I’m going to be publishing online my new book, working title “The Industry Playbook: Corporate Cartels, Corruption and Crimes Against Humanity” chapter by chapter, with the plans of officially compiling it into a book and publishing it down the road.

RICO stands for Racketeer Influenced and Corrupt Organizations. This was a major part of the US Organized Crime Control Act passed in 1970. While it was designed to be able to take down the mafia, RICO has since been used against big businesses.

Sadly, many big businesses operate similarly as organized crime. It is organized. And it is criminal. Big Tobacco was no different. The defendants in this case included the companies, Philip Morris, R. J. Reynolds, Brown and Williamson, Lorillard, Liggett, American Tobacco, Altria, and British American Tobacco. The defendants also include the Council for Tobacco Research and the Tobacco Institute which were essentially an industry PR/Scientific front group and lobbying group respectively.

Judge Gladys Kessler oversaw the RICO case. In 2003 she issued her decision in the RICO case finding in a 1,683-page opinion.

“[O]ver the course of 50 years, defendants lied, misrepresented, and deceived the American public, including smokers and the young people they avidly sought as ‘replacement smokers,’ about the devastating health effects of smoking and environmental tobacco smoke.”

The companies “suppressed research, they destroyed documents, they manipulated the use of nicotine so as to increase and perpetuate addiction…and they abused the legal system in order to achieve their goal—to make money with little if any regard for individual illness or suffering, soaring health care costs, or the integrity of the legal system.”

Armed with this knowledge we can then dive into the set of strategies and tactics described often as the “Tobacco Playbook” from which this section of the book takes its name. Quite simply, this was because Big Tobacco were the ones that pioneered many of the methods.

The Union of Concerned Scientists, the group that I first saw sharing that this practice was engaged in widely, instead refers to it as the “Disinformation Playbook.” That’s because one of the main overall strategies involved, to put out information with intent to deceive.

But it does go beyond disinformation, which is why I’ve gone with the term industry playbook. Why do industries use it? Simply because this playbook is profitable. Despite some awareness of the strategies in the playbook, they still continue to work.

It is also because it is not a static playbook. Strategies that don’t work are thrown out. Strategies that do work are used again and again. Furthermore, they are updated for new technology.

Just think, all of Big Tobacco’s crimes as covered in the RICO case came from pretty much exclusively in the pre-internet world.

Besides profits for the companies, what are the results of this? The stat is a bit old from 1995, but relevant. “[T]he number of people killed by tobacco in the United States was 502,000 of whom 214,000 were aged between thirty-five and sixty-nine. On average, each of these could have expected to live twenty-three years longer. In view of these alarming numbers, it seems to me that the still-prospering tobacco industry poses a proven threat to health and life that is many thousand times greater than the potential of bio-terrorism,” said Max F. Perutz, a Nobel prize winner in chemistry.

A 2014 US Department of Human Health and Services report shared that 20,830,000 people were killed prematurely by tobacco related disease in the fifty years since the Surgeon General’s original report on tobacco. The annual costs of smoking on disease are estimated around $300 billion.

Only with more knowledge and awareness can these strategies possibly stop working. Closing legal loopholes and more will be discussed later as well but in any case, it is more awareness and knowledge that would lead to such possible changes.

In this first part, I’ll discuss the following areas, including how they overlap:

Monopoly Power

Advertising

Public Relations

Smear Campaigns

Weaponization of Values

Advocacy Front Groups

Infiltrating Institutions

Influencing Science

Ideological Allies

Destroying Evidence

Lobbying and Buying Politicians

Controlling Regulation

Legal Defense

Influencing Journalism

Going Worldwide

Leverage through Diversification

Up to Old (and New) Tricks

The vast majority of this section of this book is based on The Cigarette Century by Allan M. Brandt, a Pulitzer Prize finalist. The Times Literary Supplement called this, “A masterpiece of medical history.” It features a whopping 1550 references and thus is a very deep look into what is one of the most important case studies of history.

I highly recommend reading The Cigarette Century if you’d like to go even deeper. While the purpose of Brandt’s book is to cover the entire history of the cigarette industry up until it was published in 2007, our purposes here are somewhat different.

The aim here is not just to cover the history, though you’ll get plenty of that, but show you how these strategies and tactics are purposefully used. Some of the dates and events that occurred will be repeated across chapters as those are relevant to different playbook strategies. Understanding their genesis with Big Tobacco helps you to spot them used everywhere else.

Key Takeaways on Big Tobacco’s Crimes and The Playbook Metaphor

The tobacco companies, including their industry fronts, lost a RICO case meaning that they functioned as organized crime, similar to the mafia.

For over fifty years the tobacco companies denied, distorted and minimized the health consequences, that their own research showed existed.

They attacked and discredited scientific links between cigarettes and disease.

For over forty years they were aware of tobacco’s addictiveness due to nicotine, but they denied cigarette smoking was addictive.

Not only did they downplay nicotine’s addictiveness, but they were manipulating nicotine levels through a variety of means, while lying saying they did no such thing.

They promoted light and low tar cigarettes as healthier options with false and misleading claims.

They specifically targeted young people through a variety of marketing campaigns as these were a highly sought-after demographic.

Their research showed that secondhand smoke, also known as environmental tobacco smoke (ETS), was hazardous to non-smokers. They suppressed and undermined this research.

They even destroyed documents, or shielding documents through legal means, to protect their profits and PR agenda.

Over fifty years, throughout which Big Tobacco denied and distorted harms, an estimated 20 million people died prematurely from tobacco-related diseases.

The playbook is a metaphor that is used to describe the plays that an industry engages in to disinform, protect profits, and obtain more power. In the coming pages seventeen specific strategies are described.

Please leave any comments or questions below. Feel free to share it with anyone you’d like.

…but it might be better described as Central Banker Digital Control.

It is a cryptocurrency, but instead of the trustless decentralization that Bitcoin relies on, it’s just more of the same of what we know and hate about fiat currency.

Having knowledge of CBDC’s and what’s happening is extremely important to the crypto world. So let’s dive in…

7 countries (including US and UK) in advanced stages of R&D

30 countries in exploratory stages of R&D

10 countries exploring the idea

2 countries which launched and discontinued them

This article mentions that the pandemic accelerated the timeline by at least five years. “There is also no doubt in our mind that a major central bank will soon launch a digital currency and we expect this to happen within the next three years,” said Guardtime, a European blockchain company.

There’s a good chance of it happening faster than that.

(What does a virus have to do with digital currency? Must just be a conspiracy theory that you shouldn’t pay attention to. OR if you do want to listen to the conspiracy factualists you can look at the evidence that the virus was used a smokescreen for the economic shenanigans all along.)

They mention a different stat of 60 central banks are exploring CBDCs.

There are 195 countries in the world.

Do you think this has a possibility of NOT happening at this stage?

The central bankers all work together. This is specifically what the Bank of International Settlements (BIS) is all about. You know that very hush-hush supranational beyond-government agency that began after WWI.

The former Bank of England and Canada Governor Mark Carney, at the BIS, said “We should be wary of path dependence and locking in existing advantages of tech companies via the payments system. There are powerful network effects in both social networks and money. If combined, these could be mutually reinforcing. Convenience once established may be hard to unwind in the Uberisation of money.”

In other words, we bankers need to make sure we control stablecoins before it’s too late.

They can’t allow for stablecoins that they don’t have control of, can they?

Here is the BIS General Manager Agustín Carstens speaking in October 2020 about CBDC’s. This is what it is really about.

“Our analysis on CBDC in particular for…general use. We tend to establish the equivalence with cash. And there is a huge difference there. For example, in cash we don’t know for example whose using a $100 bill today. We don’t know whose using a 1000 peso bill today. The key difference with the CBDC is that central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability [aka money]. And also we will have the technology to enforce that. Those two issues are extremely important and that makes a huge difference to what cash is.” (emphasis added)

This was the plan in “going direct.” This is a major step that is required for the “Great Reset.”

Doesn’t this bode ill for cryptocurrencies then?

Sort of. Yes they will make sure they have co-opted the system. In one sense this is the biggest threat to the space, particularly stablecoins (and one possible “solution” is the whole Tether scam unraveling to allow them to do it.) That’s in time though…

There’s still a golden window happening right now that will not be open long. Get in, get your profits, and get out (at least to a degree).

But on the flip side, crypto investments are not going away! The space will not just be CBDC’s. Those who want to control things have need of certain crypto projects to move their agendas along as well.

And this is what my Crypto Crash Course can help you with. Stablecoins (not CBDC’s) are an important part of this picture right now.

You must understand the fight going on for economics, how co-opting and steering the narrative works.

You can get in now, of your own free will and gain from doing so.

Or you can be forced to later when CBDC’s are crammed down your throat, and when you must have a good citizen social score, get your annual (semiannual/quarterly?) booster shots, or else your money is turned off.

That is the dream (aka nightmare) of the total control grid totalitarian plan.

After all, it’s an open conspiracy. All you have to do is listen to what people like Carstens are saying.

The good news is there is a light side to crypto that is specifically trying to ensure that doesn’t happen. The libertarian ethic is hard at work in the crypto space, laughing at the bankers and their silly dreams.

It’s not just an information war but a full on economic one too.

I just finished up the Advanced Track on the Crypto Crash Course. That’s now uploaded and available for paid members.

And that means that the pre-production discount is going away soon. I’ll leave it up until the end of the week but then the course goes up to its normal price.

(The Beginner Track will still be freely available.)

There’s an old adage to “follow the money” that I certainly put to use.

(A similarly useful one that I came up with the other day was “follow the transparency”. Who is transparent? Who is not? This is a useful shortcut for figuring out who to listen to and trust.)

Today, I’m not just talking about following the money regarding researching…but literally following the money with your investments.

Let’s talk about BlackRock.

BlackRock is a huge firm that owns significant chunks of every single big corporation. They work directly with the US treasury and the Federal Reserve ever since the pandemic hit.

Because of this Bloomberg called them, “the fourth branch of government.”

Remember what the World Economic Forum “You’ll own nothing and be happy.” BlackRock (and Bloomberg) are both partners in the WEF.

Well, someone is going to own stuff. Who do you think that will be? Do you think these titans of capitalism are going to relinquish what they own? Do you think that’s the game plan?

BlackRock is in large part the means by which the stock market is flying high from the Fed’s money printing.

There’s a good chance I’ll do a comprehensive overview of this company in the future. Today, I’ll just focus on them and Bitcoin.

Does BlackRock own Bitcoin?

Rick Rieder, the chief investment officer of global fixed income at BlackRock, said that BlackRock had “begun to dabble” in bitcoin, but didn’t give details on how much.

Consider they have $9 trillion in assets under management, and Bitcoin itself only has a $740 billion market cap.

They also own Bitcoin indirectly. BlackRock owns a 14.56% stake, the largest owned by anyone, of Michael Saylor’s MicroStrategy firm. If you haven’t heard of Saylor, he’s one of the main guys going around even in the mainstream media talking about the long-term bullish scenario for Bitcoin.

This quote from that article is worth noting “BlackRock Chief Executive Officer Larry Fink had said at the Council of Foreign Relations in December that bitcoin is seeing giant moves every day and could possibly evolve into a global market.”

Granted, BlackRock could be doing a whole lot more in the space. But that they are involved right now in growing ways is a bullish sign to me.

Of course, the coming CBDC’s could disrupt the crypto field. Considering that BlackRock is tied to the Fed that is worth considering. More on the topic next week…

I’m going to be publishing online my new book, working title “The Industry Playbook: Corporate Cartels, Corruption and Crimes Against Humanity” chapter by chapter, with the plans of officially compiling it into a book and publishing it down the road.

I originally started this project just as a plan to dive into Big Tobacco and their shady tactics, as a means to understand the history for what we see in other industries today. (And a big shout out to those donors who funded me to kick start the idea!)

Fortunately, or unfortunately depending on how you look at it, I tend to be thorough. And so, this project grew and grew. As it stands now this project is ambitious in scope. But I felt it was necessary for people to understand to breadth and depth of these strategies across industries.

To have a narrow lens and see just a bit of this picture can stop you from seeing how the game is truly played. As such, this book is divided across seven parts.

Part 1 – The Tobacco Playbook

Part 2 – Breaking Free of Big Tobacco

Part 3 – Other Industry Examples

Part 4 – The Monsanto Playbook

Part 5 – The Pharma Playbook

Part 6 – The BIG Players

Part 7 – The People’s Playbook

The Tobacco Playbook dives into the history of the cigarette companies. Their rise to power including how they were pioneers in the space of controlling scientific opinion, PR, advertising, infiltrating legislatures and regulators, influencing journalists and much more.

This details such sections as monopoly power, smear campaigns, advocacy front groups, legal defenses and more. The aim is to give you a clear outline of the many strategies employed by Big Tobacco in increasing their profits at the cost of human health and wellbeing.

The next part, Breaking Free of Big Tobacco, shows the flip side. Big Tobacco did ultimately lose some of its power. What caused that to happen? The playbook as used by industry does not guarantee an outcome. Here we explored the crucial battles and strategies of the people against the companies.

In Part 3, Other Industry Examples, we quickly explore a number of other industries to show the widespread prevalence of use of the playbook. This section covers asbestos causing cancer, water fluoridation, lead in gasoline, various chemicals and pesticides, telecom, oil and more.

Here you’ll see the industry playbook is aptly named as it is used in virtually every large industry that exists. The problem is systemic. The result is a sociopathic drive towards profit at the cost of human health.

Part 4 covers Monsanto, which was frequently rated the evilest corporation in the world. As you’ll come to see, their nickname of Monsatan was quite well earned. With this deeper dive you’ll find how the playbook has specifically been updated for the 21st century and use of the internet.

Part 5 covers the pharmaceutical industry. This part is the largest in the book and is based on much of an earlier project I engaged in called Medical Monopoly Musings. Several books can and have been published on this topic alone, but I’ll do my best to summarize the most critical understandings. The industry has been around a long time so many examples from the past will be shown. But there will be a focus on more contemporary examples, with the playbook used at an even larger scale. Big Tobacco lost power eventually. Big Pharma has continued to gain.

Then in part 6, I switch gears. There’s a question worth asking. Why does industry after industry use the same playbook? Here we explain the profit motive and sociopathic systems at play. And we dive deeper into the main players, those who move between industries, the PR firms, the lawyers and the lobbyists. If we liken the playbook to football, these big players are the coaches and quarterbacks. It is every bit as important as understanding the plays, to understand the players.

This section will also dive into the regulators, those that supposedly protect the people from nefarious industry efforts. Unfortunately, you’ll find the revolving door in full operation leading to these being predominately captured agencies.

Finally, in part 7, I continue the work only started in part 2. I call this The People’s Playbook. It is not enough to know what the industries engage in. It is not enough to be able to point to the players. We must accurately perceive what is ultimately successful in fighting against them. What actually works? And who is currently doing good work?

There is a flow from one part to the next. But you don’t have to read the book in the order it’s laid out. Feel free to skip around as you best see fit.

In addition, I’ve designed this large book with skimmers in mind. In our world of social media and short attention spans, I’ve done the best I can to summarize the findings here. Each chapter concludes with a short section on Key Takeaways.

Even if you plan to read the whole book (thank you so much for lending me that much attention!) I’d recommend the following. Read once through all the key takeaways before reading the rest of the book. This will give you the big picture framework and insight to see how all the sections fit together. It’ll help you to understand even better when you dive deeper into the details.

[Online publishing edit: obviously, the skipping around or viewing all the key takeaways first cannot be done at this time. But I left this part available here to give you an idea of what is coming.]

Please leave any comments or questions below. Feel free to share it with anyone you’d like.

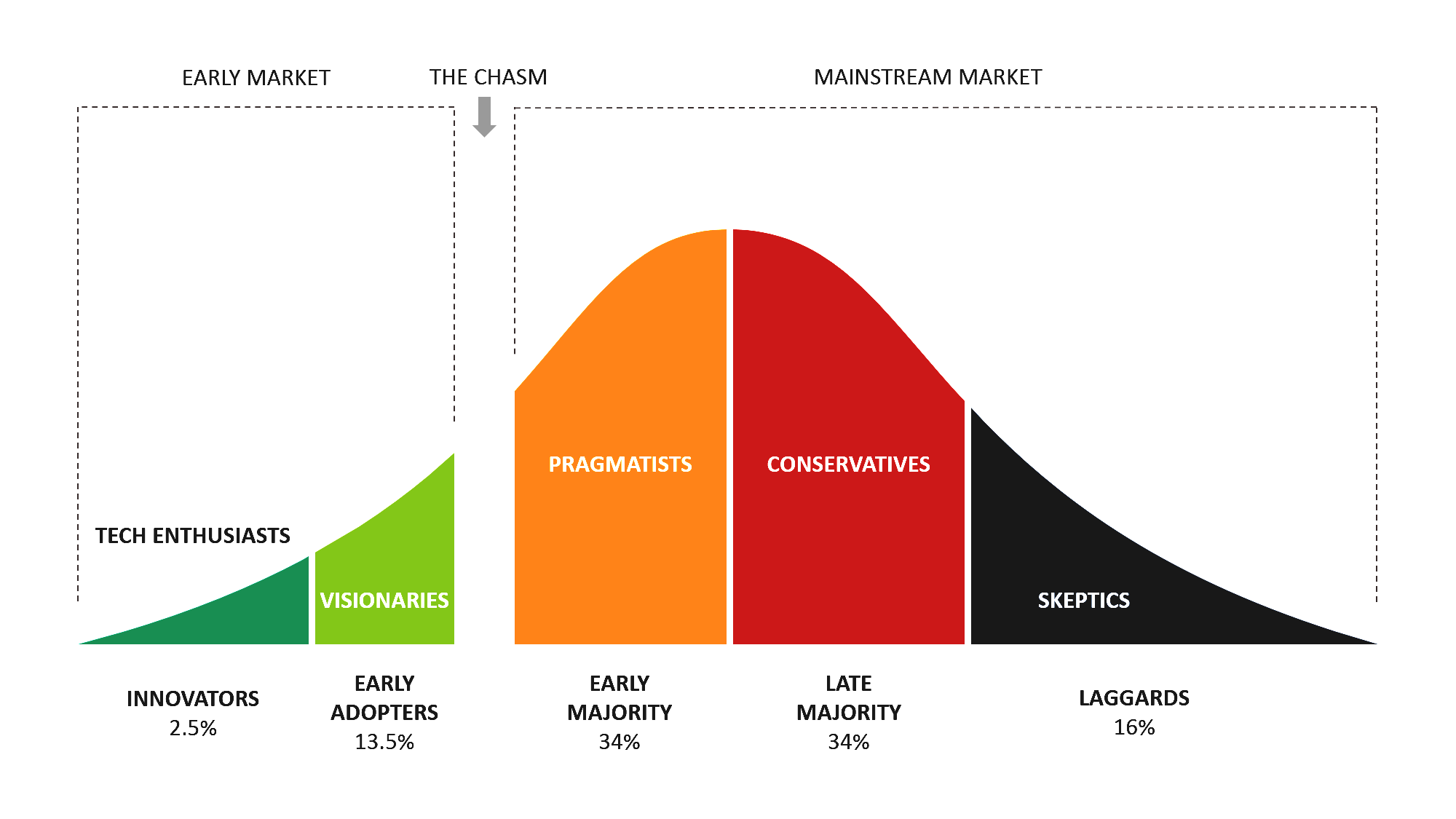

There’s a good chance there are half a billion people using crypto by the time 2021 ends.

It’s not just people.

With El Salvador it’s even a sovereign country. (When will the next one join in?)

And also hedge funds, banks, companies and more.

We’re crossing that chasm.

If you understand anything about “network effects” you’ll recognize how all these people and institutions piling in will drive prices up.

The FOMO that sets in with the next leg up will likely be legendary. Tulips got nothing on Bitcoin 😉

And the third point is the technology.

I know, I know, it’s tough to wrap your mind around how all this works. Are you an engineer? Are you into cryptography? If not, it might be tough to understand these things.

Wait, your wallet doesn’t actually hold the coins? Wait there are no actual coins just a public ledger?

I’m still struggling with it as I stretch my knowledge base!

What makes proof-of-stake different from proof-of-work? How will impermanent loss affect your liquidity pools…and thus the money you make or lose? What is seigniorage have to do with algorithmic stablecoins?

As I’ve said it gets complicated quickly!

But the possible benefits of this technology also stretch the mind.

In the DeFi space (decentralized finance, aka no bankers involved) there are things such as self-paying loans.

These can’t possibly work in the world of centralized finance. But they can work in the world of smart contracts.

It’s basically a new entity like a corporation or LLC…except that instead of owners it’s “an open-source blockchain protocol governed by a set of rules, created by its elected members, that automatically execute certain actions without the need for intermediaries.”

There’s a crypto token I’m looking at right now that offers a 7.33% yield. That’s a pretty good number to make on your money. Except it’s not an annual yield. That’s in just five days.

Sounds like a ponzi scheme, right? Except that there is a ground floor price on the token.

I could go on and on.

But here’s my point. Any one of these things (inflation hedge, adoption, and technology) would be a good reason to get some crypto.

All three of them together? Well, that’s why I’ve devoted so much of my time to the topic this year. It’s powerful.

But you could just as easily find ones today saying much the same thing.

So let me state my position. I think it is healthy to be paranoid. “They” are out to get you.

I was telling a friend the other day how I really want to use the headline “How Conspiracy Theorizing Made Me Healthy and Wealthy” but haven’t done so yet.

Healthy in that you recognize the “Great Poisoning” going on. I could make arguments for or against this being on purpose, or just a systematic result. Regardless of that, it is very helpful to recognize that it is happening everywhere and is the primary reason for the rise in chronic disease.

Wealthy in that if you understand the markets are rigged, you can play along with them. I wouldn’t call myself wealthy (yet) but neither am I doing poorly either.

If you understand a thing or two about the powers-that-be mindset and read the propaganda which is out there in the open, I feel like you can profit from that paranoia.

Just a reminder that while there are paid options, there’s also the 100% free Beginner Track you can get started with today.

Back to the topic of governments banning crypto.

What do we see in smaller countries? Crypto gets banned…and the people start buying it more. Why? Because it is a superior store of value compared to their country’s currency.

I don’t know exactly when this will happen. It could be before the end of the year. It could be out in 2022. At this point I’m leaning a bit towards the latter. (It will depend when things start going up, up, up…)

This will wipe out many, many people, just another step in the greatest wealth transfer ever to occur.

Then they’ll reboot it using their CBDC’s (central banker digital currencies).

That appears to be the gameplan.

Even if that happens, a case could be made that Bitcoin will still be around and quite valuable. But that’s a whole other topic I’ll cover another time.

On the flipside, it does appear that “the narrative” is showing some greater cracks. I’ll talk more about that in another message, including what that could mean for crypto and the world at large.

Ultimately, that would be more bullish for humanity, though there is a big caveat there.

What I recommend is you get in, get your profits, and get out (partially anyway).

I’m going to be publishing online my new book, working title “The Industry Playbook: Corporate Cartels, Corruption and Crimes Against Humanity” chapter by chapter, with the plans of officially compiling it into a book and publishing it down the road.

Speaking about Big Tobacco, Judge Haddon Lee Sarokin stated, “A jury might reasonably conclude that defendants in particular, and the industry in general, intentionally and willfully ignored the known health consequences to consumers from the sale of their products; that their so-called investigation into the risks was not to find the truth and inform their consumers but merely an effort to determine if they could refute the adverse reports and maintain their sales. Defendants were confronted with a choice between the health and lives of the consumers and profits and the jury could reasonably conclude that the industry chose profits. Health of consumers does not receive even passing mention in the internal documents of the defendants, except as to the advantage to be gained by expressing such concern publicly.”

“The evidence presented also permits the jury to find a tobacco industry conspiracy, vast in its scope, devious in its purpose and devastating in its results,” continued Sarokin. “The jury may reasonably conclude that defendants were members of and engaged in that conspiracy with full knowledge and disregard for the illness and death it would cause.”

A conspiracy vast in its scope and devious in its purpose. That is what this book is about.

Those who do not learn history are doomed to repeat it. We’ve all heard this phrase. But as it’s become somewhat cliché, few really aim to understand history, especially what I would call its seedy underbelly.

If history is written by the victors, you must dig below the surface, past the whitewashing and PR spin that the victors engage in.

Large corporations, such as those companies that make up Big Tobacco, make tons of money. I’ve got no problems with that, owning for-profit companies myself though far smaller in scale. Profits are used to secure more profits. Again, this is no real indictment yet.

While advertising is one such tool, and easily seen, it is the behind-the-scenes strategies that are far more powerful. This “marketing” of science, legality, journalism, and influence at the highest levels of government is ultimately far more important to their bottom line than ads on billboards, magazines and TV.

And this is where I say the line is crossed.

In the world of mega-corporations, especially publicly owned, it is simply a matter of cost-benefit analysis. It would be unprofitable and unwise to not engage in such tactics. In fact, it would be illegal because of their fiduciary responsibility to shareholders to maximize profits.

When cutting corners and shady practices pay, you can bet that we’ll see more of those. And that is exactly what we’ve seen over the decades.

When actual criminal activity pays, you can bet that we’ll see more crime. It would be logical and profitable to engage in crime if you get away with it time and time again. Or be punished with a fee less than the profits made. That makes it just a business expense.

With more profits, you have more money by which to do even more. These ill-gotten gains give their possessors more power to continue further down the same route. Not to mention, once you’ve made one step in the direction of lying, cheating, and covering up, the next step is more obvious.

For these reasons, we’ve seen an expansion of the industry playbook over time rather than a shrinking of it. The strategies are more numerous. The plays are done even bigger in scale.

Everyone I know is vaguely aware of what Big Tobacco did in peddling cigarettes. VAGUELY being the key word.

Ask yourself how did they get away with being hugely profitable for decades and decades once the science was clear about the risks?

I would argue you must understand the details. Why? Not because you’re likely to get tricked by Big Tobacco in the future (though as we’ll see later the youth of today are being tricked by the exact same industry). Instead, my aim is not for you to just understand Big Tobacco, but because these same strategies and tactics are used by industry after industry.

Many industries are successfully using the exact same methods today and most people are none the wiser.

The average person has not learned THIS history. It’s certainly not being taught in schools.

While Big Tobacco has lost some of its once triumphant power, we must understand how the system operated and still operates. There is no doubt that Big Tobacco did lose key battles. Just like a military at war, some learned from such loses.

The PR firms that Big Tobacco worked with learned. The lawyers learned. Those that would control scientific opinion learned. Those that would buy politicians and regulators learned.

This is why “a conspiracy vast in its scope, devious in its purpose” appears to be going on. Like a disease of corruption, it has spread and infected the top businesses and echelons of power the world over.

It’s not one big conspiracy, but a bunch of smaller ones, because the problem is systemic. To dismiss such as conspiracy theories as is often done is foolish. Such a tactic of labeling things that way is in fact used by those in power.

That’s why I wrote The Industry Playbook. It is a user’s manual for the public of those tactics and strategies that are used to influence how they see the world. A worldview that protects and increases big companies’ bottom lines, often while sacrificing health and wellbeing of the public at large.

Their goal is to steer science. Their goal is to steer regulation. Their goal is to steer legislation. Their goal is to steer not just public opinion, but professional opinion as well, as that is the key to steering the rest.

Big companies have accomplished these goals far more than they have failed at them.

The goal of The Industry Playbook, as I’ve laid it out here, is to give you details on the exact plays as used by Big Tobacco as our first example, then industry after industry from asbestos to lead in gasoline, chemicals to agriculture, pharmaceuticals and more, so that you become aware of them.

Or better yet, with this exposure, to become immune to them.

Education of the populace is ultimately what is necessary for such methods to stop working. If everyone could call out such tactics on first sight, they would lose effectiveness. If we all laughed at the blatant PR spin, the obvious industry misled science, the recognizable political favors, some of these wrongs could be righted.

Too many people have an unthinkability bias when it comes to this stuff. They can’t even imagine the state of our world is as bad as it truly is. I feel that is for two reasons. First, most people don’t see how it could be done, and that’s for lack of understanding how the playbook works.

Make no mistake, the methods described herein have been worth trillions of dollars.

Secondly, most people being good-natured, this kind of evil is unthinkable. I use the word evil purposefully. When you put profit above human misery, lying to do so, that qualifies as evil in my book. So I say it is only by looking evil in the eye and not blinking that we can hope to transform it.

The evidence is dark. But the evidence is there, and all you need to do is scratch below the shiny façade to find it.

There’s a saying that the greatest trick the Devil ever pulled was convincing the world he didn’t exist. Industry after industry would have you believe these strategies didn’t exist, that they were being above-board with everything they say and do.

But the evidence is more often than not to the contrary. So much so that the default position of skepticism for anything said by big business, it’s PR people and all the journalists, scientists, and politicians influenced by them, is the best route to go.

Corruption is a systemic problem that gives rise to crimes against humanity. This book will show you how and why.

Please leave any comments or questions below. Feel free to share it with anyone you’d like.

The inspiration for this article was ignited by a video from Clif High. I’ve been following Clif’s work for maybe a year and a half or two years now. He is definitely off the deep end…and I think there is some genius there otherwise I wouldn’t continue to follow him. If nothing else, it is a fascinating perspective.

This immediately caught my attention, helping weave together what were disparate threads in my mind.

Now there’s a lot in that video that he talks about if you watch it that you might not agree with. Here’s the thing. Regardless of the specific scenarios, I think this is a useful model.

First of all, we are without a doubt going through civilization collapse. Now, this does not necessarily mean the “apocalypse” is upon us, 90% of humanity is going to die, we’re going back to living in caves, etc. It COULD mean that…in time especially with cascading effects. That is absolutely a possibility.

Just because there is an emotional or unthinkability bias against these possibilities that stop most people from seeing them, doesn’t mean it’s not actually there.

Secondly, there is a strong chance of much of the ‘collapsing’ of the collapse being mitigated, thus the collapse is short-lived, or localized, humanity bouncing back. In this sense the collapse might have more to do with institutions and cultural norms, then much of the technological underpinnings of our society. The magnitude of this happening is still HUGE.

If you doubt this…observe the world flip flop from conspiracy theory to leading theory about the origins of the virus…and people begin to see the financial ties of individuals involved.

Of course the damage control spinners are working overtime! Interesting times nonetheless…

Still, since we’re talking civilization collapse, for some background it can be worth studying the collapse of the Roman Empire, the Mayans, and many others that have come before. There are strong parallels available.

So what is this Civilization Collapse Stack?

This is a way of thinking through the possibilities of how this can play out.

If it gets really, really, really bad (aka Mad Max world as Clif High mentions) then we’re all the way down to the bottom of the stack.

If it’s not that bad, we’re at the top of the stack, not even collapsing just stepping into the future from here.

How far we go down the stack remains to be seen, but by being aware you can be better prepared.

And this doesn’t just have to do with survival but thriving which basically leads us into investments, along with adaptability.

So let’s dive into his stack and I’ll riff on it.

PB/Food/Mobility

Have you seen Mad Max? That’s a description of the worst things could go in. The Walking Dead minus the zombies is a likely more accurate description that gets rid of the flamboyancy of Mad Max.

PB stands for lead, aka ammo and guns. Food is a descriptor of not just food, but water and everything else you need to survive. Mobility is being able to move as that could be the difference between life and death.

An important aspect of these assets are not just that you need them to survive but they are good for barter. That you can trade any of these goods for other things you need is important in this world where any and all currency might not be worth anything. (I’m reminded of the image of people burning cash in the Weimar republic in order to stay warm.)

RE – Subsistence

RE stands for real estate. Perhaps more importantly here, can you live off your land? Grow your own food? (Can you defend it…to go back a level?) Depending on how difficult things are and for how long the ability to meet your survival based on where you’re at could be especially useful.

Note that this contrasts with mobility. Best bet would be to have a self-sustaining place as well as mobility.

Real estate also acts as a worthy investment. Right now, with asset inflation real estate is going up, up, up. There is not likely to be a change in that anytime soon unless civilization collapses down the stack. In that sense with a good home you can be set either way.

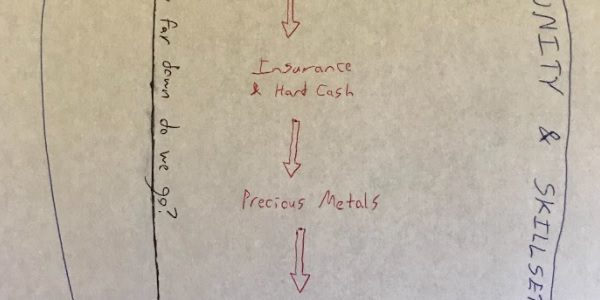

AU/AG

Those are the chemical symbols for gold and silver. Precious metals have always held value throughout almost all human civilization. This trend could stop at some point but is not likely. I like to call this the “old money” play.

If the US dollar goes into hyperinflation and becomes worthless this would be a rock-solid hedge against that.

The interesting thing going on with these is that even though ALL other assets are seeing inflation, it has not happened in precious metals. Why? There is significant evidence of the manipulation of these markets. They likely will have their time to shine in the sun again but can’t say for sure when that will happen.

Having some of these on hand in small denominations allows for trading in any world that isn’t solely about short-term survival.

Physical Cash

The interesting thing about the US dollar is that most of it is already digital. Nothing more than bits on computers. There is a case to be made that actual physical cash could be more valuable than the digital version. The fact that cash is not tracked like everything soon will be makes a case for this.

At the very least it is useful to have cash on hand for any variety of short-term emergency situations.

Cryptos

We’re going through the Great Reset, an economic transition. As I’ve talked about before that appears to be coming one way or another. Now we may go down the civilization collapse stack before that fully happens. Or it could be a more seamless transition depending.

Cryptos obviously have no use in a Mad Max world. But they are a worthy investment in many versions of “Future World.”

These are the central bankers rolling out their versions of centralized, more highly controlled, technocratic cryptocurrencies. The technical name is CBDC’s, central banker digital currencies. China is already experimenting with their version. The Fed is soon to release prototypes of its Digital Dollar.

The goal is to not go through civilization collapse but steer us into this system in the making. And it’s not just these but there’s reason to believe the powers-that-be are behind some of the popular crypto technologies today.

What most of the powers-that-be seem to want is a near seamless step into this control grid world.

Though an argument can be made that much needs to collapse before the world (like the freer parts of the USA) are ready to go there. If that’s the case then collapsing is desired and may receive “assistance.”

My Version of the Civilization Collapse Stack

I see this a bit differently than Clif. I see these two top parts of the stack more or less as split pathways. (Not that it’s all or nothing as these could fight it out for some time.)

Here’s my drawing.

A key point is that there is what we may call “normality” the pre-pandemic world. So here you see a splitting of the possible futures.

Look, I think the US dollar is doomed as the national reserve currency. It may be re-born as the digital dollar. Something else could take it’s place. But it’s chances of remaining long term the world’s reserve currency are doubtful, based off of very solid historical trends and the facts that show up today.

I highly doubt we step seamlessly in the future from this point. Instead, it’s a matter of how far down the collapse stack we end up going. If we collapse hard down the stack, then currency isn’t so much a concern.

If we don’t collapse as hard, or we do but go through a “Great Rebuild,” it is a cryptocurrency future in one form or another. That’s the way I see it.

Collapse – A Phenomenon Spanning Time and Location

Yes, we’re a globalized world right now. That is the main thing, with all it entails, that makes our current position different than the Roman Empire collapsing.

That adds so much complexity that predicting things is tough to do. That’s why this principle-based look at civilization collapse is useful. It simplifies the complexity.

And one of the most useful things to know about civilization collapse is that that doesn’t happen all at once.

Civilization collapse is not an overnight thing. In fact, it could take more than my lifetime! But a fair guess is that the rest of the 2020’s are rocky.

There’s one other key point…

Collapse doesn’t affect every area across the globe the same either.

Over the past five years or so, it has gotten worse every single year.

Last year was a big step up from before. Not just California but the entire west coast up to Canada!

This year the state is drier than last year.

Fire season is just about to start once again…

What helped me out here? Surviving and thriving. Mobility and insurance came in handy here personally. And unfortunately, that makes many of the other things tougher to do. (I lost all my stockpile of survival goods for instance and had to start over.)

That’s the thing about this model. It’s not just civilization collapse but also useful for short-term emergencies too.

One thing I’m thankful for in the fire is that it stretched me out of my own unthinkability bias here. That it couldn’t happen to me. And thus, with this antifragile outlook, I feel more prepared to look at such scenarios as I’m laying out here.

Insurance of various types can help through many possibilities, which is why I added it to my chart. The thing is you must also trust those institutions to be there as well.

And in any case, survival goods and weaponry are a type of insurance. Being in cryptos has gotten me thinking a lot more about risk mitigation in many different ways.

There are more natural disasters happening. Remember how Texas froze this last winter?

Whether there is a grand solar minimum coming causing a mini ice age, it’s man-made changes causing cascading environmental effects, weather modification weaponry, or some combination of these factors I can’t say for sure. Probably all of them. What will effect where you live? Are you ready for that?

Another example. We just had the Colonial Pipeline Hack. Even though it was the owners that shut it down, not the hackers, it caused people to not be able to get gas, disrupting their lives.

Those are just a few minor examples. As the collapse occurs across multiple issues, these things exacerbate each other. For example, the fires happening during the pandemic/government edicts made things tougher.

It is completely possible that certain places (whole countries?) may collapse completely, while others function virtually untouched.

Certain places become Mad Max while others step straight in the future. It’s not fair, but it may be how it goes.

Community and Skillsets

I’ve added two meta categories to my drawing that encompass the whole stack.

The community of people you surround yourself with is important no matter what level we descend too. In addition, it can be useful to know people that specialize in different levels of this such as survival vs. investing.

Not to mention that investing in your community (which may mean your family, your friends, worthy charities, those fighting the good fight, etc.) is always worthwhile.

Then there are skillsets involved in the whole stack. At the bottom of the stack, the many branches of survival skills and subsistence living. Towards the top end more so on investing skills. And so much besides that.

Investing in your personal skillsets is always worthwhile. But not just the same old skillsets. With this model is a call to expand your proficiency into likely new skillsets.

What to Do with This?

Ask yourself: How prepared are you for these different levels of collapse?

I really don’t want to be promoting fear. Some describe me as cynical. But these are plenty of realistic scenarios worth thinking through. That’s why I put together this article, largely to sharpen my own thinking through them.

The best bet is to be ready for anything!

Unfortunately, that is not easy to do. So what do you do? Start at some bare basics at the bottom of the stack and work your way up. The specifics of preparations are beyond the scope of this article. There are places that cover that far better than I could at this time anyway.

Return to this model overtime to modify your positions, insurances, plans and assets as necessary.

What do you see as most likely? Least likely?

What is most harmful if you get it wrong? (If you miss out on a financial investment you can live with that, if you miss out on being able to feed yourself, not so much.)

It can easily be overwhelming. So what is one thing you can do, even today that is a step in the right direction?

I’ll be doing another article that looks at some of the existential threats on the horizon.

I’ve been talking a lot about cryptocurrencies lately and will continue to do so. One of the big topics that stops many people from getting involved is how safe are they?

Safety is an important question, but I want to change tracks a bit. How safe is your money in general? How safe is the ever-growing economic bubble we all live in? (Like a fish in water, most can’t see it.)

In this article we’ll be looking at several areas to dispel the myths of safety we are supposed to believe in, showing that such safety nets that we assume exist may not be there when we expect them to be, especially as this country continues to fall apart.

“To understand the state of our currencies, it is essential to realize that we live and transact in a transition time between two systems—amid a global currency war. The first system is the U.S. dollar, which has served as the global reserve currency since World War II…The second system is ‘in the invention room’ as we speak. Numerous parties throughout the developed and developing worlds—including members of the dollar syndicate—are attempting to bring up new digital transaction, payment and settlement systems…these unfolding developments represent a complex, confusing landscape for even the most sophisticated financial observer…The important thing to understand in this transition period is that many members of the global leadership do not intend to bring up a new currency system for use by the general population. Instead, they intend to end the use of currency as we know it, as part of a radical reengineering of our existing laws, finances, and culture. Their goal is the end of individual sovereignty—managed with technocracy and transaction systems that can operate without markets or currency in the classic sense, integrated with other heretofore separate control systems.”

I’ve touched on many of these areas before but aim to give a bigger picture looking at the unsustainability of our current system here in a two-fold way:

The system at large

Your dollars within the system

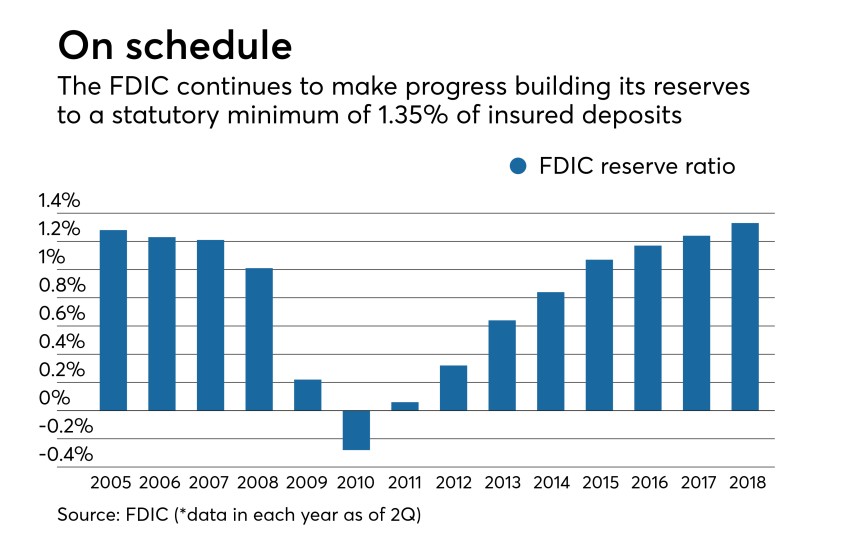

How Safe is the FDIC?

FDIC, the Federal Deposit Insurance Corporation, is what backs every bank account to the tune of $250,000 nowadays. Your money is safe in banks because the government guarantees it.

As their website says, FDIC is “an independent agency created by the Congress to maintain stability and public confidence in the nation’s financial system. The FDIC insures deposits…”

But do you believe in a guarantee when you know that our government is run as a criminal organization?

(After all, the Constitution is supposedly a series of government guarantees, but we can see these guarantees are all being whittled away.)

Here’s a history lesson. Another US insurance organization, the Federal Savings and Loan Insurance Corporation, became insolvent in the 1980’s savings and loan crisis.

It was “recapitalized” with taxpayer money, $15 billion in 1986 and $10.75 billion in 1987. Despite these efforts, by 1989 it was still broke and was gotten rid of. Its responsibilities were replaced by the FDIC. That crisis ultimately cost taxpayers $150 billion dollars.

So let’s look at the FDIC.

Did you know that the FDIC was $8 billion in the hole back in 2010 from the last big crisis and bank failures? They’ve since reversed that, but just how exactly are they insuring that your money stays in bank accounts when they themselves haven’t always had it?

Nothing fundamental was fixed after the 2008 crisis. The problems are all bigger now…just elsewhere besides mortgages.

That covers 400,800 accounts at the $250,000 limit. Of course, most people don’t have that much money. But of those that do, many have several different insured accounts at different institutions.

If a crisis bankrupted a federal insurance institution before, what are the chances of it happening again? I’d be willing to bet on it.

Bank Runs?

Investopedia defines a bank run as the following: “A bank run occurs when a large number of customers of a bank or other financial institution withdraw their deposits simultaneously over concerns of the bank’s solvency. As more people withdraw their funds, the probability of default increases, prompting more people to withdraw their deposits. In extreme cases, the bank’s reserves may not be sufficient to cover the withdrawals.”

If there is a demolition of the current system (whether controlled or uncontrolled) this is a potential consequence.

Oh, and regarding those reserves? I reported on this back in March of 2020. The Fed stated: “As announced on March 15, 2020, the Board reduced reserve requirement ratios to zero percent effective March 26, 2020. This action eliminated reserve requirements for all depository institutions.”

Banks aren’t required to hold any reserves anymore. Suspicious timing…What does a pandemic have to do with bank reserves? There’s no answer on the surface level which is why such a policy change got no mainstream coverage. But below the surface…everything.

I guess if we go fully digital there can’t really be a bank run?

…at least no one will SEE the bank run since all they need to do is transmit some bits over there and say we’re not allowing cash transactions anymore (because of the virus of course).

The FDIC is there to ensure that bank runs don’t happen. But what if the system is pushed to the point of collapse where FDIC goes with it.

The “good news” is there is a solution…

The Solution to Every Problem – Print More Money

The answer to any and all of these questions is to print more money. That seems to be our economic plan. That is what Modern Monetary Policy says to do.

Yes, the FDIC could be rescued from ANY failure by printing more money. But understand that comes at a cost, the dollars we all have get debased further.

Printing money acts as a hidden tax on the people. Congress doesn’t have to approve it. (Technically in the Constitution they approve budgets but that’s hardly how it actually works now.)

They don’t take it from you like they do with taxes, instead they just make any dollars you hold worth less.

In fact, with almost everything listed here the answer may be the same. Got a pandemic? Print more money. Going to war with China? Print more money. Climate change? Print more money. Alien invasion? Print more money.

It’s the magical solution to any threat, real or spun.

Why would they debase a currency like this?

Understand that by printing more, the bankers and their political, intelligence, non-profit, and corporate friends can gobble up assets better than anyone else. They get the benefits of new money created out of thin air, while it negatively impacts all the other existing money in value.

This creates bubbles. Bubbles always pop. Whether engineered or not, growing bubbles contribute to economic inequality. The rich get richer. The poor get poorer.

…And the bubble popping is another crisis which gives license to print more money.

It’s a hell of a system. Kicking the can down the road like this, without any fundamental reform, only delays and grows the problems that will have to be dealt with at some time.

Many in the financial space liken this money printing to be hooked on crack, heroin and meth!

The Debt Death Spiral

A zombie company is defined as a company that either needs bailouts in order to operate or has debt that it can pay interest on but not principal. While some can get turned-around most ultimately go bankrupt.

It must be great to be too big to fail, right?

Bloomberg reported that since the pandemic started over 200 large corporations, with over $2 trillion in debt, were added to the list of zombies list. This included Boeing, Delta, Exxon Mobil, Carnival, Macy’s and more.

Even more important than companies…what happens when the US goes full on zombie government?

This was BEFORE all the pandemic bailouts. Are we already a zombie or will it be in 2022 or 2023?

I suppose they can just print more money to handle the debt, right?

How Safe are 401K’s?

Most IRA’s are only taxed when you withdraw from them. (Roth IRA’s being the exception, where you pay taxes before contributing and then can withdraw tax free.)

Here’s a question to ask yourself. By the time you’re taking money out, do you think taxes are going to:

A) stay the same? B) go lower? C) go higher?

Really take some time to ponder that question. They might just print money, but I’d also be willing to bet taxes will be going up.

With government spending ramping up, likely to ramp up even more, where do you think that money is going to come from?

And if you think only the richest people are going to be taxed, I’m sorry but you’re not paying attention. Yes, there are things like the proposed California wealth tax, but the brunt will always fall on the middle class, while the elites have their ways of avoiding the worst of such policies. (After all, they’re paying the politicians to write the rules.)

I know some of my readers are already retired. Others won’t for decades to come. But you really need to project out where you think the USA is going for this.

Do you even own Your 401K?

Can the government just take your 401K? Not with current laws. But laws can change. Apparently, this would take going through Congress, the President and the Supreme Court. Again, if you think this is impossible, I ask you how many impossible things happened in 2020?

My friend Garrett Gunderson first clued me into this. In a Forbes article he wrote, “Did you know that your 401(k) does not even technically belong to you? Read the fine print and you will find that it is what’s called an “FBO” (For Benefit Of). In other words, it’s held in trust by a custodian on your behalf and is subject to a slew of government regulation and change. It’s essentially a tax code. If history proves to be a reliable guide, 401(k) funds are therefore in great jeopardy! In the same way that the government raises and lowers taxes at their whim, it can change the rules and take the money that you so diligently saved.”

But realize that is just one means of transferring wealth.

Even if 401K’s aren’t touched, we know that the markets are largely rigged. I don’t know if it is completely so, or just partially, but insider’s do have ways of creating, inflating and popping bubbles to their benefit. They can ride the bubbles on the way up and get out before they pop.

In 2008, my mom’s retirement in her 401K was cut in half by the stock market crash. She passed away before she retired (because of the poisoning of our environment and ineffective medical care) but I know she was worried that she wouldn’t be able to retire when she planned to. She’d have to work longer because of the market of which she had no control. She just trusted that her 401K was a wise choice.

Is the Stock Market Safe?

We saw stocks drop significantly in March of last year, only for it to resume going to new highs. The stock market is thriving only because of the money being pumped into the system. But that won’t inflate it forever.

But what goes up must come down.

There will be another bigger and prolonged crash at some point. Guaranteed.

Most people have ZERO control over their 401K’s, all of which is in the stock market. It’s managed by some mutual fund, typically paying a hefty but hidden fee for the privilege.

A better option in my mind is a self-directed 401K. This way you can do much more than index funds in the stock market. With the right setup you can invest in businesses, real estate, precious metals, foreign assets, and even cryptocurrencies.

Personally, I don’t have a 401K. And I don’t ever plan to. Truthfully, I don’t even buy to the idea of retirement for myself. That doesn’t mean I’m not working for my future; I’m just using different vehicles to do so.

The fact that you don’t actually own it makes it highly suspect in my mind.

What if the government decides that all white people need to pay reparations for their whiteness and the 401K is a good way to do that? Because obviously, if you have a 401K you’re privileged and engaging in white supremacy.

I only say this in partial jest with the direction things are going…After all, if math can be racist, all things are on the table!

It’s not a far leap from the right answers in math being racist, to any financial literacy and therefore retirement funds being racist.

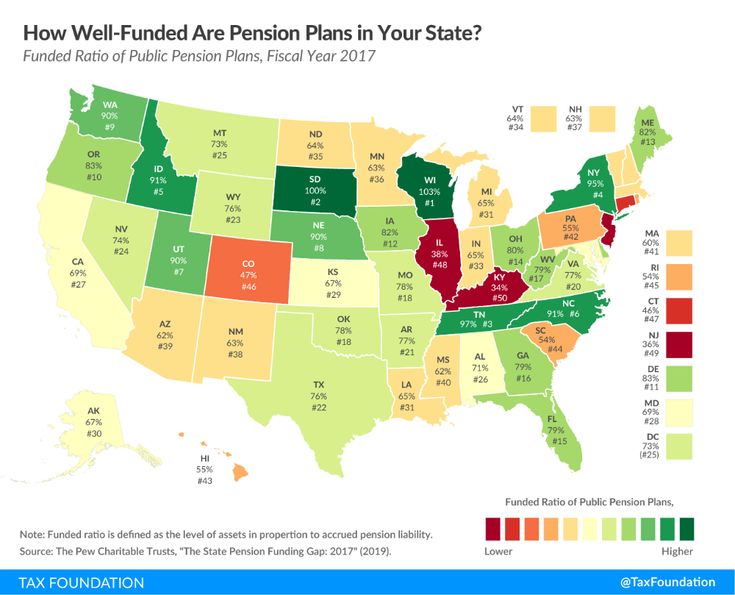

How Safe are Pensions?

Virtually all the state pensions are underfunded.

Here’s a graphic from 2017 showing the average state is short about 30%. Some like New Jersey are deeply in the red. Only two states, South Dakota and Wisconsin were fully funded.

That’s government workers. What about private pensions?

There are many more examples of such actions the world over. Do you think this kind of thing is impossible within the USA?

Is it American exceptionalism alone that protect us?

A good question is why are these pensions underfunded? The government is full of crooks that are already robbing us every chance they get. For the sociopaths involved, they’ll continue to rob us of anything and everything with whatever they can get away with. Of course, there are ways of getting at pension money, just like social security which will be bankrupt within a couple years.

Yes, there is tons of government waste. But so much more of this money is going into the pockets of corporate partners. (Like all those private prisons and contractors. It’s a very profitable system and has been for decades to throw victimless criminals in jail.)

Moderna was almost 100% government funded, the last little bit kicked in from…you guessed it, the Gates Foundation.

Public funding, yet Moderna gets to keep the profits private. Furthermore, the private companies have zero product liability, that falls on the government too. That’s one a hell of a deal!

This is how the organized criminal syndicate runs. This is why the system is so overburdened with debt. the criminals loot money from taxpayers to pass back and forth between each other.

The Student Debt Bubble

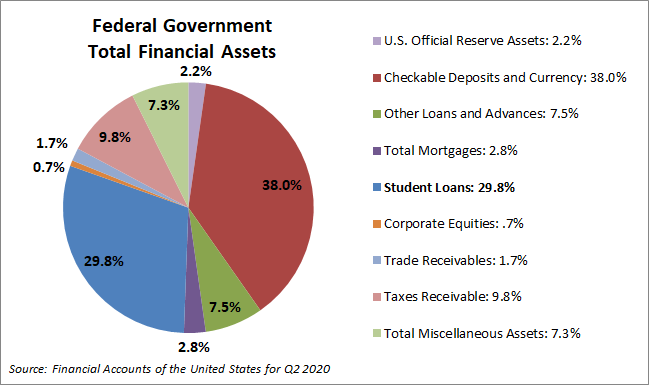

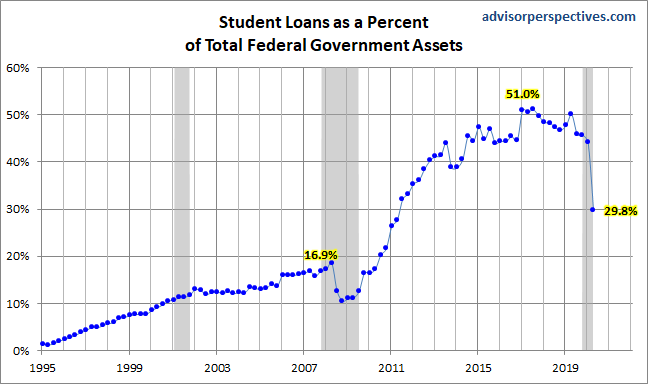

Student loan debt makes up almost a third of the assets of our government.

And previously it was even a larger chunk, over 50% of governement assets!

Student loans are certainly a racket that screws over people big time. I’m not trying to debate that here.

But just looking at it from the other side…what happens when you get rid of the biggest asset held by a government quickly going bankrupt?

I suppose you can just raise taxes or print more money to make it up.

The Dollar Continues to be Downplayed Across the World

The discussions between Russia, China and other countries about moving away from the dollar continue to occur. This has been going on for years now.

Recently, Nikkei Asia reported, “Russian Foreign Minister Sergei Lavrov began a visit to China on Monday with a call for Moscow and Beijing to reduce their dependence on the U.S. dollar and Western payment systems to push back against what he called the West’s ideological agenda.”

“Washington has been abusing SWIFT to arbitrarily sanction any country at will, which sparked global dissatisfaction. If China and Russia could work together to challenge the dollar hegemony, a laundry list of countries would echo the call and join the new system,” Dong Dengxin, director of the Finance and Securities Institute at the Wuhan University of Science and Technology, told the Global Times.

But it’s not just our “enemies” saying this…

Mark Carney, governor of the Bank of England said in 2019, “The world’s reliance on the U.S. dollar won’t hold and needs to be replaced by a new international monetary and financial system based on many more global currencies.”

The Coming Shocks

Understand that all this IS the desired outcome by many at the top of the financial pyramid. It allows the cover-up of crimes over the decades and for the global ponzi scheme to continue. And of course, even more power and control.

How? Read The Shock Doctrine. At the very least watch the documentary. It’s a great overview of how things have worked and will continue to do so.

An analogy that I think fits is that we’ll be going through a fall-of-the-USSR type of change, covered about halfway through the video here.

(Though they went “communist” to “capitalist”, while our case seems more in reverse. Those labels aren’t what is most important, but instead to see the commonalities of the economic impacts! In either case powerful oligarchs manipulating the systems are profiting while people suffer.)

By continuing to manipulate markets, loot pensions and taxpayers, this allows for benefits to them today and bigger shocks for the common people later.

Then greater austerity measures will be introduced.

Your acceptance of the totalitarians aims in order to get your handouts are the carrot. Their threats and violence, the stick.

Furthermore, while tested out with Ebola, the bird and swine flus, and even earlier, we can say that “Pandemic Capitalism” is definitely on the rise.

Let me ask a few questions…

Did drugs go away after we declared war on them? (Not when intelligence agencies were funding their black ops by running drugs.)

Did cancer go away after we declared war on it? (Not when the pharmaceutical-industrial-government complex is profiting from both causing and curing cancer.)

Did terrorism go away after we declared war on it? (Not when the military-industrial complex profited trillions.)

We declared war on the coronavirus. Does that mean the coronavirus be gone soon?

It is frustrating to me that people think we’re getting back to normal now.

A temporary reprieve at best. Something that serves to drive us deeper into trance come the next shock.

No, the endless wars (not just physical) have been running for a long time now.

Looking at and understanding the economics of it (instead of getting wrapped up in left/right politics, royal scandals with Markle and Oprah, even scientific debates about health) will give you the most clarity moving forward.

That’s why I’m going to be talking about this even more.

Economics is probably the most useful lens to use to see how the world really works.

My Conclusion: US Dollars are Not Safe

Wrap your mind around that. To keep assets in USD is risky. Once again, I don’t think the dollar is going away anytime soon. It’s a step-by-step process that will unfold over the next several years.

But we are on that road.

The value trend is going down while other assets inflate. (Despite a spike up in USD value recently. That likely has to do with it’s not just the US printing money either.)

Not today, but soon. Perhaps somewhere in 2023-2025 when the US debt stands at $40 trillion, we’re a zombie government, social security is bankrupt, and more has all occurred?

That’s the old system. What about the new?

I found this interesting. Soros Fund Management chief information officer Dawn Fitzpatrick said, “We think the whole infrastructure around crypto is really interesting, and we’ve been making some investments into that infrastructure — and we think that is at an inflection point…I think when it comes to crypto generally, we’re at a really important moment in time, in that, something like Bitcoin might have stayed a fringe asset, but for the fact that, over the last 12 months, we’ve increased money supply in the U.S. by 25%.”

The hedge funds are seeing it. Are you?

An inflection point.

You can literally follow the money right now as we go from the dollar system to the new system.

By that I mean follow the money with your money.

Of course, this doesn’t make cryptocurrencies completely safe either. Far from it. A big crash will come there too. A huge shock which allows the “Fedcoin” to come in is almost assured at some point.

But right now, as it is in the “invention room” we’re FAR from the totalitarian control of the system. We are going through the massive change right now.

So many in the crypto space are against the totalitarian control. But just like everything else, you need to seek to see what is going on behind the scenes.

Most of my assets besides my businesses are invested in cryptocurrency right now.

The writing is on the wall. I’m reading it. I could be wrong about this trend , but I don’t think I am. I certainly benefited by seeing this trend last year.

This gives me time to profit from the asset inflation, the bubble, take profits along the way and get out when the time is right.

To reinvest those profits in my family, my community, supplies and Plan B scenarios. Also to fund those that are fighting the good fight.

You might think me risky to do so…but as I’ve shown, money, the US dollar, is risky right now.

There is risk either way…

But I am trusting in my understanding of the global system! I’m almost all in.

More Spots Opened Up

Reading over this article multiple times, I feel like it may be stoking lots of fear. I sincerely apologize for that, but I think it is best to be realistic even if it looks incredibly pessimistic.

There still is hope that the system implodes on itself allowing people to get free. But even if that happens that too will be rough.

Neither should this be construed to mean that cryptocurrency is some utopian thing that will save us all. I hope I’ve clearly explained how it very well could be the exact opposite.

Still, I do believe their is a window of opportunity here. So much so that I’m not just doing it myself but sharing this message with others.

On that note, my crypto crash course coaching is going great. Several have made their first investments already. (One even got in right before one token shot up in value about 20%. Good timing there.)

As I’m halfway through with several clients, I’ve decided to open up a few more spots. If you’re interested email me at logan@legendarystrength.com and I’ll send you more details.

Even if you don’t work with me I hope you’ve taken this message to heart and are a little better prepared, psychologically…and perhaps financially… for what is coming.

Cast your mind back to the earlier days of the internet. Do you remember when online banks became a thing?

And many people were scared to use them. “How could you trust a bank that didn’t have a building?” they asked.

Your money would disappear into the electronic ethers and you’d have to trust it would be there. I remember when I first signed up for one such bank, ING Direct. My parents thought I was crazy to do so!

That fear seems pretty naïve at this point of the pervasive internet, right?

While I’m sure that some still swear off these things, they’ve become quite common. People routinely do banking, make payments, buy and sell stocks off their smarts phones these days.

But that yield has gone down, closer to what the big banks were giving. One of the places I used, has gone from 1.5% down to a measly 0.5%.

This does not even keep up with the inflation we have going on. The Fed expects 2.4% this year…when we know better than to trust official numbers. (That means it is most definitely higher.)

In other words, holding money in a bank account is a good way to lose.

No thanks, I need a better option.

EnterDeFi

DeFi stands for Decentralized Finance. Basically, this is the ecosystem that has sprung up around cryptocurrencies, most notably the Ethereum network.

By being decentralized it relies on smart contracts and a network of people. There are no centralized hubs like the banks. Instead, there are decentralized applications that build a financial platform available to everyone that operates peer to peer.

Let me check in…have I already lost you?

Do you understand what I’m talking about, or did your eyes glaze over earlier?

In the past months I’ve been having quite a few conversations with different people on these topics. And most simply cannot wrap their heads around it. It is too different from what they know.

New is challenging. Like conspiracy topics they don’t seek to understand because they want to stay safe within their worldview.

I understand it’s not easy to grasp. Yet, that is part of the reason it is important to do so now. Get ahead of the curve not behind, as I talked about in my last post.

Let me take you back in time…

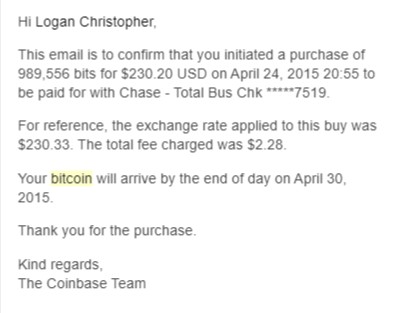

It was 2015 and I had heard about Bitcoin from several different sources. So I dug in. I decided I had to get what this was. It took me some time to do so, looking at multiple sources. It was challenging. But the reward was then I felt like I understood enough that I could begin investing.

On April 24th, 2015 I bought my first ever Bitcoin for $230.20.

Was that a good choice? While I have made many mistakes along the way, the fact that I saw the future coming at least to some degree, and did the hard work of trying to understand it, paid off.

The question is will you do the same if you haven’t already?

The Easiest Way I’ve Found into the Benefits of DeFi…without the Complications!

Why did I bring up online bank accounts? Because it is much the same here.

I’m going to cover more of the complex stuff in the future. But first I want to simplify it for you. Can you get the power (and benefits of DeFi) without actually understanding any of it?

Yes, you can.

What follows is the simplest route in that I’ve found. This doesn’t involve exchanges, setting up wallets or anything like that.

Unfortunately, at this time it is only available for iOS. But they are working on Android.

And that leads me to start with what I do not like. This financial app is exclusively for your smart phone, or iPad. They have a website, but you can’t even login there! You can only interface through the app right now.

Let me be clear, I do not like this trend. Since most of my work is at a computer, I use a desktop. I really don’t even use my cell phone much. But this is where things are going. (And that’s not to mention the whole being controlled by the smart device thing which will grow and grow.)

The good news is that if you can and do use any financial apps, you can do this too.

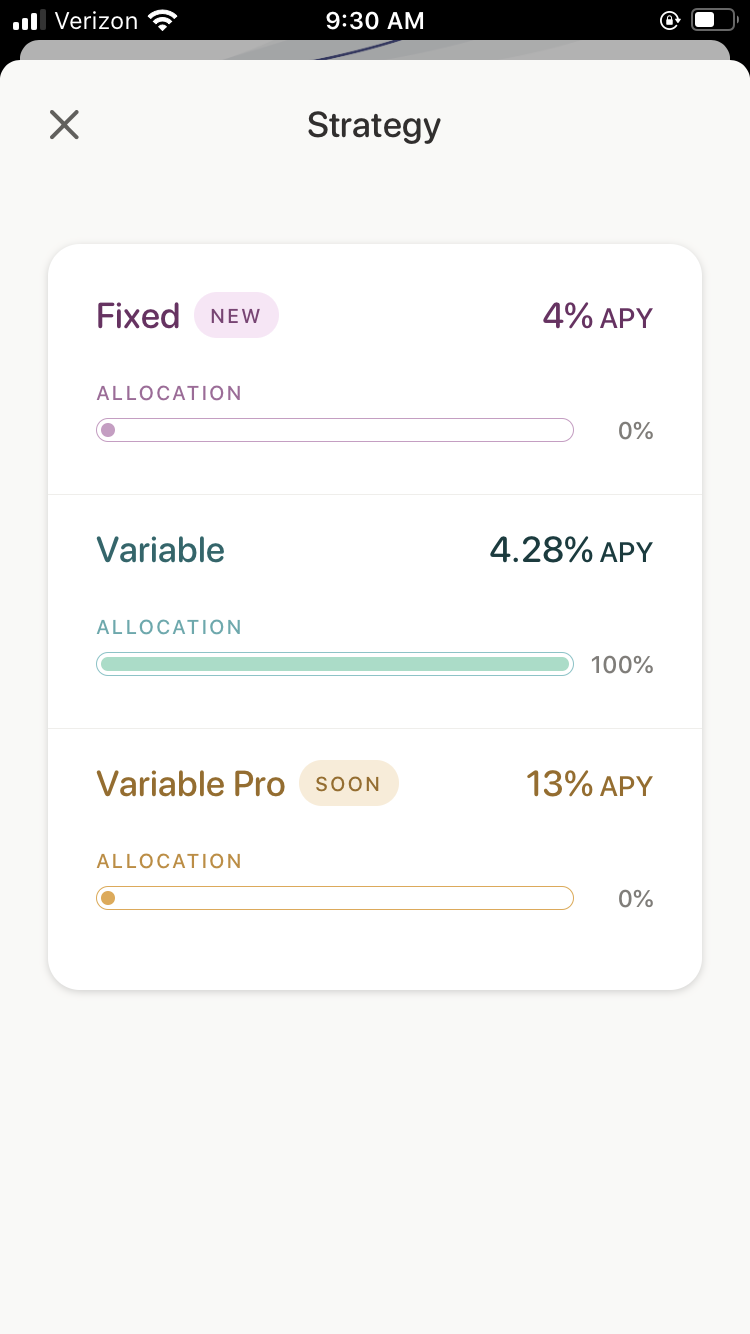

How Would You Like to Earn 4-13% on Your Cash?

Basically, because in DeFi there are ways to earn much larger yields, 5-12% is quite easy, and possibilities of making a ridiculous 1000%+, this company can use the money you save to do so.

And they can give you your cut of 4% for use of your funds.

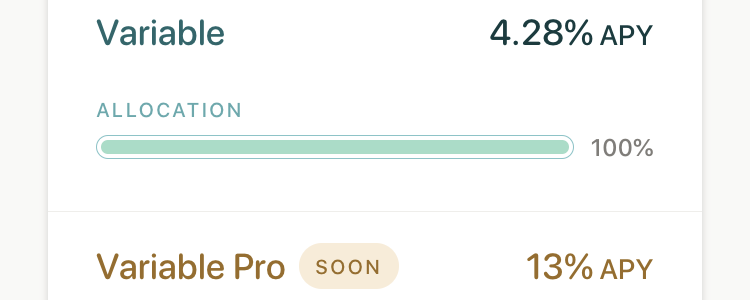

Here is an actual screenshot from my account. I have only been using this for a couple of months and have already earned more interest than a full year of my online savings accounts with a much smaller balance.

In fact, you can get more than 4%. You can select the variable amount. At the time of this screen shot it was 6.96%. I have seen it move below 4% as well. (The thing is you can click a button and then move back to the standard 4% when that happens too.)

And soon they’re planning on offering even more. This morning I took another screen shot. You can see the variable rate is just above the fixed rate at 4.3%. And they have a Variable Pro rate of 13% coming soon.

So at the very least you’re earning 8x times more than most banks offer. And there are possibilities for much more than that.

This is the power of DeFi…made really simple to get started with.

To understand this, you have to understand more about digital currencies. One thing (of several) that have stopped their widespread adoption is the volatility. The space does go through some wild swings.

And this is why stablecoins were created. They are cryptocurrencies that are pegged to a (comparatively) stable asset, such as the US Dollar.

These are basically a cryptocurrency versions of the US dollar. Like a digital dollar but typically backed by real cash and audited (PAXOS), backed up by code and a basket of other cryptocurrencies (DAI), or seemingly backed by cash but actually a scam (USDT aka Tether). More on stablecoins including the scam details another time.

In short, these stablecoins are stable in price compared to other cryptocurrencies. Importantly for this topic, they can be lent out in a variety of ways to make money in the space.

With Donut, your cash is converted into stablecoins (DAI specifically) and then lent out for you. You can withdraw your cash at any time.

Is this Risky? Is this Safe?

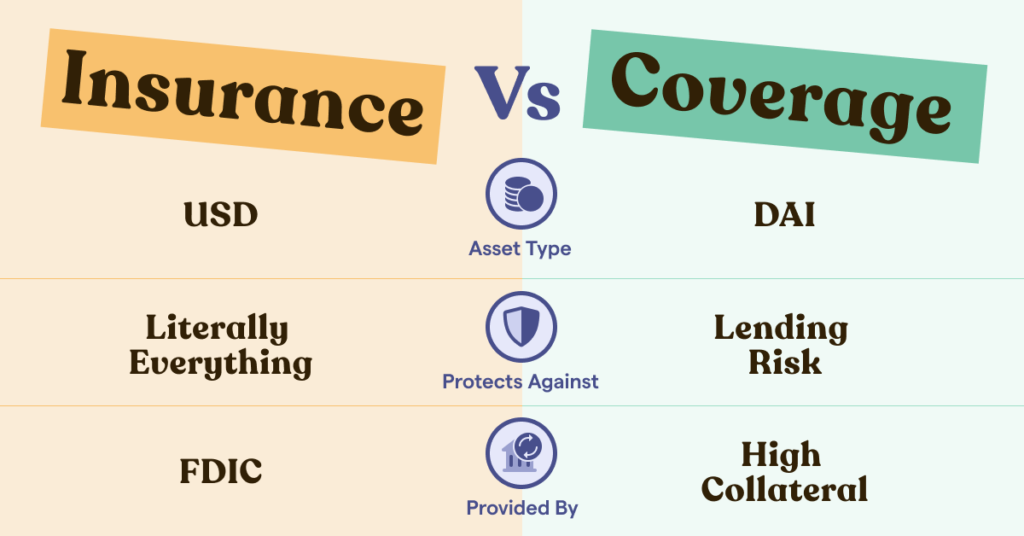

First of all, this is not FDIC insured. There is no Federal guarantee that your money is protected. (As you might imagine, there are financial problems with this federal agency, I plan to explore in the near future.)

FDIC insurance backs every bank account. But not this.

But the fact that this lending is backed by collateral ultimately acts as coverage, at least to a degree. While there are ways of leveraging such assets, within DeFi lending things tend to be collateralized over 100%. Often 150%. So it is safer in that way.

Donut has been around since 2019. I know that doesn’t sound like much but that is a decent timeframe for a stable company in this space!

Ultimately, time will tell. There is a big crypto crash at some point in the future. Nothing ever just goes up. When that crash occurs does the collateral cover everything so that Donut and their users have zero problems? I hope so. For my sake and theirs.

Ideally, I would like to see even more information on their website including audited reports.

My Use of Donut

I would NOT recommend you ditch any and all other investments and use only this. Far from it. Instead try it out as one place to make use of.

Diversification of platforms is one of my strategies especially in this newer field.

I am actively using Donut as one of my savings accounts. Sure, I can use those funds within the crypto space and make even more doing the lending myself.

One thing I like about this is the extremely quick liquidity of it. You can withdraw your cash at any time and it’ll arrive back to your bank within 1-5 business days.

This is far from the end-all, be-all of DeFi, but I choose to share it as it’s an incredibly easy intro point where you can get some of the benefits of crypto without the hassles of it.

Regardless of whether or not you choose to (or can) use this app, I hope that this served as an intro into the space. Much more to come in the future.

Let me know if you have any questions below.

Disclaimer: This is not to be used as financial advice. Logan Christopher and Legendary Strength LLC are not registered investment, legal or tax advisors nor a broker/dealer. All investment opinions expressed are from personal research and experience. Email and website content is to be used for informational purposes only. Logan Christopher is personally invested (long) in a number of cryptocurrencies.