to take shortcuts. Trust can’t be won with a press release or a social media ban; and it can’t be strengthened by turning away from hard conversations. It comes from building and respecting relationships. For the media ecosystem, it requires building from a new foundation.

That is the work we commit ourselves to at Substack. It is hard, and it is messy. It is the only way forward.

Will this continue to be the case always? I sincerely hope so.

But even if they do stand their ground, that would only mean that they’ll come under attack in other forms. They will be smeared and censored.

While I’m going to be using Substack for the time being, as a backup all articles will also be hosted on here on LoganChristopher.com, a platform I control.

A 3 part mini-series on Supporting Independent Media as part of the People’s Playbook

To do proper sensemaking on the world you need to get news from someplace.

The mainstream media is clearly corrupted. Some people still believe in the partisan games and therefore believe their side’s media due to this reason. But even while some truth gets out on these platforms there is still much that is hidden.

Mainstream media in the USA is all funded by corporations through advertising. Pharmaceuticals dominate the airwaves of news programs today. There are also interlocking directorates leading to top-down decisions on what is covered and what is not. (See #49 and #50 of Medical Monopoly Musings for details.) These are just a few of the important pieces to controlling journalism.

In other countries, the media is directly funded by the government.

Online the same games are being played. Big Tech is on board with mainstream media pushing their voices further, while suppressing others. And taking direction from government as well.

Many are of the mistaken assumption that truth can only come through such official channels. Thankfully more and more people are dropping such illusions.

The good news is that there are a great many independent voices available. But how do you separate the wheat from the chaff?

In this short series I want to deliver three things:

Principles for finding and vetting your own sources

A list of some of my top independent sources that I follow

An understanding of this “parallel news economy” and how you can play a part in it

Let’s get started with the principles.

Principles to Finding and Vetting Your Own Sources

Here’s my list of principles:

Follow the Money

Follow the Transparency

Witness Mistakes

Limited Hangouts and Seeking Parallax

Follow the Smears

Follow the Silenced

Follow the Money

Everyone has heard of this. This is what I mentioned before regarding the money flows of advertising, personal conflicts between board members and much more.

Two big things to ask here. Is the journalist corrupted from covering things by incentives either personally or institutionally?

Do they themselves follow the money in their coverage?

I won’t belabor this point as it is well-known. The other principles have a lot less awareness.

Follow the Transparency

Is the journalist transparent about their sources? Now, of course there are times when sources must be kept secret. But 98+% of times the source or reference can be shown.

Specifically, is the issue of data transparency rather than the fallacy of authorities. There is a big difference in saying “The CDC says…” compared to showing a specific study or data instead. (And when you can use the CDC data to show the CDC is lying, well that tells you something.)

In the online world particularly, you want to see links to reference material. You’ll notice that I strove to do this in my own work because I witnessed others doing the same. It’s much more work but it is more trustworthy to do so.

If a source is transparent about where their facts are coming from that’s a big plus. (Of course, for true vetting you need to make sure the sources in fact say what the coverage says they say.)

If a source is not transparent about their facts, and is not transparent about potential conflicts of interest, then that’s a big negative.

Witness Mistakes

This is related to the subject of transparency. You obviously want to find someone with a good track record. These are people worth continuing following for making sense of the world. Do their stories and predictions pan out?

But no person is flawless. We all make mistakes.

How does this journalist handle theirs? Do they bury them and pretend they never got anything wrong?

Or do they come out and admit what they got wrong? Do they apologize? Do they openly talk about the subject?

This helps you to differentiate who are the propagandists and who are legitimate journalists.

Limited Hangouts and Seeking Parallax

The term “limited hangout” comes from intelligence. It means to leak out some partial truth in order to control the narrative. Along with the partial truth are either lies or just an avoidance of all the facts. This method is often used as part of damage control.

Here’s the thing. All news is essentially limited hangouts, albeit mostly unintentionally, because no one can possibly cover all angles. It is by necessity limited to some degree.

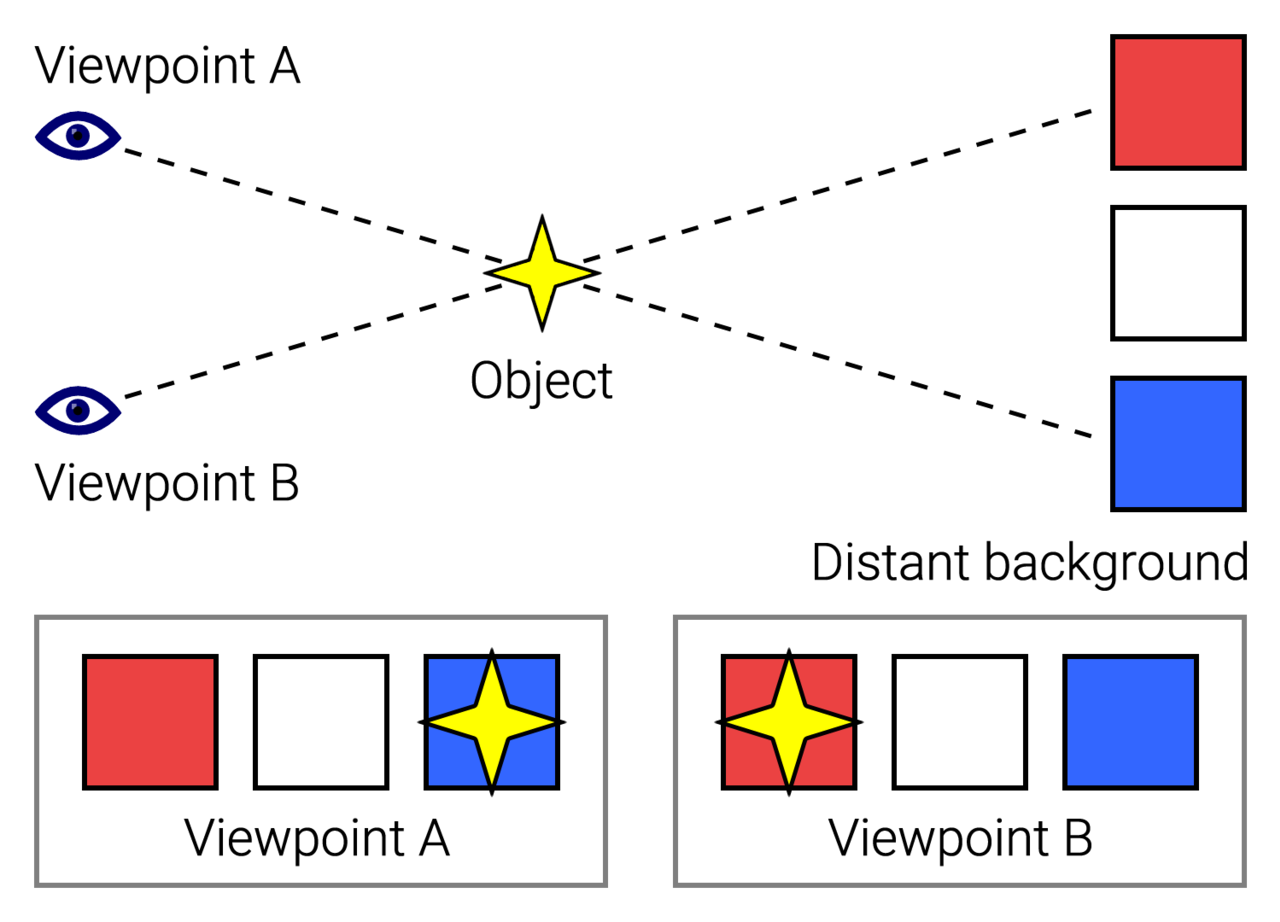

Parallax is the apparent displacement of an observed object due to change in position of the observer. By having two eyes you’re less likely to fall prey to blind spots that are inherent in a single point of view.

Journalistically, I think of parallax as being the idea that getting different viewpoints, different coverage on a story helps you to see it more accurately. Any single viewpoint is by definition, limited.

By having different sources, that come from different worldviews, you’re likely to come to understand more. This is especially true for those seeing past intentional limited hangouts as well as ideologies that everyone get wrapped up in. Especially those that don’t think they get wrapped up in ideologies, they’re the worst!

Follow the Smears

You must understand how smear campaigns work. I detailed this inside chapter 6 of The Tobacco Playbook.

Smears are nothing new. It’s just accelerated today.

Understand this…any good journalist dedicated to truth will be squeezed out from any mainstream place and will be smeared in the process.

Today the smears use the common phrases of “conspiracy theorist,” “right-wing,” “extremist,” “anti-vaxxer,” “science denier,” “racist,” and so on. I’ve been called all these things of course!

In smears you need to follow the other principles here. Are there transparent sources and data about the facts? Or is it merely ad hominem attacks?

Smearing is used as a control mechanism, so you must understand how it works.

Be warned that it is not as simple as flipping things to the inverse though. A good way to have controlled opposition gain credibility would be to have them smeared.

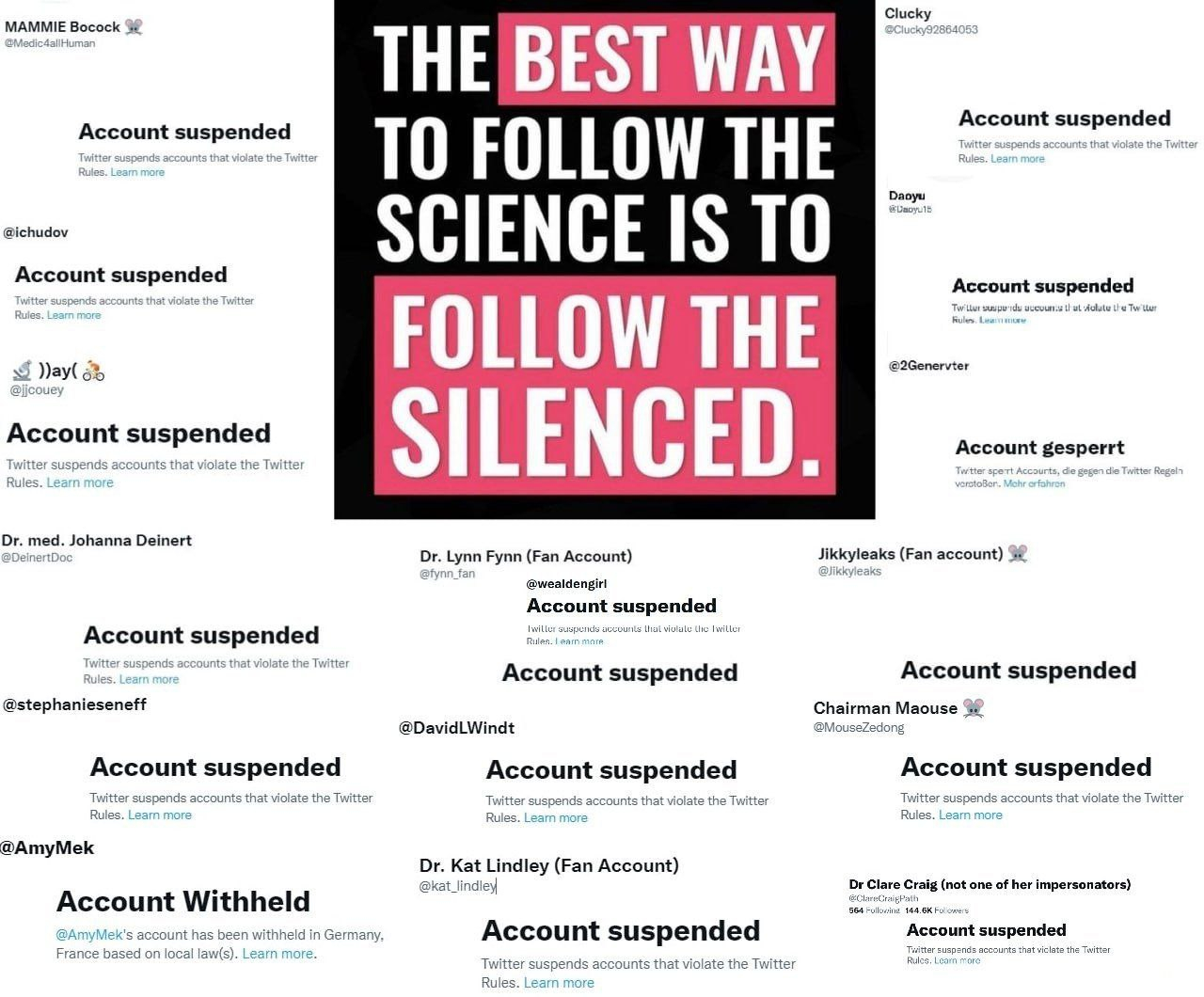

Follow the Silenced

I came across this meme the other day.

This is the next and often simultaneous step of smearing. To down-rank, shadowban or outright censor information.

If it doesn’t support the agendas, it will not get widespread distribution.

Again, you shouldn’t automatically 100% trust anything just because it is censored, but this can be seen as a clue.

Putting Them Together

These are the principles I use to vet out when looking at media and various sources.

Any one principle alone is a good start, but it is insufficient. By understanding and utilizing all of these you get a much better picture of who is worth listening too.

In the next two parts I’ll detail out my top intel sources, as well as showing how to support them.

But first I’d like to ask what your principles along these lines? Anything to add to this list?

I figured I’d start with this one as it is something I am actively engaged in. I’ll be moving up to Idaho from California later this month.

Strategic Relocation is the name of a book by Joel Skousen. From his website:

Strategic Relocation is an in-depth analysis of North America’s safest places to live. Unlike most guides in today’s bookstores that tout the “best places” to live based on golf courses, doctor/patient ratios, warm sunny climates, availability of cultural activities, status of educational institutions and the growth potential of the local economy, this book will help you consider future threats that most other people fail to see or choose to ignore such as:

A labor crisis or pandemic that halts the inflow of food and business goods

An economic crisis that threatens your pensions, investments and other so-called “guaranteed” income streams

A major earthquake or other natural disaster that suddenly upsets the natural social order for months at a time

An emergency that clogs the area’s freeways

The “unthinkable” nuclear war or major terrorist attack on a U.S. city with chemical or biological weapons

Joel is an extremely conservative man. And I do not mean conservative as the slur that it is commonly used today. I mean it genuinely. As such, I do not share all his viewpoints. At the same time, that is great because I enjoy learning from people who I do not share all viewpoints on.

It’s quite mind-stretching to see that he believes with some certainly that at some point the USA will be attacked by Russia in a limited nuclear war. Apparently, Russia never bought in the MAD idea (mutually assured destruction) and thought a nuclear war was winnable.

Then I was also just reading in The Pentagon’s Brain, a book about DARPA, about the “super plague” that the Russians were supposedly working on too! But don’t worry the head scientist of such biological weapons defected to the USA.

Anyway…

This book covers very many interesting things. Also included is Joel’s viewpoint is that inside the USA is still better than any other country to be in. That many places that people think of in Central and South America are to go total military dictatorship, as many have before.

If the book interests you than by all means grab a copy. But even without that want to talk about this subject.

My wife and I had actually have been trying to get out of California since 2019 before the pandemic even started. While I love California’s geography and weather, as well my friends that live here, the economics and politics are not serving me.

Our primary reason for moving is that my daughter cannot attend school in California without following the CDC’s schedule of vaccinations. And that’s a hell-no-over-my-dead-body thing for me. While we could homeschool in California, that is not something we are desiring to do at this time.

We moved up to Oregon for a short time. While better on this front currently, that state seems to be following in California’s footsteps.

Unfortunately, a long strange bout of unidentified disease with turned out to by Lyme in my wife brought us back to California, as we needed family support. But after a diagnosis, while not healed completely yet, we’re were in a much better place. Good enough to seek to move outside California again.

After visiting several states we made the decision to move to Idaho. This was before getting Joel’s book, but I was happy to see that state rated the highest at four and a half stars out of five. (Utah being the only other state with that rating)

In Idaho we found a school that never even required kids to wear masks throughout the whole pandemic.

(It was quite ironic to view other Waldorf schools that advocate for no screen time at all for young children…that went to distance learning during the pandemic! Can you say cognitive dissonance? I believe Rudolf Steiner is rolling over in his grave.)

Idaho happens to have the freest laws regarding home schooling. You can basically do anything you want. So that’s good to know should we want that option in the future, which indeed we may choose is necessary in due time.

The gun laws are of course very lax as compared to California.

No one much thinks about Idaho, as compared to some of the other states that have much more focus that many are moving to such as Texas and Florida. I think less attention on the world stage is a good thing.

Since my house burned down in California, looking at the natural disasters of the area was obviously important too. I personally didn’t want to deal with hurricanes so the East Coast wasn’t an option for me. Idaho doesn’t have much. Fires are a possibility there, but not something that has happened in the area I’m moving too.

And then there is the cost. While house prices have risen significantly in Idaho as they did everywhere over the last couple years, and more so because of a lot of other people relocating, it was still cheap by California standards. This immediate savings in cost of living can then be repurposed for some of the other strategies I’ll be covering in the People’s Playbook.

I could go on and on, but you get the point.

While the circumstances are certainly not the same, I’ve often wondered about the Jews in Germany back in WW2 and before then. At what point was the right time to get out? There obviously was a too late. But there were many that left earlier and thus were spared.

California is on a trajectory. I don’t see that changing any time soon, so I’ve chosen to leave now before it is deemed necessary. It’s not an easy choice. In fact it changes just about everything in my life to do so.

And this is exactly why this strategy is so important.

Where you live is your home base. This is your base of operations in which the other strategies will be implemented.

Where you live is one of the major fronts of the war that we’re all fighting on.

I have a sense that it is harder to enact change in California due to that trajectory and the demographics. Meanwhile, with its smaller population, more can likely be done in Idaho politically, legally and economically.

Plus it should be much easier to find like-minded people too. (After all there are still people in Santa Cruz driving around by themselves wearing masks here. As I write this, I can see school children walking by themselves outside wearing masks through my office window.)

Here’s a few questions for you to ponder:

Are you in a strategic location or simply a location of circumstance?

What are the benefits, costs, threats and opportunities in where you live?

Should you relocate? Where to?

Should the shit-hit-the-fan do you have a plan B and plan C for strategic relocation?

As I’ve discussed in the Civilization Collapse Stack, your home is a massively important piece of the puzzle, especially if aiming for subsistence. Mobility is also important too so don’t neglect that.

I’ve chosen to relocate for a wide number of reasons, most of which were mentioned above. And I’m far from the only one. Many others have done the same and many, many more will still do in the coming years.

It’s tough because there is no guarantee that it is the right choice, but I’m playing the odds. What about you?

I’m back to writing on worldly topics but in a new location (Substack…I’ll talk more about why I chose this another time) and now focused on solutions to some of the problems we see ourselves in.

I’m calling this new series The People’s Playbook. This is in contrast to The Tobacco Playbook that I’ve extensively detailed here, which of course is not just about Big Tobacco, but has been used by industry everywhere. That deep dive was to understand the structure of how it’s done.

Did Bitcoin arise organically from Satoshi Nakamoto as a result of the 2008 financial shenanigans?

We don’t know who Nakamoto was. The answer is shrouded in darkness, so you better believe that there are conspiracy theories on this topic! Was it an NSA/CIA project from the beginning to usher in the transformed and controlled economy we’re stepping into?

Yet that’s hard to matchup with the libertarian ethic of the vast majority of people in the crypto space, especially early on.

Understand this is a system, designed how it is to be decentralized and trustless, that could free us from the centralized system of financial tyranny and control we live under. Or at least that’s on the surface.

However, I don’t want to underestimate their ability to co-opt movements or utilize multi-layered deception, including roping in numerous patsies in a long-range plan.

Even if Bitcoin was something built to help free people from the beginning, in what ways can the narrative be steered?

There is no doubt in my mind that cryptocurrency is the basis of our future economy (unless we destroy ourselves back to the stone age or a solar flare wipes out all electronics). This complete transformation will take place over the next decade or two. The question is whether it is economic collapse or economic controlled demolition as I’ve been talking about? Or, most likely in my opinion, some combination of the two, a steering of collapse in a certain direction to “build back better” how it is desired.

The conclusion that crypto is the future of money, in one form or another, is one thing.

But HOW exactly it plays out, for better or worse, is what I’m really interested in. If you and I can get this right, it will be easier to navigate future events, including making “civilization collapse stack” investments along the way.

This article focuses on Bitcoin almost exclusively. The next part will look into other cryptocurrencies, most notably the field of stablecoins and CBDC’s (Central Banker Digital Currencies).

Bitcoin’s Origin Story

Bitcoin as a Technology to Free Us from Banker Control

The 2008 financial crisis had kicked off with Lehman Brothers collapsing in September. Satoshi Nakamoto put out a whitepaper on October 31st that year, titled Bitcoin: A Peer-to-Peer Electronic Cash System.

As a result, Bitcoin began with its genesis block on January 3rd, 2009, when the first 50 BTC were mined into existence.

Contained in this genesis block was a hidden message, “The Times 03/Jan/2009 Chancellor on brink of second bailout for banks,” which was the headline of The Times newspaper that day.

And so it was that Bitcoin was initiated as a solution to the systems caused by bankers. Meanwhile, via their captured government partners, the bank that were “too big to fail” were rewarded for bad choices to “preserve the system”.

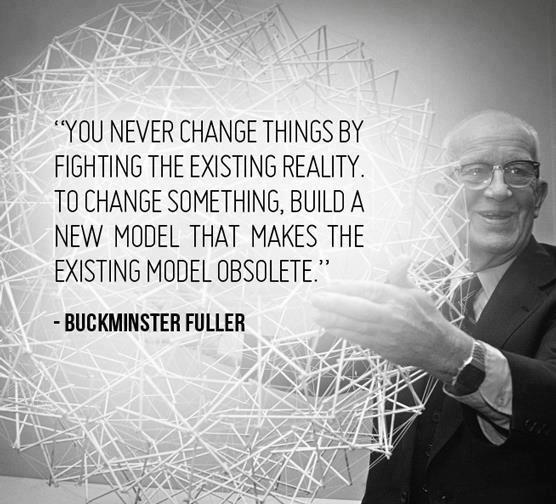

This reminds me of the Buckminster Fuller quote that I often think about…

Here was something that didn’t aim to fight the system, but instead to overcome it by building something better.

And so most of the people involved in the early days were crypto-anarchists and libertarians.

We don’t know who Satoshi Nakamoto is. Was he just a smart but otherwise average person interested in cryptography that kicked off a revolution?

Way back in 1517, Martin Luther posted his “Ninety-five Theses” in the church door, condemning the corrupt world power of the time, the Roman Catholic Church. This event kicked off the Protestant Revolution, which over the coming centuries would alter the course of Western civilization and thus the world.

Is it a coincidence that Martin Luther posted the Thesis on October 31st, the same day as Nakamoto’s whitepaper? Or was this another “encoded” message?

Regardless, it is worth considering that the Bitcoin Whitepaper started a similar trend in action. That we are in the midst of a revolution just beginning to take shape.

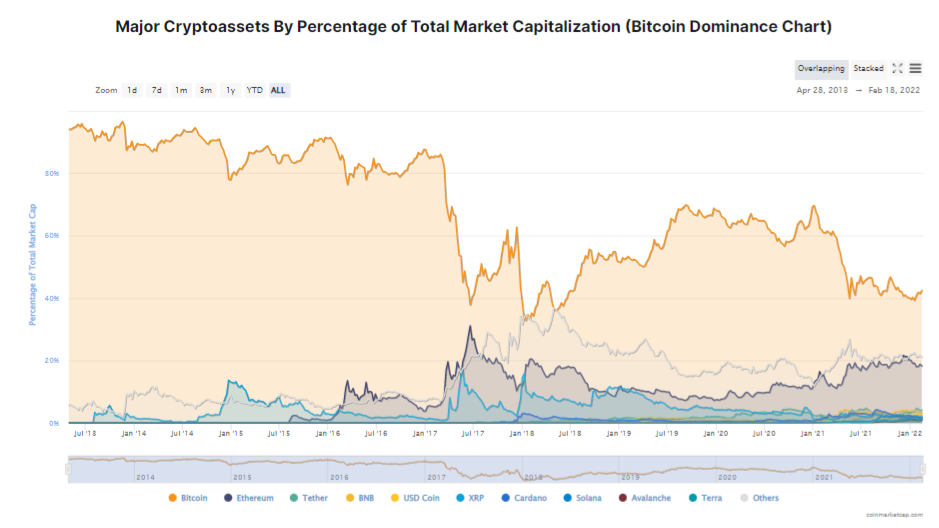

Make no mistake, there were previous attempts at cryptocurrency, like Bit Gold and Hashcash. But Bitcoin was the first one to become successful and reach a dominating network effect.

Bitcoin is currently over 40% of all crypto by value and that is near it’s lowest ever mark. The next player, Ethereum, isn’t even half that.

Still, this story is only one narrative and is not the only option…

Bitcoin as a Controller Plot from the Beginning

It’s tough, without knowing much of anything really about Satoshi Nakamoto, to judge where this came from.

There are conspiracy hypotheses that Bitcoin was a CIA plot from the very beginning. Or NSA, or bankers, or whatever other powerful entity you might think of.

What if the controllers of the world saw that the fiat system was unsustainable, especially with the grift-machine involved, and wanted to start up a new system that would give them even more control?

Satoshi Nakamoto, whomever that is, is sitting on a stash of 1.1 million BTC. That’s worth about $40 billion USD in today’s prices. If it was one person, that person would be roughly the 15th richest person on earth (publicly anyway) from this alone.

What happens if this money ever actually moves?

Could a new system have been designed from the ground up?

Oh, how devious would it be to enroll libertarians into your new system, only to enslave all people even more so later on.

To me, this seems a bit of a stretch. I concede it is possible because no one really knows how the world works. But that doesn’t mean it seems likely.

After all, there isn’t really anything I’ve seen in the way of proof to back this up. Nothing solid I’ve seen anyway. (If you have data, please do let me know.)

This is a conspiracy theory that exists only off of conjecture. That doesn’t make it wrong, but certainly very opaque. Based on other evidence they do seem capable of pulling of massive, devious and long-range planes.

Secondly, the fixed and therefore sound money supply, plus the decentralization involved do seem quite contrary to the ideas of centralized control.

Related to this is the idea that Bitcoin was a prototype, but was never meant to be the final solution. Which brings us to the next narrative. Even if Bitcoin had noble intentions from the beginning, doesn’t mean that would always be the case…

Bitcoin Co-Opted?

Do NOT underestimate the ability to co-opt and steer legitimate movements. We see CIA infiltration of the feminist movement, FBI infiltration of anti-Vietnam movements with COINTELPRO and so much more. We see powers that be literally involved in terrorist acts, murdering innocent people with Operation Gladio to steer the narrative as desired. There are so many examples of this.

So what if Bitcoin was a legitimate revolution as it may well have been?

Do you think the powers that be would simply roll over and allow a new financial system to take away all their power? Of course not!

Infiltrating the movement and influencing its direction would be expected. It’s not a question of if…but how. What does that look like exactly?

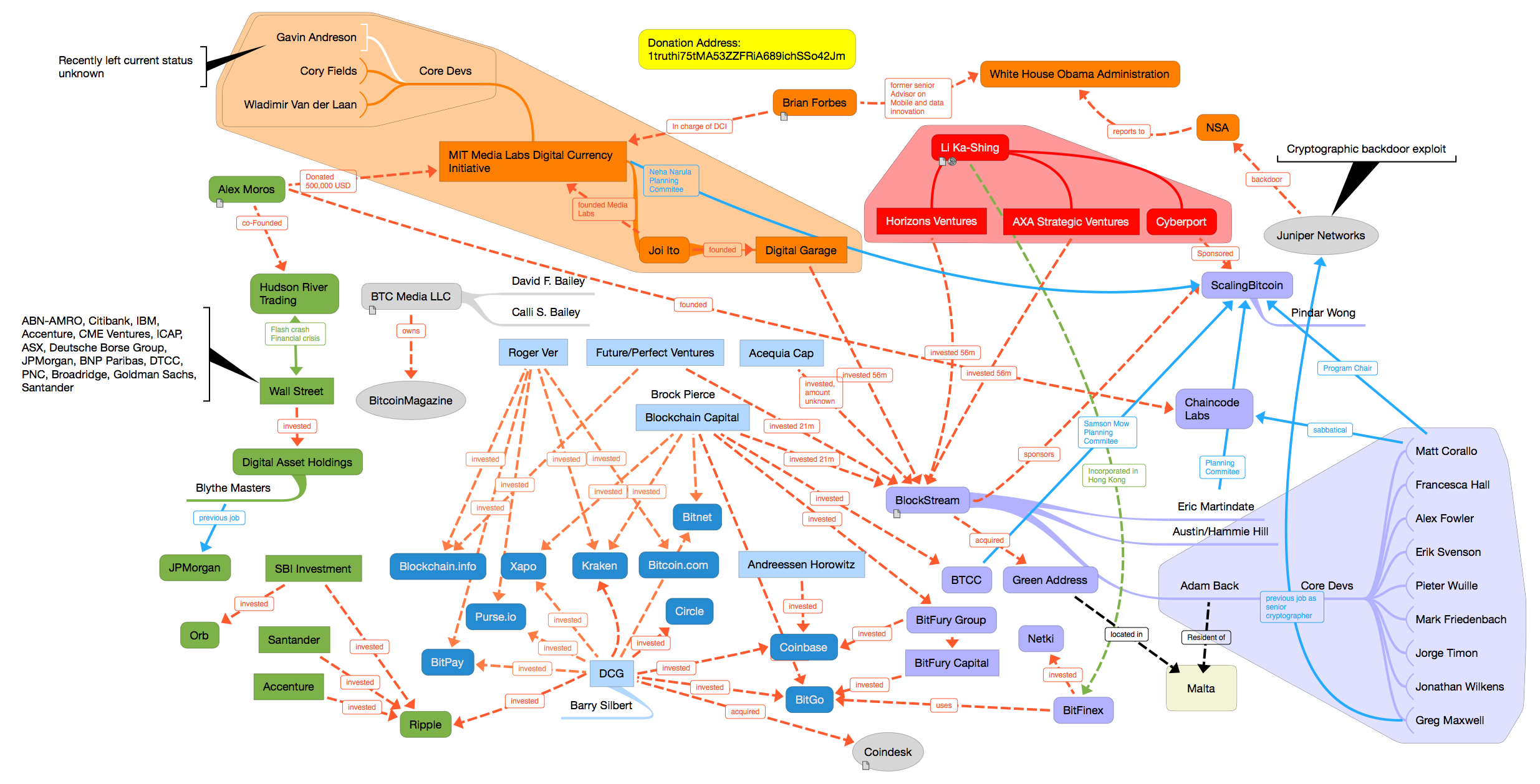

Here’s one possibility. The following comes from an exchange years ago I had with my friend who gave me permission to share this. (Some slight edits involved for readability.)

I’ll distill it down for you as best as possible. It’s like this:

Original Bitcoin = First big threat to banks in many centuries. Original bitcoin is called bitcoin core.

Banks form fund through AXA Investors (well over trillion in assets) – many ties to Bilderberg group, institutional investors, etc (ref: AXA is the second most powerful transnational corporation in terms of ownership and thus corporate control over global financial stability and market competition)

AXA Investors does (documented, likely much more) 75m investment into a company called Blockstream.

Blockstream goes on hiring spree of some of the best blockchain programmers at high pay and begins to do 4 things:

Inject proprietary patentable code (with NSA back door) into bitcoin core’s code.

Break the functionality of bitcoin core so it is NOT usuable as peer to peer electronic cash, resulting in centralized nodes of control (lightening network), like banks have with high fees so they can control it better. This was what the big block/small block debate was. Blockstream limited blocksize to destroy the functionality of bitcoin (slow to no confirmations) and charge high fees from a tollbooth position.

Turn it into a financial instrument, like a security so they could drive up the price and crash it to make money and shake the publics confidence and control it.

Hired a massive social media trolling army to change the narrative to “store of value” and “digital gold” (i,e., not a medium of exchange for normal people) and viciously attack other crypto’s namely, Bitcoin Cash which forked away from Core and is actually the original bitcoin.

Here’s an infographic but it’s only a fragment of what’s going on and out of date by several years.

FYI this is the only uncensored Bitcoin forum on Reddit. The rest are controlled by the troll army and heavily censored as is twitter, etc – owner of twitter is actually paid Blockstream shill, no shit.

ETH was actually created because Vitalik was blocked by Blockstream from using his ideas in Bitcoin.

Do you know about that Tether scam? In a nutshell, Tether acts as a large central bank for Bitcoin core. Every time the price of core goes down they will mint millions of tether and buy Bitcoin core to prop the price up. An academic paper was even written about this that proved the link, mostly through Bitfinex.

I don’t want to be anywhere around core when that pops. It will bring down the whole system for awhile, but especially core.

To wrap it up, Bitcoin Cash is the original bitcoin. It’s super fast, super low fee and used grassroots world-wide. It is the original Bitcoin. Bitcoin Core is no longer bitcoin, that ceased with the fork. Roger Ver is a libertarian who is the largest proponent of BCH or bitcoin cash, he gets DESTROYED in social media by the Core Troll Army. Here is his site which is pretty much the only non-propaganda news you can get in the crypto world (i.e., it’s not controlled by blockstream).

I paid my brother $200 in BCH (bitcoin cash) last night, payment went through in 2 seconds. I use it online all the time. The utility is there.

Crazy story!

***

I personally have not dug deeply into all this to vet it out, but share it here to share the possibility and have the links for digging deeper to start your research if you want.

This has the ring of accuracy to me. It absolutely is true that BCH is faster and cheaper to use than BTC for transactions.

And I have dug into the shadiness of Tether (USDT).

If the bankers that essentially control the world economic system saw a threat in Bitcoin, why wouldn’t they do something about it? If you couldn’t outright destroy it due to its decentralized nature, the least you could do is get your tentacles into it, just like they’ve done with pretty much every single big institution in our world. In that way this seems to follow the playbook.

And of course there’s even more rabbit holes to go down…

There is Craig Wright, who claims to be Satoshi Nakamoto (most people don’t believe him as his proof is dubious at best). But Bitcoin Cash (BCH) was forked to become Bitcoin Satoshi’s Vision (BSV). If BCH is the true Bitcoin, was this another co-opting, done to further muddy the waters and make BCH seem less useful by confusing people?

One of the best ways to keep people from finding the truth is to layer in more deception. When there’s too many rabbit holes to go down, there will be massive confusion. And a confused mind is easier to control.

Block Size and Decentralization

However, I list that as a possibility. I do understand something of the contrary argument. To increase Bitcoin’s block size would increase its centralization. Bitcoin (BTC) blocks are 1MB in size. With that its entire history is about 380GB in size.

Meanwhile, Bitcoin Cash (BCH) blocks are up to 32MB in size.

It’s entire blockchain size is only 176 GB. Why is it smaller, if it has a larger block size? Less transactions in total. BTC is much more popular and thus has many more transactions.

For those of you who have no idea what this means, let me explain it simply. These bigger block sizes mean that transactions are cheaper and faster as more transactions are contained in each block. However, this does come at a cost of decentralization. The miners (or validators in other blockchains) need storage space and capacity to hold the blockchain so they can secure and verify transactions. The bigger the chain is, the less individual people can do it on home computers and the more big dedicated companies need to be involved. If people alone can’t do it, only big companies can, then this is more centralized. More details on BTC vs BCH in this article.

And just to throw it in there, BSV has a 2GB block size! The chain is 2334 GB and growing fast.

(Compare also to one of the hot blockchains right now, Solana (SOL), which has a 1GB block size every second, producing 4 petabytes of data per year. While they split validators and archivers, this doesn’t seem like a sustainable model. In any case it is highly centralized and subsidized.)

Understand that decentralization is key to keeping it uncontrollable by ANY entity. This is what the bitcoin maximalists are shouting about.

So that covers some of the theories about the past. Now we’re going to switch gears and look at some ongoing narratives about Bitcoin.

Current Bitcoin Narratives

Bitcoin is Bad for the Environment

This is probably the most prevalent of the narratives. Here’s a video from Coin Bureau that goes over the facts.

Bitcoin can be mined with polluting forms of energy, absolutely. But it also can and does use sustainable forms of energy for mining, with this being an ever growing amount. It can also use wasted energy production such as the flare off of natural gas at oil mining sites to also mine bitcoin, further improving economics.

In short, “bitcoin is bad for the environment” is easily falsifiable in a couple of ways.

The traditional finance system that Bitcoin aims to replace takes far more energy than bitcoin does.

Compare the energy used for let’s say the US military. The left doesn’t really talk about reducing that, even though they use to be anti-war, instead they focus on favorite enemies like bitcoin instead.

And maybe part of the narrative is that Bitcoin isn’t good for the environment, so another system such as any of the proof-of-stake cryptos which are much more energy efficient (and typically much more centralized) should take its place.

Rest assured, with the ongoing climate change narrative, this narrative regarding bitcoin and cryptocurrency is not going away anytime soon.

Bitcoin is Used By Criminals

In a WSJ interview, Bill Gates was asked what technological advancement the world could do without. Gates replied, “The way cryptocurrency works today allows for certain criminal activities. It’d be good to get rid of that,” he quickly added: “I probably should have said bio weapons. That’s a really bad thing.”

Early on, bitcoin was used to fund WikiLeaks when they were blocked by a financial blockade which included Bank of America, Visa, MasterCard, Paypal and Western Union in 2010.

One of Satoshi’s last few posts read, “The project needs to grow gradually so the software can be strengthened along the way. I make this appeal to WikiLeaks not to try to use Bitcoin. Bitcoin is a small beta community in its infancy. You would not stand to get more than pocket change, and the heat you would bring would likely destroy us at this stage…It would have been nice to get this attention in any other context. WikiLeaks has kicked the hornet’s nest, and the swarm is headed towards us.”

Was it this event that got the financial powers to start targeting and co-opting Bitcoin?

Yes, Bitcoin was used by people to buy drugs, including online. But so is cash. And the stats show that more financial crime is done with the US dollar over anything else. In that way this narrative is quickly falsifiable. The US dollar or other fiat currencies aren’t targeted by the narrative because of their use by criminals. (After all the biggest criminals, the bankers, use their fiat currencies of choice.)

Of course they never let the facts get in the way of a narrative. Senator Elizabeth Warren echoes these: “Cryptocurrencies have created opportunities to scam investors, assist criminals, and worsen the climate crisis.” A triple whammy!

It happened with WikiLeaks. It’s happening now…

Bitcoin Funds Terrorists!!!

While this has been an ongoing narrative for some time, there’s a present event that is being talked about in these regards.

The Freedom Convoy in Canada. Here’s a couple videos for those not familiar with this (what with the mainstream media blackout primarily, and smear campaigns secondarily).

Funding was raised initially through GoFundMe. They, being a Silicon Valley company, stopped the funding. (For many people this was the first time they heard of GoFundMe doing such, but they’ve been delisting anti-narrative things for well over a year now.)

The crowdraising platform GiveSendGo became the next place to be used with almost $10 million raised so far. As a result they were:

Hit by denial-of-service attacks to disrupt the website.

Bitcoin is great in that it can’t be censored. That’s what people have been talking about for a long time, ever since WikiLeaks. However, if they’re freezing bank accounts (not to mention crypto exchange accounts) you can’t necessarily transform BTC into fiat currency. This is okay if others will take your BTC, but not if you need to go from one economic system to another.

BREAKING: Canadian Federal Police call for FINTRAC to block over 30+ #Bitcoin wallets from transacting with major financial institutions.

In short, Bitcoin being used as the crypto of choice for hackers doing ransomware of other cyber attacks. (Actually Monero and other privacy coins are far better than Bitcoin as it is relatively easy to track Bitcoin on the blockchain.)

I finally found the video that I couldn’t find for that post! Matthew Kratter discusses how such an event could specifically target Bitcoin. The scenario he lays out starting at 5:55 is:

Global internet outage

Shadowy super-coder hackers demand Bitcoin ransom

Global outcry against Bitcoin

Coordinated global crackdown on Bitcoin

This then leads to a global war on cyber terrorism that leads to required internet registration, “internet passports,” CBDC’s and the like to further control…

Definitely seems like a good way to go with the plan. Squeeze out bitcoin while CBDC’s and your digital ID, the trusted solution, come in its place.

Bitcoin Will Be Banned or Regulated Out of Existence

All of these other narratives lead to the idea that bitcoin will be banned.

Its tough because as long as enough people use it bitcoin will continue on the trajectory it’s been on since its inception, which is towards mass adoption.

Bitcoin has been claimed dead some 444 times in the media now! But then some people just make bad projections…

I’ve said it before and I’ll say it again, I don’t want to underestimate my enemy’s ability to co-opt movements and steer the narrative. The aforementioned narratives ramped up far and hard enough could ultimately lead to this place of crushing bitcoin.

The following is a long video but a good discussion with Catherine Austin Fitts, author of the Solari Report, some of the best intel for the people in my opinion, and Aleks Svetski, found of Amber a Bitcoin app and editor of The Bitcoin Times, hosted by Dr. Mercola:

Fitts viewpoint is that basically some of the narratives mentioned here will crush bitcoin. That it was a prototype of the controllers from the beginning. And that digital money cannot help us thrive if other steps aren’t taken to stop the digital control grid.

On the other side…Svetski’s thesis is related to the next point, and switches gears to a more positive narrative for Bitcoin…

The Bitcoin Standard

Bitcoin is designed to be inflationary but at a set amount that cannot be changed. Furthermore, it is a decreasing amount, unlike the inflation we’re facing now and is fiat’s destiny. This makes bitcoin scarce.

And as Michael Saylor has argued, it is the first currency that was ever engineered to be so. In other words, it is the first technological improvement in money as a whole in a long time.

The further innovation is that it was designed to be trustless, or perhaps in a better put way, the trust is so flatly distributed (through the miners) that there is no central controller. No central controller means a fair and independently sovereign money.

That these factors could lead to Bitcoin becoming the standard by which the global money supply is used. It could be the bitcoin standard like it used to be the gold standard. And in fact, bitcoin is superior to gold in several ways not the least of which is its ease and cost in being moved.

(One possible scenario that came to mind is what if we get to a Bitcoin standard…only to later have that removed decades later through one means or another? Again, co-opting and steering narratives is always done.)

So even if it was crippled to become “digital gold” instead of “digital cash” the benefits of this being the settlement layer for the world could very well be vast.

This is what all the bitcoin maximalists are pushing for. The fact that there is an actual possibility of it occurring, makes bitcoin worth investing in at some level, in my opinion.

Does this solve all our problems? Of course not! But we absolutely need steps in the right direction.

Even just to have bitcoin as one of many possible currencies does give big utility for savers and censorship resistance. Where I disagree with Fitts on this subject is that bitcoin is a helpful step in the right direction. It can be used now to help us, but certainly is just one tool in a kit we need to assemble.

Bitcoin as Legal Tender & Sovereign Money

Related to this we see the adoption of bitcoin as money, not just by people and institutions but by countries.

El Salvador made the news last year when they adopted it as legal tender, in addition to the US dollar.

My prediction, as well as the prediction of many others, is that this year we’ll see more countries follow suit.

Basically, it’s going to go one of two ways. Will there be contagion, other countries doing the same? Or it will be crushed in some form?

If Bitcoin does indeed fight the powers-that-be, El Salvador is very likely in for a rough ride ahead. This includes regime change being on the table. (Libya’s leader Gadaffi wanted an African union and currency outside the petro dollar for example.) Still, if such attacks can be weathered, and if it is played smartly El Salvador could become much more successful.

If Bitcoin is part of wicked a plan of centralization through deception, then El Salvador may do well indeed, but slowly move towards greater control and less freedom.

I am very curious to see how this plays out. Exactly how things go for El Salvador gives us very strong hints as to whether Bitcoin is really for freedom or has been controlled/co-opted.

Should You Invest in Bitcoin?

In summation, I don’t know where it came from! I don’t know where it’s going!

This article probably gives you more questions than answers. But at the very least I hope this has given a good overview of the different possible past and future scenarios and various ways they could play out.

As for your own personal investing, understand this. At worst Bitcoin can go to zero. The chances of this happening are far less than that of other cryptocurrencies, but it is still possible. Besides that it may get controlled in such as way that it becomes less usable (the platforms that allow convertibility to fiat).

On the positive side, bitcoin is censorship resistant and in its short history, has been not just a store of value but ever increasing in value when looked at in the span of years. That this could continue means the sky is the limit on where bitcoin could go.

For it to back the world’s financial system or even just a portion of it would mean a six and eventually seven figure bitcoin.

Even (especially?) if it is controlled/co-opted it may still have a role for the powers that be. And that would almost certainly mean its value will go up.

I remember someone mentioned that they can’t kill bitcoin because it would kill trust in digital money which would be bad for CBDC’s. I’ll tag on that they can’t kill it YET, but that time may indeed come.

Playing the odds, it is my opinion that you ought to have some bitcoin. Worst case is it goes to zero. Best case is sky is the limit. How much is up to you.

The next article will continue talking about economic collapse and demolition but with a wider net of other cryptocurrencies, most notably stablecoins and CBDC’s.

This is Chapter 27 of my new book, working title “The Industry Playbook: Corporate Cartels, Corruption and Crimes Against Humanity” that is being published online chapter by chapter.

The story of leaded gasoline is far worse than that of cigarettes. But fewer people seem to be aware of any of the details of this escapade of big industry. You and I have lead still in our bones to this day because of the actions of the people shown here.

In 1921, Thomas Midgley Jr., an engineer working at General Motors (GM), discovered that adding tetraethyl lead (TEL) to gasoline improved engine performance by having an anti-knock effect.

Midgley’s boss was Charles Kettering, the head of research at GM. The president and CEO was Alfred P. Sloan. Their names would go on to be best known today as being on the Memorial Sloan-Kettering Cancer Center. (What goes on there and in the wider cancer industry will be discussed later.)

It wasn’t just GM involved. By 1920, the du Pont family owned more than 35 percent of GM shares. So Du Pont was intimately involved from the beginning. We’ll also hear more about Du Pont in a later chapter.

Standard Oil of New Jersey was also involved. They merged with Standard Oil of New York becoming what is known today as Exxon, the largest player of the original monopoly of Standard Oil that had been broken up.

These companies and their researchers said that the lead from gasoline wouldn’t harm anyone. Some of them probably believed that was the case. The common refrain, that the amounts used would be too small to hurt anyone, was the company line.

The result was that massive amounts of lead were spread across the entire world through the use of cars and other vehicles.

The dangers of lead were already known back when they started using it. Even the ancient Greeks thousands of years ago where aware of what lead could do.

Lead is linked to lower IQ, heart disease, cancer, many other diseases, and even rises in violent crime and other behavioral issues.

It easily contaminants the air, water and soil. This leads to bioaccumulation as it does not break down, being one of the periodic elements. The estimated 7 million tons of lead burned in gasoline are now spread throughout the environment. A 1983 report by Britain’s Royal Commission on Environmental Pollution stated that “it is doubtful whether any part of the earth’s surface or any form of life remains uncontaminated by anthropogenic lead.”

A 1985 EPA study estimated 5,000 Americans died annually from lead-related heart disease before the phase-out occurred.

Leaded gasoline’s eventual USA banning lead to a drop in mean blood-lead levels of 75 percent. Understand that between 1927 and 1987 every single person was exposed to toxic levels of lead. This was most damaging to children, including babies in the womb.

But other countries continued to use it longer. Venezuela sold only leaded gasoline until 1999. Sixty-three percent of newborn children contained levels of lead in excess of the safe levels established by the government there.

An estimated 90% of the lead in the atmosphere is from gasoline. Other areas like mining and lead based paints contribute a minor amount in comparison.

All these dangers were denied and covered up by industry from the very beginning.

They Knew the Dangers of Lead When They Started Using TEL

Tetraethyl lead was first discovered by a German Chemist in 1854. It wasn’t used commercially because of “its known deadliness.” For over sixty years, it had no use until Midgley found one for it.

William Mansfield Clark, lab director in the US Public Health Service, had written the assistant Surgeon General A.M. Stimson when Du Pont’s production first got underway. He said TEL was a “serious menace to public health” and that reports were coming in that “several very serious cases of lead poisoning have resulted” from the plant’s production.

In turn, the US Surgeon General, H.S. Cumming wrote to Pierre du Pont in December 1922, “Inasmuch as it is understood that when employed in gasoline engines, this substance will add a finely divided and nondiffusible form of lead to exhaust gases, and furthermore, since lead poisoning in human beings is of the cumulative type resulting frequently from the daily intake of minute quantities, it seems pertinent to inquire whether there might not be a decided health hazard associated with the extensive use of lead tetraethyl in engines.”

Midgley himself was suffering from lead poisoning in 1923. “After about a year’s work in organic lead I find that my lungs have been affected and that it is necessary to drop all work and get a large supply of fresh air,” he wrote.

Leaded Gasoline was Never Needed, in fact Inferior from the Very Beginning

Not only were the dangers known, but the benefits weren’t even that great. Other additives to gasoline functioned in much the same way, in fact many are superior. Ethanol, better known as alcohol, is used instead of lead today.

Ethanol could be used back then. An article in Scientific American said in 1918 that, “It is now definitely established that alcohol can be blended with gasoline to produce a suitable motor fuel.”

Unfortunately, ethanol had a fatal flaw as far as industry was concerned. It couldn’t be patented. This and other additives were suppressed and smeared by the industry.

In fact, ethanol might have been used to power cars completely without oil involved at all! Kitman wrote, “In 1907 and 1908 the US Geological Survey and the Navy performed 2,000 tests on alcohol and gasoline engines in Norfolk, Virginia, and St. Louis, concluding that higher engine compression could be achieved with alcohol than with gasoline. They noted a complete absence of smoke and disagreeable odors.”

Henry Ford’s Model A car could be adjusted from the dashboard to run on gasoline or ethanol. But this simply wouldn’t do for the growing oil industry.